Person reviewing health insurance paperwork at home

COBRA Coverage Guide for US Workers

Content

Your job just ended. Your last day of health insurance? Also ending. Now what? That's where COBRA steps in—a federal lifeline that lets you keep your employer's health plan after you've left the company. Sounds great, right? Then you see the price tag and suddenly you're wondering if there's a better option out there.

What Is COBRA Coverage?

Back in 1985, Congress passed the Consolidated Omnibus Budget Reconciliation Act. (Yes, that's a mouthful—everyone just calls it COBRA.) Here's what it actually does: forces certain employers to let you stay on their group health plan temporarily after you leave, though you'll foot the entire bill yourself. Think of it as your health insurance's "pause button" rather than hitting stop.

The cobra coverage definition boils down to this: same exact coverage you had before, except now you're paying what your employer used to pay on your behalf.

But COBRA doesn't apply to everyone. The federal rules only kick in when your employer has at least 20 people on the payroll for more than half the working days in the prior year. Work for a smaller outfit? Your state might have "mini-COBRA" laws covering companies with 2-19 employees, though these typically last for shorter periods than federal COBRA.

What actually triggers your right to COBRA? Several events open that door. Lost your job (unless you did something truly egregious)? That qualifies. Hours cut so far back that you no longer meet the eligibility threshold? Also qualifies. The rules expand for your family members—they can get COBRA if you pass away, if you divorce or legally separate, once you enroll in Medicare, or when a child hits the age limit on your plan.

Here's where timing gets crucial. Let's say you get terminated. Your former employer has a month to alert the health plan administrator. That administrator then has two weeks to mail you your election paperwork. Miss that notification by not updating your address? You might not even know you have COBRA rights until it's too late. For life events you control—divorces, mostly—you've got 60 days to tell the administrator yourself, or those rights evaporate.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

How COBRA Coverage Works

Understanding how cobra coverage works means mastering a calendar full of deadlines that don't bend. Your election notice arrives in the mail. From that moment (or from whenever your coverage actually stopped, whichever comes later), you've got 60 days to make up your mind. Not 65 days. Not "around two months." Exactly 60.

Here's the silver lining: if you do elect COBRA, your coverage reaches backward in time. Wait 50 days to enroll? Fine—your coverage still starts from day one of your unemployment. That doctor visit three weeks ago? Covered. This retroactive feature creates an interesting gamble some people take, which I'll explain in the costs section.

Sign up for COBRA, and another deadline appears: 45 days to submit your first payment. That payment needs to cover everything from your termination date forward. Skip this deadline and the plan administrator can rip up your election like it never happened.

How long can you actually keep COBRA? That depends entirely on why you qualified. Job loss or reduced hours typically buys you 18 months. Become disabled according to Social Security's definition within your first two months of COBRA? You and your family might stretch that to 29 months. Certain qualifying events affecting dependents—divorce, death of the covered employee—can extend coverage all the way to 36 months.

Let me walk through a real timeline. James gets laid off May 20, 2026. His employer notifies the plan administrator by June 15. James receives his election packet on June 28, which gives him until August 27 to decide. He mails his election form August 20 and has until October 4 to pay premiums covering May 20 through August 31. His 18-month window closes November 20, 2027.

What COBRA Covers and What It Doesn't

What does cobra coverage cover? Literally everything your employer plan covered before—no more, no less. COBRA isn't a new insurance policy. You're staying on your old plan under different payment terms.

Had medical, prescription, dental, and vision before? All of that continues under COBRA. Here's the catch: it's all or nothing. You can't elect to keep medical but drop dental to save money. The entire package continues as a unit, which means you're paying for every piece your employer plan included. On the flip side, if your employer only offered medical coverage without dental, COBRA won't magically add dental just because you're now paying the full freight.

Your provider network stays frozen in place. That cardiologist you've been seeing for three years? Still in-network. The hospital across town that accepted your insurance? Still accepts it under COBRA. This continuity matters enormously if you're mid-treatment or have established care relationships with specialists who don't take every insurance plan.

Prescription coverage continues with identical copays and the same formulary. Paid $15 for generics before? Still $15 under COBRA. That specialty drug your insurance covered? Still covered at the same rate. You're just covering the premium costs your employer used to subsidize.

What if your former employer switches plans after you elect COBRA? Generally, you switch too, under the same terms as active employees. But any benefits your former employer adds after you leave don't flow backward to you unless all employees get them through a plan change.

One more thing: yes, technically you can continue a flexible spending account (FSA) under COBRA. Financially, though? Almost never worth it. You'd pay 102% of your remaining annual FSA election as monthly premiums. Unless you have massive planned expenses and a huge remaining balance, you're paying more in premiums than you'll get back in reimbursements.

