Health insurance card, laptop, and notes about therapy coverage on a desk

Does Health Insurance Cover Therapy Services?

Content

If you're wondering whether your insurance will pay for mental health counseling, you're not alone—this ranks among the top questions people ask when they're ready to seek help. The insurance landscape for therapy has shifted dramatically over the past decade, yet confusion still reigns about who pays what, which providers you can see, and how much will actually come out of your wallet.

Here's what you need to know upfront: coverage for therapy exists across nearly all modern health plans, thanks to federal legislation passed in 2008 and strengthened in 2010. That said, your actual experience depends heavily on your specific policy details, your provider's network status, and how well you understand the financial mechanisms at play before you book that first appointment.

Understanding Mental Health Coverage in Health Insurance Plans

When we talk about the does health insurance cover therapy definition, we're really discussing mental health parity—landmark federal legislation requiring insurers to treat behavioral health benefits on equal footing with medical and surgical care. The Mental Health Parity and Addiction Equity Act of 2008, later reinforced through the Affordable Care Act, fundamentally changed how insurance companies must handle therapy coverage.

Under these laws, your insurer can't discriminate against mental health services by charging steeper copays than what you'd pay for a regular doctor visit, demanding more aggressive pre-approval processes than those required for medical procedures, or creating separate deductible buckets exclusively for behavioral health. In practice, if your plan charges a $25 specialist copay, your therapy copay shouldn't exceed that amount.

Therapy now falls under essential health benefits—a category of ten service types that all non-grandfathered plans must include. Employer coverage, individual policies purchased through Healthcare.gov or state exchanges, Medicaid programs, and Medicare all incorporate mental health services. The exception? Plans grandfathered under the ACA (those continuously active since March 23, 2010, without significant changes) may operate under old rules with thinner behavioral health benefits.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

One critical nuance: having coverage doesn't mean accessing care is seamless. Enforcement of parity laws remains spotty. Patients regularly report that insurers still create hurdles—questioning medical necessity more aggressively for therapy than for physical conditions, maintaining inadequate provider networks, or processing mental health claims more slowly. These challenges persist despite the legal framework protecting your rights.

Whether you've selected a Bronze plan with lower premiums or a Platinum option with minimal cost-sharing, mental health coverage must be included. Your out-of-pocket expenses will vary significantly across metal tiers, but the actual types of services covered remain consistent.

What Types of Therapy Are Covered by Health Insurance

Examining what does does health insurance cover therapy cover reveals a surprisingly broad scope of services eligible for reimbursement:

Individual therapy sessions represent the foundation of covered mental health services. Whether you're working with a licensed professional counselor, clinical psychologist, psychiatrist, or licensed clinical social worker, one-on-one treatment for conditions like depression, anxiety disorders, PTSD, OCD, or bipolar disorder typically receives approval. Most insurers green-light weekly 45-minute sessions initially, though your therapist may recommend different frequencies based on your needs.

Group therapy offers a cost-effective alternative that generally receives coverage when facilitated by licensed professionals. You might join a cognitive behavioral therapy group for panic disorder, a dialectical behavior therapy skills group, or a grief support circle. Per-session costs run lower than individual therapy—often 50% to 70% of individual rates—and your insurance applies the same coverage rules.

Family therapy qualifies for benefits when addressing a mental health diagnosis affecting household dynamics. The key factor: someone in the family must have a diagnosable condition requiring treatment. If your teenager has been diagnosed with major depression, family sessions exploring communication patterns and support strategies should receive coverage. Some plans require the identified patient to participate in every session; others allow family-only sessions within an overall treatment plan.

Marriage and couples counseling exists in murkier territory. Standard relationship counseling without an underlying mental health diagnosis often gets excluded. However, when one or both partners carries a diagnosis and couples therapy serves as part of their clinical treatment plan, coverage becomes more likely. For example, if one spouse developed anxiety following job loss and couples therapy helps address resulting marital stress, that may qualify. Documentation and diagnosis coding become crucial here.

