Young adult comparing health insurance plans on a laptop at home

How to Get Health Insurance in the United States?

Content

Here's what typically happens: you're 25, still on your parents' plan, not worried about insurance. Then your 26th birthday hits. Suddenly you're uninsured, Googling "health insurance" at 11 PM, overwhelmed by acronyms like PPO and HMO, wondering why this process feels harder than filing taxes.

Or maybe you just got laid off. Your HR person mentioned something about "COBRA" that costs $1,800 monthly—more than your rent. Now you're racing against deadlines you didn't know existed.

You need coverage, but the system looks deliberately complicated. It's not, really. Five main routes get you insured, each with specific enrollment windows and price structures. This walkthrough explains which path makes sense for your situation, what the enrollment process actually involves, and how to use your coverage once you've got it—including the claim process that trips people up constantly.

What Health Insurance Is and Why You Need It

Insurance companies operate on a simple premise: collect monthly payments from thousands of people, use that pool of money to pay medical bills for whoever gets sick or injured. You're betting you'll need expensive care; they're betting you won't. When you do need treatment, you pay a small portion (maybe $50 for a specialist visit), they cover the rest (the other $450).

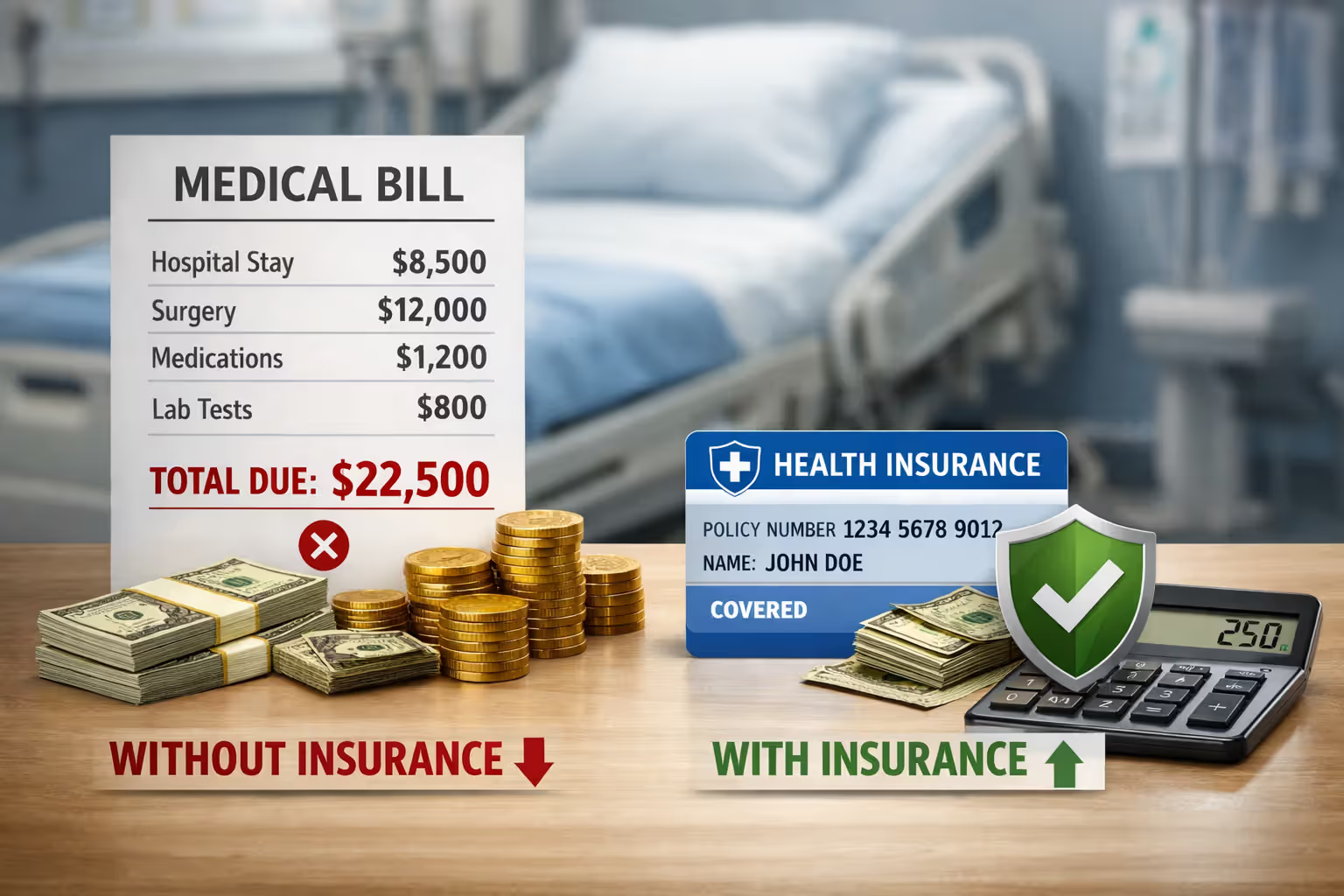

The financial protection matters more than most people realize until they've been hit with medical debt. Emergency appendectomy with three hospital days? You're looking at $28,000-$33,000 without coverage. Break your femur skiing and need surgical repair with hardware? That runs $25,000-$40,000. Chemotherapy for cancer treatment can easily exceed $100,000 annually, sometimes pushing past $1 million over the full treatment course.

Even routine care adds up fast. Take someone managing diabetes—test strips, glucose monitors, endocrinologist visits, insulin, annual eye exams, and kidney function labs total $8,000-$12,000 yearly at full retail prices. Insurance typically reduces your portion to $1,500-$3,000.

The federal penalty for going uninsured disappeared in 2019, dropping to zero nationwide. Five jurisdictions kept their own penalties though: California charges the greater of $850 per adult or 2.5% of household income. Massachusetts hits you with up to $135 monthly. New Jersey, Rhode Island, and DC enforce similar penalties. Beyond avoiding fines, staying insured means you won't skip necessary medical care or face bankruptcy if serious illness strikes.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Types of Health Insurance Plans Available

Insurance plans split into four main categories that balance monthly costs against provider flexibility:

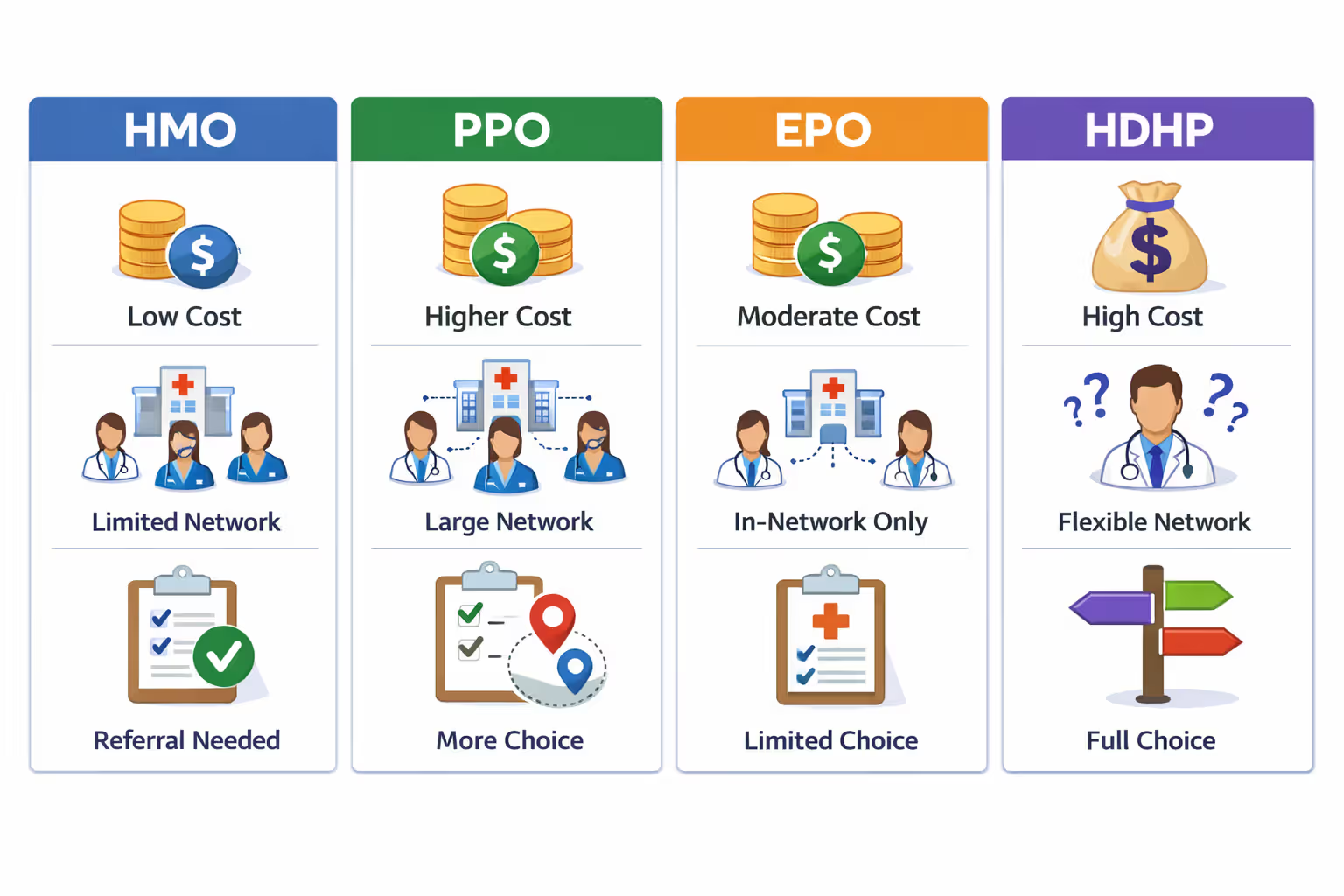

HMO (Health Maintenance Organization) plans come with the lowest premiums—sometimes $200-$300 less monthly than comparable PPOs—but restrict where you can receive care. You'll select a primary care physician who coordinates everything. Need to see a dermatologist about a suspicious mole? Your PCP must write a referral first. Visit an out-of-network doctor (outside emergencies) and you're covering 100% of the bill yourself. These plans work well if you're relatively healthy, don't mind the referral system, and want maximum affordability.

PPO (Preferred Provider Organization) plans cost significantly more—expect $150-$250 higher monthly premiums than similar HMOs—but eliminate most restrictions. See any specialist without referrals. Visit out-of-network providers and still receive partial coverage (typically 50-60% reimbursement instead of the 80-90% you'd get in-network). Pick PPOs when you've established relationships with specific doctors or need flexibility for complex medical conditions requiring multiple specialists.

EPO (Exclusive Provider Organization) plans split the difference. Skip the referral requirements but lose all coverage for out-of-network care except true emergencies. Essentially an HMO minus the primary care gatekeeper.

HDHP (High Deductible Health Plan) options reverse the usual formula. Monthly premiums drop low—sometimes $180-$250 for individuals—while deductibles jump high, ranging from $3,000 to $7,000 before insurance pays meaningfully toward most services. The upside? HDHPs pair with Health Savings Accounts where you can deposit pre-tax dollars, invest the money, and let it grow tax-free for medical expenses. These suit healthy people who can absorb upfront costs or anyone building long-term healthcare savings.

Plans also carry metal tier designations indicating cost-sharing levels. Bronze plans cover approximately 60% of medical costs—you're covering the other 40%. Silver plans hit 70% coverage. Gold plans reach 80%. Platinum plans provide 90% coverage. Lower metal tiers charge less monthly but expose you to higher bills when receiving care.