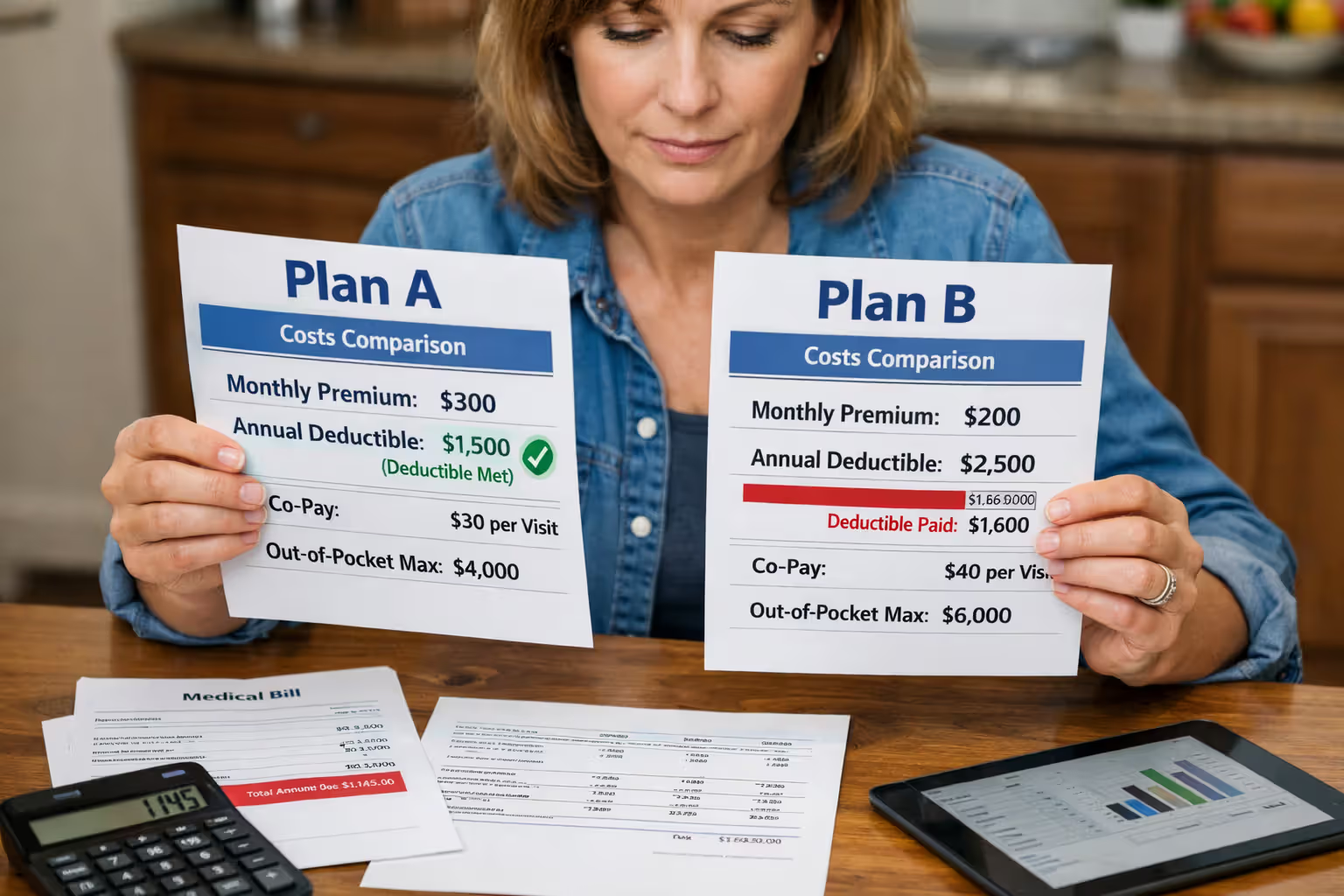

Understanding Your COBRA Deductible

Explaining the cobra coverage deductible means starting with what carries over from your employer plan. Met $1,800 of a $2,000 deductible before your last day? You only owe another $200 under COBRA for the rest of that calendar year. Everything resets January 1, but until then, COBRA picks up right where you left off.

This creates situations where COBRA suddenly makes financial sense despite the sticker shock. Take Jennifer, who loses her job in November after already satisfying her $3,000 deductible and paying $5,500 toward her $7,000 out-of-pocket maximum. She needs knee surgery in December. Under COBRA, she pays just $1,500 more to hit her maximum, then zero for the surgery. Switch to a marketplace plan instead? She'd face a completely new $4,500 deductible and $8,500 out-of-pocket maximum—potentially thousands more in costs for the same surgery.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Every January 1st, though, those counters reset regardless of when you started COBRA. Elect continuation in October with eight months remaining? You'll experience two separate deductible periods: October through December under this year's numbers, then a fresh deductible starting January 1.