Telehealth therapy exploded during 2020 and permanently changed how insurers approach virtual care. Today, video sessions receive identical coverage to in-person appointments across most plans. Medicare removed geographic and originating site restrictions for behavioral health telehealth in 2023, and private insurers have largely followed suit. Your $35 copay for an office visit should match what you pay for a HIPAA-compliant video session.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Inpatient psychiatric treatment receives coverage during acute crises requiring round-the-clock supervision—think severe suicidal ideation, psychotic breaks, or dangerous substance withdrawal. Outpatient intensive programs sit between standard therapy and hospitalization. Intensive Outpatient Programs (IOP) typically involve 9-12 hours weekly across 3-4 days, while Partial Hospitalization Programs (PHP) provide 5-6 hours daily, 5 days weekly. Both require pre-authorization and involve different cost structures than regular therapy.

What doesn't get covered? Life coaching focused on career development or personal success rather than treating mental illness. Court-mandated anger management unless it meets medical necessity criteria. Educational counseling helping students with college selection. Performance coaching for athletes or executives. These services may be valuable, but they fall outside medical treatment definitions.

How Therapy Coverage Works Under Your Health Plan

Grasping how does health insurance cover therapy works means getting comfortable with insurance terminology that determines your actual financial responsibility.

Deductibles and Out-of-Pocket Costs

Think of your deductible as the threshold you must cross before your insurance starts sharing costs. In 2026, individual deductibles commonly range from $1,500 up to $8,000 depending on your plan design and employer contributions. Before crossing that threshold, you'll pay the full contracted rate your insurance company negotiated with in-network providers—usually $100-$200 per therapy session depending on your location and therapist credentials.

Here's where the does health insurance cover therapy deductible explained becomes important: plan designs vary significantly. Some insurers apply therapy visits toward your general medical deductible, meaning you pay full freight until you've spent enough on all healthcare combined. Other plans built therapy into their copay structure, letting you pay a fixed amount per visit ($30, for example) regardless of whether you've satisfied your deductible. High Deductible Health Plans (HDHPs) paired with Health Savings Accounts always require meeting the deductible first—though you can use tax-advantaged HSA funds to cover those costs.

Once you've cleared your deductible hurdle, cost-sharing kicks in through either copays or coinsurance. Copays represent flat fees—perhaps $40 per session for a specialist visit. Coinsurance means you pay a percentage of the allowed amount, commonly 20%-40%, with your insurer covering the rest. These payments accumulate toward your out-of-pocket maximum—the ceiling on your annual spending for covered services. Federal regulations cap these maximums at $9,450 for individuals and $18,900 for families on marketplace plans in 2026, though employer plans negotiate their own limits.