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Every marketplace-sold plan must include ten essential benefit categories: emergency services, hospital admissions, outpatient care, maternity and newborn care, mental health services, substance abuse treatment, prescription drugs, rehabilitative services, laboratory work, preventive and wellness visits, plus pediatric services including dental and vision for children. Preventive care—annual checkups, cancer screenings, vaccines—always comes free with zero copay regardless of whether you've met your deductible.

Where to Get Health Insurance

Five primary channels provide coverage, each serving different populations with distinct eligibility requirements:

Employer-sponsored coverage insures most working Americans because employers shoulder 70-80% of premium costs. When your company offers health benefits, you'll select plans during their open enrollment period, usually spanning 3-4 weeks in October or November. Your premium share gets deducted automatically from paychecks. Adding family members costs extra—count on $250-$600 more monthly for spouse and kids—but remains cheaper than most alternatives.

Healthcare.gov and state marketplaces serve everyone else. These government-run exchanges let you compare plans, check subsidy eligibility, and enroll during the annual open enrollment running November 1 through January 15 nationwide. Fifteen states operate their own exchanges—California runs Covered California, New York has NY State of Health, Colorado operates Connect for Health Colorado, and others—with occasionally different dates and plan offerings.

Medicaid delivers free or low-cost coverage to lower-income individuals earning up to 138% of federal poverty thresholds. For 2026, that means roughly $20,780 for a single person or $43,056 for a family of four. Pregnant women, children, elderly individuals, and people with disabilities qualify at higher income cutoffs. Thirty-nine states plus Washington DC expanded Medicaid under the Affordable Care Act. Twelve states—including Florida, Texas, Wyoming, and Tennessee—haven't expanded, creating coverage gaps for low-income adults. Unlike marketplace insurance, you can apply any month and coverage begins once approved.