Out-of-pocket maximums follow identical logic. Every copay, every coinsurance payment, every dollar toward your deductible from your employment period counts toward your annual maximum. COBRA doesn't wipe that slate clean—you continue climbing toward the same ceiling.

Coverage Limits Under COBRA

When people ask about cobra coverage coverage limits, they're usually asking how long it lasts rather than what benefits get capped. Federal law establishes maximum durations: 18 months following job loss or hour reductions, 29 months if you're deemed disabled, and 36 months for events like divorce or a dependent aging out.

These represent ceilings, not guarantees. Multiple scenarios can cut your COBRA short. Land a new job with health benefits? Your COBRA typically ends, though there are some technical exceptions if the new plan excludes pre-existing conditions (rare under current regulations). Become eligible for Medicare? Your COBRA usually terminates, though your dependents can continue theirs.

Stop paying premiums and you're done, usually after a 30-day grace period following each due date. Premium due April 1st, still unpaid by April 30th? The administrator can cancel everything back to April 1st.

Your former employer going through tough times and eliminating health coverage for everyone? Your COBRA ends too. They should offer alternative coverage if available, but if they simply drop health benefits entirely, your continuation rights disappear with the plan.

Benefit limitations embedded in your plan travel with you to COBRA. Your employer plan limited certain therapies to 20 sessions annually? Still limited under COBRA. Network boundaries don't change either—out-of-network care still costs whatever percentage it cost before.

COBRA Costs and Premium Payment

Brace yourself for COBRA's financial reality check. That $175 monthly deduction from your paycheck? Turns out the full premium was $1,650, and now you're paying all of it. Tack on a 2% administrative surcharge (allowed under federal rules), and your new monthly bill hits $1,683. For family coverage, those numbers can easily double.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Most employees never see the employer's contribution amount because it happens behind the scenes on the balance sheet. You knew your share; you didn't know your boss was kicking in another $1,475 every month. COBRA tears away that curtain, and the view isn't pretty.

That 2% administrative fee covers the plan administrator's costs—sending notices, tracking elections, processing payments, maintaining compliance. Some employers charge less than the 2% maximum or waive it entirely, but most assess the full amount they're legally permitted to collect.

Premium deadlines after that initial 45-day payment window? Generally, first of each month, with a 30-day grace period before termination. Some administrators require payment by the first without any grace period, depending on how the plan is structured. Late payments risk losing everything, and here's the painful part: once terminated for non-payment, you cannot re-elect COBRA for that same qualifying event. You get one shot at continuation coverage.

Payment methods vary wildly by administrator. Some accept only checks mailed to a P.O. box. Others offer online portals. A few allow automatic bank withdrawals. Ask about accepted payment methods when you elect coverage—don't assume your administrator has caught up with 21st-century payment technology.

Now for the strategy some people use: if you're healthy with no immediate medical needs, you could wait until day 58 of your 60-day election period to sign up. Stay healthy during that gap? You elect COBRA at the last possible moment and pay premiums covering the entire period retroactively. Get hurt or sick on day 25? You immediately elect COBRA and your coverage applies backward to day one. This gamble carries real risk—if you're in a car accident before electing, you're betting you can complete paperwork and mail elections while potentially incapacitated. Not for the faint of heart.

Filing a Claim with COBRA Coverage

The cobra coverage claim process works exactly like it did when you were employed, because you're literally on the same insurance plan. Most claims happen automatically without any action from you—your doctor's office submits everything electronically to your insurer.

Visit any provider under COBRA? Hand them your insurance card just like before. Some carriers issue new cards when you elect COBRA; others keep everything the same except a notation in their system. Your member ID and group number typically remain unchanged. Providers verify your active coverage, file claims through their usual channels, and you receive explanation of benefits statements showing what insurance paid and what you still owe.

Seeing a provider who demands full payment upfront? You'll submit claims for reimbursement yourself. Grab a claim form from your insurance carrier's website, attach itemized receipts and bills, and mail or upload everything to the claims department. Include your member ID clearly, along with the group number and patient details.

Reimbursement timelines typically run 30 to 45 days for complete submissions with all necessary documentation. Incomplete claims drag on much longer—forget the provider's tax identification number or skip the itemized statement, and you've just added weeks to the process.

Denied claims? The appeals process mirrors what active employees go through. Your carrier sends written denial explanations with instructions for appealing. Most plans feature multiple appeal levels: internal review by the insurance company first, then external review by an independent organization if the internal appeal doesn't resolve things.