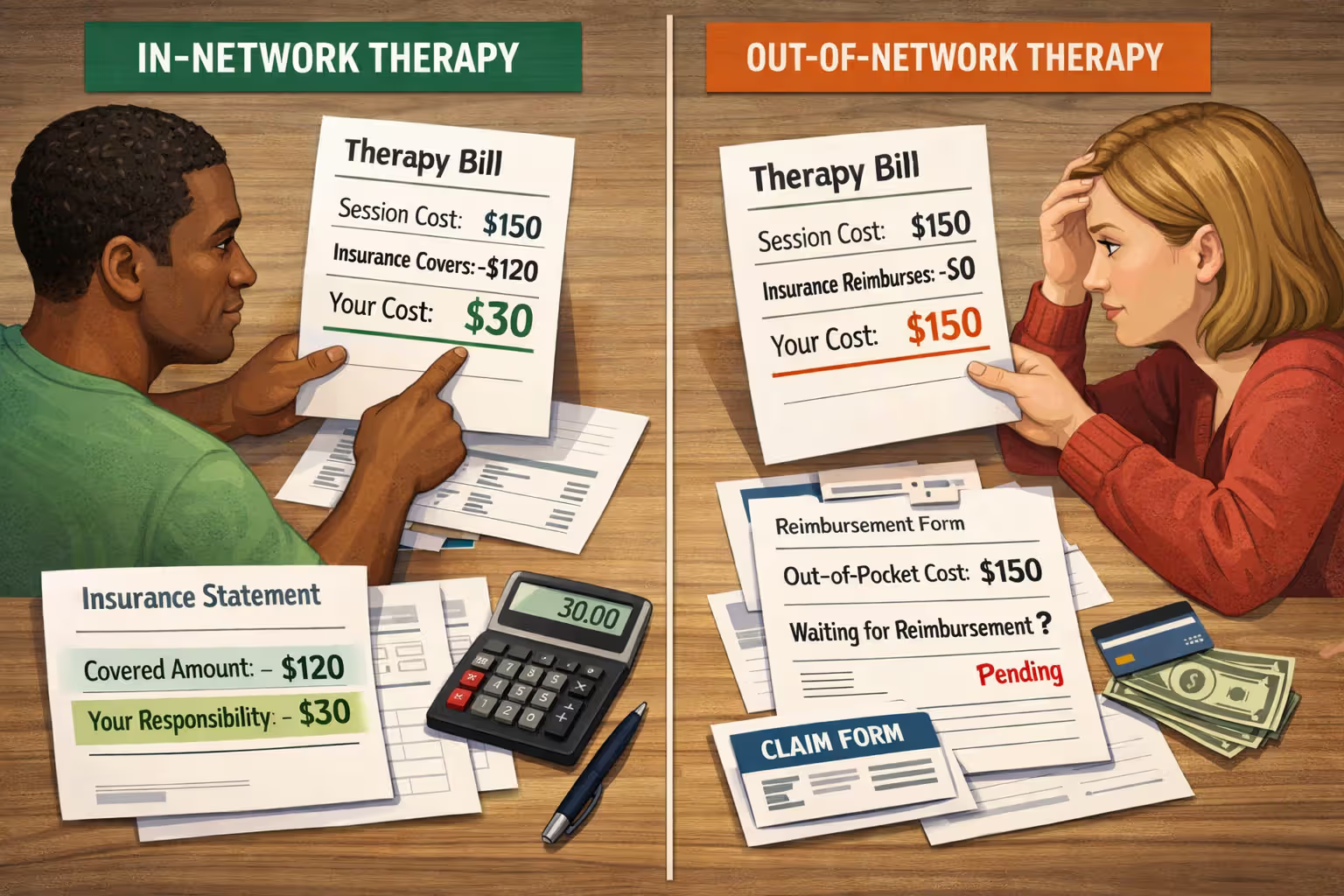

In-Network vs. Out-of-Network Providers

Provider network status makes an enormous financial difference. In-network therapists have signed contracts with your insurance company agreeing to accept negotiated rates as full payment and handle claim filing directly. Out-of-network providers charge their market rates—often $150-$300 per session in urban areas—and your insurance may reimburse only a fraction, if anything.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Consider this real-world example: Sarah sees an in-network therapist in Chicago. Her negotiated rate is $120 per session, but she only pays a $30 copay after meeting her deductible. Total annual cost for weekly therapy: $1,560 in copays. Her friend Michael sees an out-of-network therapist charging $180 per session. His plan reimburses 60% of "reasonable and customary" charges after a separate $3,000 out-of-network deductible. Michael pays $180 upfront, files claims himself, and eventually receives $108 back—netting $72 per session. Annual cost for weekly therapy: $3,744 plus his $3,000 deductible for the first 17 sessions. That's $8,844 versus Sarah's $1,560.

Plans handle out-of-network coverage differently by type. PPOs generally offer the most flexibility, reimbursing 50%-70% of out-of-network care. HMO and EPO plans may provide zero coverage outside their network except for emergencies. POS plans fall somewhere between. Many plans also maintain separate out-of-pocket maximums for out-of-network care, meaning costs don't cross-apply.

Session Limits and Pre-Authorization

While mental health parity laws banned arbitrary session caps, insurers still apply "medical necessity" reviews. Most plans initially approve a set number of sessions—perhaps 12 to start—then require your therapist to submit progress notes and treatment justifications for continued authorization. This parallels how chronic medical conditions get monitored; your doctor must document why you still need blood pressure medication after six months.

Pre-authorization requirements vary wildly. Some plans demand approval before your first visit. Others allow an initial evaluation without pre-auth, then require approval for ongoing treatment. Many plans skip pre-authorization entirely for standard outpatient therapy while requiring it for intensive programs. Psychiatry visits, especially medication management appointments, typically need less documentation than long-term talk therapy.

Your therapist's billing staff usually handles authorization requests, but ultimate responsibility sits with you. Attending sessions without proper approval can result in denied claims leaving you liable for full charges—potentially hundreds per session.

Coverage Limits and Restrictions You Should Know

Understanding does health insurance cover therapy coverage limits requires recognizing several common restrictions that coexist with parity protections.