Medicare becomes available at 65 for most Americans, plus covers younger individuals with qualifying disabilities or end-stage kidney disease. Part A covers hospital expenses (premium-free if you worked 40+ quarters paying Medicare taxes), Part B handles doctor visits ($174.70 monthly in 2026 for most people), Part D adds prescription drug coverage, and Part C (Medicare Advantage) bundles everything through private insurers. Enroll during your Initial Enrollment Period—a seven-month span starting three months before your 65th birthday month, including that month, plus three months after—or face permanent late-enrollment penalties.

Direct insurance company purchase lets you buy coverage straight from carriers like Blue Cross Blue Shield, Aetna, Cigna, or United Healthcare outside marketplace exchanges. You'll pay full retail without subsidies, making this route 30-60% pricier than employer coverage for comparable benefits. Makes sense when your income exceeds subsidy thresholds but you want a specific plan your employer doesn't offer.

COBRA continuation extends employer coverage for 18 months after leaving a job. Brace yourself for sticker shock—you'll pay the full premium (your old share plus what your employer contributed) plus 2% administration fees. Family coverage frequently runs $1,600-$2,400 monthly. COBRA works as temporary coverage when you need uninterrupted care for ongoing treatment, but marketplace plans almost always cost substantially less.

| Where to Get Coverage | Eligibility Requirements | Monthly Cost | Enrollment Timing | Main Advantage | Primary Drawback |

| Through your employer | Must work for participating business | You pay 15-30%, employer covers rest | During company's benefits enrollment | Employer pays majority of premiums | Limited to plans your company selected |

| Marketplace exchanges | Open to anyone lacking affordable workplace coverage | Full cost minus income-based subsidies | Nov 1-Jan 15 each year | Subsidies can reduce premiums dramatically | Must renew subsidies annually |

| Medicaid program | Income below state thresholds | Usually $0-$20 monthly | Any time during year | Minimal to zero premiums and deductibles | Provider networks sometimes restricted |

| Medicare coverage | Age 65+ or disability status | $0-$200+ based on which parts | Seven months surrounding 65th birthday | Comprehensive coverage for seniors | May need supplemental plans for gaps |

| Direct from insurers | Anyone willing to pay | Full retail pricing | Available year-round | Get coverage immediately | Costs 50-100% more than subsidized plans |

Step-by-Step Process to Enroll in Health Insurance

Securing coverage involves similar steps regardless of which channel you're using, though deadlines and documentation vary:

First, identify which coverage options you can access and when. Check with your employer first—if they provide benefits, that's usually your best financial option. No workplace coverage available? Go to Healthcare.gov and complete the eligibility screener to see if you qualify for Medicaid or premium subsidies. Mark November 1 through January 15 on your calendar for marketplace enrollment. Outside this window, you'll need a qualifying life event to enroll—marriage, childbirth, losing existing coverage, or moving states all trigger special enrollment periods.

Second, gather required documentation. You'll need Social Security numbers for everyone seeking coverage, income verification (recent pay stubs, W-2 forms, or prior year's tax return), immigration documents if applicable, and information about current coverage if you have any. For marketplace applications, your most recent Form 1040 speeds up subsidy calculations since they're based on projected yearly income.

Third, compare plans beyond just the monthly premium. This trips up more people than anything else—they see Bronze at $240/month versus Gold at $430/month and grab the Bronze automatically. Calculate total annual exposure: Bronze at $240 monthly equals $2,880 in premiums plus a $6,800 deductible, putting you at $9,680 before meaningful coverage kicks in. If you take daily medications or visit doctors regularly, you might hit that deductible. Compare with Gold at $430/month equaling $5,160 yearly plus a $1,800 deductible—total $6,960 before comprehensive coverage starts. If you'll use healthcare services, Gold saves you money despite higher monthly costs.

Fourth, verify your providers participate in the network. Insurance company directories frequently contain outdated information—doctors appear as "in-network" months after dropping the contract. Call your doctor's billing department directly and confirm they accept the specific plan you're considering. Do the same for hospitals you'd likely use, particularly if you're planning surgeries. Also confirm your prescriptions appear on the plan's formulary and check which cost tier they're in.