Critical advice: photocopy and save everything. COBRA's administrative complexity means documents occasionally vanish into the bureaucratic void. Provider claims your coverage lapsed? Your premium payment records and election confirmations prove otherwise.

Common COBRA Mistakes to Avoid

COBRA delivers real value in narrow windows—primarily when you've already satisfied a substantial chunk of your deductible and out-of-pocket maximum, or when you're seeing specialists who don't participate in marketplace networks. For someone who lost coverage in February with minimal healthcare spending, marketplace plans typically offer superior value, particularly once you factor in premium subsidies that COBRA doesn't provide under any circumstances

— Rachel Moreno

Letting that 60-day election window close ranks as the single most expensive COBRA mistake. Some folks assume they can decide whenever they're ready, not realizing the opportunity vanishes permanently once those 60 days expire. Others lose the election notice in the chaos of a job transition and forget about it until months later. Day your election notice arrives? Calendar it immediately, with additional reminders at the 30-day, 45-day, and 55-day marks.

Electing COBRA impulsively without crunching the numbers ruins plenty of household budgets. Before you check that election box, calculate your total monthly premium including the 2% fee, multiply by however many months you'll need coverage, and honestly assess whether you can sustain those payments. Then compare that total to marketplace plans—you might find better deals even without subsidies.

Forgetting to notify the plan administrator about qualifying events you control—divorce, legal separation, or a child aging out—within 60 days costs your family members their COBRA rights. Your employer won't discover your divorce through telepathy. The clock starts ticking from the event itself, not from whenever you remember to mention it.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Paying COBRA premiums for several months, then stopping and letting coverage terminate, means you cannot restart it later. COBRA is a single-use election. Elect coverage, pay for three months, stop paying and get terminated? You've exhausted your COBRA rights completely. No second chances, no do-overs.

Electing COBRA automatically without researching alternatives first locks you into expensive coverage when better options might exist right under your nose. Your spouse's open enrollment period, marketplace plans, a new employer's coverage, or even short-term health insurance might cost less while providing adequate benefits. COBRA shines in specific circumstances—you've met your deductible, you need particular providers only in your current network, or you're continuing complex treatment—but it's not the default best answer for everyone.

COBRA vs. Marketplace Insurance: Cost and Coverage Comparison

| Factor | COBRA Coverage | Marketplace Insurance |

| Monthly Premium | $600-$1,800+ (full cost of employer plan plus 2%) | $300-$1,200+ (varies by metal tier; subsidies can slash this substantially) |

| Annual Deductible | Continues from employer plan; resets each January 1 | Starts fresh at $0; typically ranges $1,500-$8,000 based on plan tier |

| Provider Network | Exact same network as employer plan; zero disruption | Different network; may need to switch doctors |

| Enrollment Period | 60-day window following qualifying event notification | Special enrollment period (60 days post-coverage loss) or November-January open enrollment |

| Coverage Duration | 18-36 months based on qualifying event type | Continuous year-round with annual renewals |

| Subsidy Availability | Zero subsidies regardless of income | Premium tax credits available for eligible incomes |

| Pre-existing Conditions | Covered identically to when employed | Fully covered; ACA prohibits all exclusions |

Frequently Asked Questions About COBRA

COBRA works as a temporary bridge, not a permanent solution. Eventually, your continuation period expires, and those premiums strain most budgets long before then. Approach your COBRA election as a financial decision requiring calculation, not as an automatic default choice. Project your healthcare needs across the continuation period, calculate total costs under COBRA versus alternatives, and weigh the value of provider continuity if you've got established relationships with specific doctors.

Received a severance package along with your pink slip? Allocating some of that money toward COBRA premiums might make sense for several months while job hunting. Facing extended unemployment? Marketplace plans with income-based subsidies usually cost significantly less. Lost coverage in November after meeting your deductible? COBRA often provides optimal value through December 31st, after which switching to marketplace coverage makes more financial sense.

That 60-day election window gives you breathing room to explore alternatives—actually use it. Request marketplace plan quotes, calculate subsidies using healthcare.gov's estimator tool, and compare total out-of-pocket costs including both premiums and your expected medical expenses. COBRA's retroactive coverage feature means you can wait until day 58 of your election period to decide, giving you nearly two full months to evaluate alternatives while preserving your option to elect coverage if circumstances change.

Whatever route you choose, act before deadlines slam shut. Miss your COBRA election window or the 60-day special enrollment period for marketplace plans, and you could end up uninsured for months, exposing yourself to both catastrophic financial risk and potential tax penalties in states still requiring health coverage. Mark every deadline clearly, gather information early in your window, and make an informed decision based on your specific medical needs and budget reality.