Medical necessity standards create the primary gatekeeping mechanism. Insurance companies require a diagnosable condition from the DSM-5-TR (Diagnostic and Statistical Manual of Mental Disorders, Fifth Edition, Text Revision). Your therapist must document specific symptoms, functional impairment in work or relationships, and measurable treatment goals. A diagnosis like Major Depressive Disorder with documented symptoms affecting your job performance typically sails through; Adjustment Disorder with vague symptoms may trigger additional scrutiny.

Network adequacy problems create practical access barriers despite theoretical coverage. Many insurance networks include insufficient numbers of mental health providers, particularly child psychiatrists, eating disorder specialists, trauma-focused therapists, or any mental health professionals in rural counties. Some states report that fewer than 25% of licensed therapists accept any insurance, creating de facto limitations on your covered options.

Diagnosis documentation requirements mean you need a formal mental health diagnosis on file to receive any reimbursement. Someone seeking preventive counseling during a stressful career transition without clinical depression won't qualify for covered visits. Your therapist assigns a diagnosis code (from ICD-11, the International Classification of Diseases) on every claim, which becomes part of your permanent medical record. This can affect future insurance applications, security clearances, or disability insurance in some circumstances—something to consider before using insurance for minor concerns.

Annual and lifetime benefit caps on mental health services were eliminated by the Affordable Care Act for essential health benefits. However, grandfathered plans predating March 2010, short-term health plans, and some supplemental policies may still impose dollar limits or visit caps. Review your Summary of Benefits and Coverage document carefully if your plan predates the ACA.

Step therapy or fail-first protocols occasionally require attempting lower-intensity interventions before approving higher levels of care. Your insurer might require four weeks of outpatient therapy before authorizing an Intensive Outpatient Program, or multiple medication trials before approving ketamine treatment for depression.

How to File a Therapy Claim with Your Insurance

The does health insurance cover therapy claim process splits into two pathways depending on whether your provider bills insurance directly or operates on a cash-pay basis.

Direct billing (the most common scenario): Your therapist's practice files claims straight to your insurance company. You pay your copay or coinsurance at checkout, and the practice collects the remaining allowed amount from your insurer within 30-60 days. This happens automatically with in-network providers who've signed participation agreements. You'll receive an Explanation of Benefits showing what your insurance paid, what applied to your deductible, and what you owe.

Manual reimbursement (for out-of-network or cash-pay therapists): You pay the full session fee upfront, then submit paperwork to your insurance company requesting reimbursement.

The step-by-step reimbursement process looks like this:

- Request a superbill after each session. This detailed invoice includes your therapist's full name and credentials, National Provider Identifier (NPI) number, tax identification number, the diagnosis code assigned to you (example: F32.1 for Major Depressive Disorder, single episode, moderate), the procedure code for services rendered (typically 90834 for 45-minute individual therapy or 90837 for 60-minute sessions), the exact service date, and total payment amount.

- Download and complete your insurer's reimbursement form. Most companies offer online portals or mobile apps for digital submission. You'll enter your member ID, group number (if applicable), patient demographics, and attach your superbill. Paper forms remain available via phone request if you prefer mailing claims.

- Track your submission. Upload documents through your member portal, use the mobile app, or mail paper claims to the address on your insurance card. Save copies of absolutely everything—take photos or scan all documents.

- Allow processing time. Most insurance companies process reimbursement claims within 30-45 days. You'll receive an Explanation of Benefits statement breaking down allowed amounts, deductible applications, and reimbursement calculations. Check whether it matches your expectations based on your plan details.

- Receive payment via direct deposit (if you've set this up through your member portal) or paper check mailed to your address.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

When claims get denied:

Start by carefully reading the denial reason. Common issues include incorrect CPT codes (your therapist used the wrong billing code), missing information (NPI number omitted), services deemed not medically necessary, or out-of-network benefits exhausted. Call member services immediately for clarification. Often your therapist can resubmit with corrected codes or additional clinical documentation supporting medical necessity.

If the denial persists after resubmission, initiate a formal appeal. Federal law requires your plan to provide an appeals process—beginning with internal review by different personnel than those who made the initial denial. Submit a detailed appeal letter including your therapist's clinical notes demonstrating medical necessity, relevant research supporting your treatment approach, and documentation of how your condition impairs daily functioning. If internal appeals fail, request external review by an independent medical reviewer. Your state insurance department can provide guidance and occasionally intervene in disputes, particularly regarding parity violations.