Fifth, complete and submit your enrollment application. Marketplace applications consume 25-50 minutes through Healthcare.gov or your state exchange website. Employer enrollment happens through your company's benefits portal or third-party administrator. Select your plan, add dependents who need coverage, and choose your effective date. Coverage typically starts the first of the month following enrollment if you enroll by the 15th of the prior month; enroll after the 15th and your start date pushes back another month.

Sixth, pay your first premium. Your enrollment means nothing until you've paid. Expect your initial invoice within 7-14 days after enrolling. Set up automatic payments to avoid accidentally missing a premium and losing coverage.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

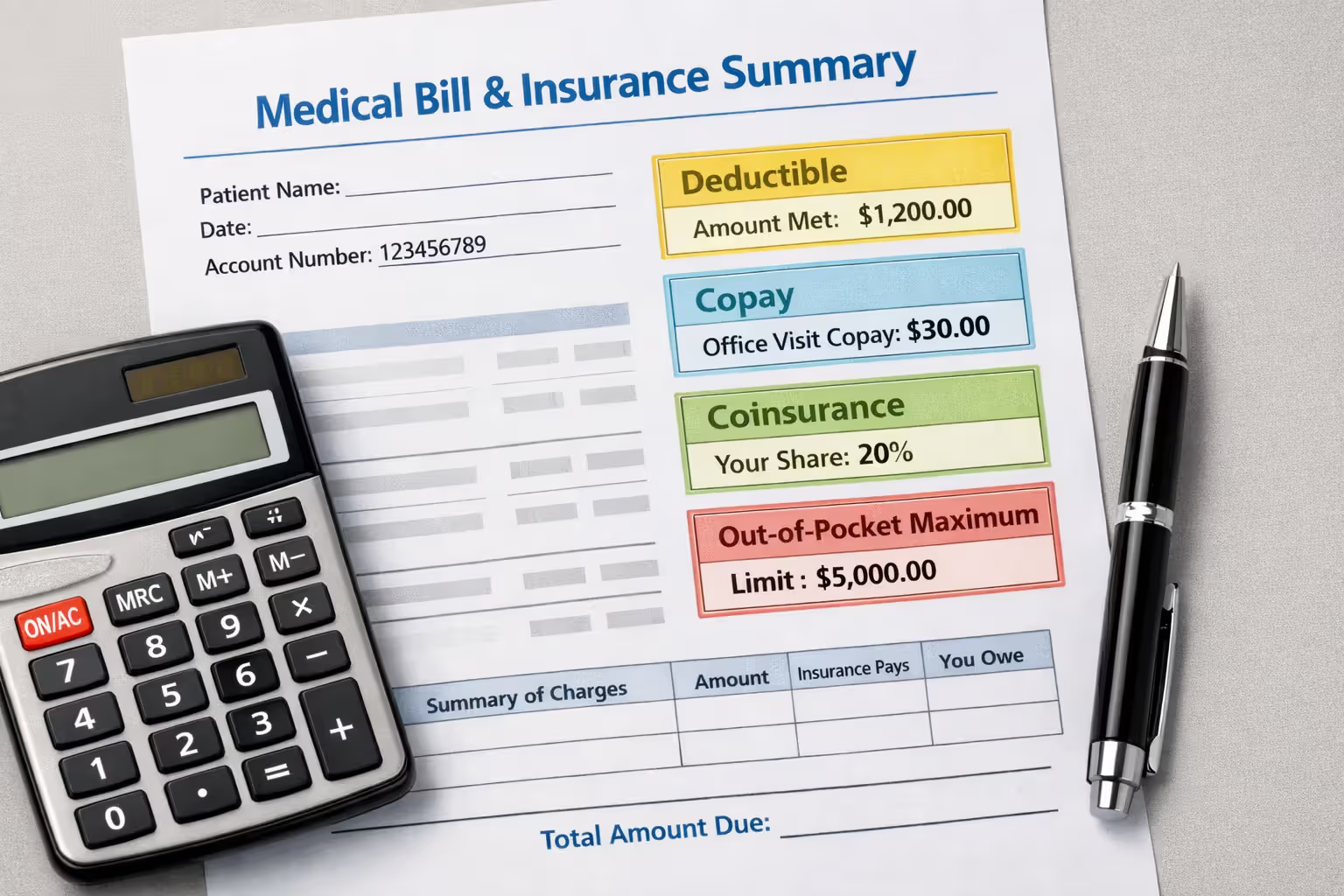

Understanding Deductibles and Out-of-Pocket Costs

Your deductible represents the dollar amount you'll pay each year before insurance starts covering the bulk of medical expenses. Consider a plan with a $3,000 deductible—you'll personally cover the first $3,000 in doctor appointments, lab work, and procedures (preventive care excluded, always free). After you've spent that $3,000, your responsibility shifts to copays and coinsurance for most services.