Understanding Your Therapy Coverage: Key Takeaways

| Coverage Scenario | What You'll Pay Per Session | Important Details |

| Paying Without Insurance | $100–$250+ depending on location and provider credentials | Consider asking about sliding scale fees based on income; community mental health centers often charge less; some therapists reserve reduced-fee slots |

| In-Network After Meeting Deductible | $20–$50 copay per visit | Most affordable option once deductible is satisfied; only copay owed per session with no additional charges |

| In-Network Before Satisfying Deductible | $100–$200 (negotiated rate) | Pay the contracted rate per visit until reaching your deductible threshold, then your cost drops to copay amount |

| Out-of-Network Provider | $150–$300 upfront; receive 50–70% reimbursement later | Significantly higher expenses; separate deductible frequently applies; requires filing claims yourself; reimbursement may take 30-60 days |

How to Verify Your Therapy Benefits Before Starting Treatment

Confirming coverage details before your first appointment prevents financial shocks and helps you budget realistically.

Contact your insurance company's member services line (printed on your card). Rather than asking whether they cover therapy generally, pose these specific questions:

- Are outpatient mental health services included in my plan benefits?

- How much will I pay per therapy session—is it a copay amount or coinsurance percentage?

- Will I need to satisfy my deductible before my copay kicks in, and how much of my deductible have I already met this year?

- Does therapy require pre-authorization, and if so, who initiates that process?

- How many sessions will you initially approve before requiring additional review?

- What's my plan's out-of-pocket maximum, and how much have I already spent toward it this year?

- Can you confirm whether [specific therapist name] participates in my network?

- Do telehealth appointments receive the same coverage as in-person sessions?

- What's the procedure code you expect therapists to use, and what diagnosis codes are typically covered?

Review recent Explanation of Benefits statements from other medical care to understand your deductible status and how your plan processes claims.

Contact your prospective therapist's office during your initial phone call. Many practices verify insurance benefits as a courtesy, researching your copay, deductible status, and authorization requirements before your appointment. However, remember this is an accommodation, not a guarantee—you remain ultimately responsible for understanding your coverage. Get any coverage information in writing via email.

Log into your insurer's member portal to search their provider directory, review your specific plan benefits document, and check year-to-date spending toward deductibles and out-of-pocket maximums. Most portals now include coverage estimators where you enter a service type and receive cost projections.

Locate your Summary of Benefits and Coverage (SBC), a standardized document federal law requires all plans to provide. Look specifically for the behavioral health or mental health section, which outlines copay amounts, coverage percentages, and any special limitations. This document follows a standard format across all insurers, making comparisons easier.

The single biggest financial mistake I see patients make is assuming their insurance will handle therapy coverage without confirming the details in advance. I've watched two patients with cards from the same insurance company discover they had wildly different coverage—one paid $25 per session while the other owed $150 until meeting a $5,000 deductible. They had different plan designs from different employers. Spend five minutes calling your insurer with your member ID and policy details handy. Get written confirmation of your benefits via their online portal or email. This tiny investment of time can mean the difference between affordable care and thousands in unexpected bills

— Dr. Patricia Chen

Frequently Asked Questions About Therapy Insurance Coverage

Getting clear on your insurance coverage for therapy services puts you in the driver's seat when making decisions about your mental health treatment. While navigating the system requires patience and persistence, federal parity legislation ensures mental health benefits receive equal status with medical coverage across most contemporary plans.

Before scheduling your first therapy appointment, invest 30 minutes verifying your specific benefits, understanding what you'll pay out-of-pocket, and confirming your chosen provider participates in your network. This upfront legwork prevents billing surprises later and lets you focus your energy where it belongs—on your healing and growth.

When you hit obstacles accessing covered care, remember you're not alone. State insurance departments maintain consumer assistance programs. Mental health advocacy organizations like the National Alliance on Mental Illness (NAMI) offer navigation support. Your therapist's administrative staff has likely helped hundreds of patients work through similar issues. Many people successfully access fully covered or affordable therapy once they understand their plan's specific requirements and know which questions to ask.

Seeking mental health treatment represents an investment in your overall wellbeing that pays dividends across every area of life. With solid knowledge of your insurance benefits and a willingness to advocate for yourself, you can access quality care while keeping costs manageable.