Copays are fixed amounts for particular services—$30 to see your primary physician, $60 for specialists, $15-$120 for prescriptions depending whether they're generic, preferred brand, or specialty drugs. Copays don't count toward your deductible but do accumulate toward your annual out-of-pocket maximum.

Coinsurance represents your percentage of costs after satisfying the deductible. With 20% coinsurance, a $1,200 CT scan costs you $240 while insurance pays $960. Bronze plans frequently charge 40-50% coinsurance; Platinum plans might charge only 10-15%.

Your out-of-pocket maximum caps what you'll spend annually on covered care. Federal regulations limit these to $9,450 for individuals and $18,900 for families in 2026, though many plans set lower caps—often $6,000-$7,000 for individuals. Reach that ceiling and insurance covers 100% of covered services through December 31st. This protection becomes critical during serious illness—cancer treatment or multiple surgeries can generate $200,000-$500,000 in bills, but your maximum exposure stays capped at the out-of-pocket limit.

One important caveat: everything resets January 1st. Meet your deductible in late December? You'll start from zero again in two weeks. This timing influences healthcare planning—if you've satisfied your deductible in November or December, schedule elective procedures before year-end to avoid paying a new deductible.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Coverage Limits and What's Included

The Affordable Care Act eliminated lifetime and annual dollar limits on essential health benefits, meaning insurers can't terminate coverage after $1 million in cancer treatment or cap you at $75,000 yearly. This protection proves crucial for people with chronic conditions, catastrophic injuries, or serious illnesses requiring extended treatment.

Insurers still impose limits through other mechanisms though. They might restrict physical therapy to 25-35 visits annually, limit outpatient mental health sessions, or require prior authorization before approving expensive prescriptions, imaging scans, or surgeries. Service restrictions vary dramatically between plans, so review the Summary of Benefits and Coverage carefully if you need particular ongoing treatments.

All marketplace plans include these ten essential benefit categories: outpatient services, emergency care, hospitalization, maternity care and delivery, mental health and substance abuse services, prescription medications, rehabilitation services, laboratory services, preventive and wellness care, and pediatric services including dental and vision for kids under 19.

Preventive services receive special protection under federal regulations—insurers must provide annual physicals, cancer screenings, immunizations, and preventive services at zero cost with no copay and no deductible requirement. This covers mammograms, colonoscopies, blood pressure screenings, diabetes tests, contraception, and dozens of other services. Use these no-cost benefits to catch health issues early.

Common exclusions across most plans include cosmetic procedures (unless medically necessary following injury or reconstruction), adult dental and vision care, hearing aids, long-term nursing home care, and experimental treatments lacking FDA approval. Some plans exclude complementary medicine like acupuncture or chiropractic care; others cover them with visit limitations. Medical services received outside the United States typically aren't covered except genuine emergencies.

How Health Insurance Works After You Enroll

Once your coverage becomes active, using your benefits effectively requires understanding operational details that confuse many people.

Your insurance card shows your member ID number, group number (for employer plans), copay amounts for typical services, and customer service phone numbers. Bring this card to every doctor appointment, pharmacy visit, and hospital admission. Medical offices scan or copy it to verify your coverage and submit claims to your insurer.

Locating in-network doctors and facilities substantially impacts your costs. Your insurer's website includes searchable directories organized by specialty, location, and facility type. When booking appointments, confirm the provider accepts your specific plan and verify the facility itself contracts with your insurer—sometimes doctors with privileges at out-of-network hospitals generate surprise bills even when the doctor is in-network. For scheduled procedures, triple-check that your surgeon, anesthesiologist, any consulting specialists, and the facility all participate in your network.

Claims processing usually happens behind the scenes without your involvement. After you receive care, your provider electronically transmits a claim to your insurer detailing services provided and billed charges. Your insurance company reviews the claim, applies contracted rates (often 40-65% below the provider's list price), determines coverage based on your benefits, and calculates your portion using your deductible, copays, and coinsurance. You'll receive an Explanation of Benefits (EOB) showing what the provider originally billed, the contracted rate, what insurance paid, and your responsibility. The EOB isn't a bill—your provider bills you separately for your share.

Claims processing takes anywhere from two weeks to ninety days depending on complexity. Claim denials happen regularly, but you've got appeal rights. Common denial triggers include services deemed "not medically necessary," out-of-network providers when you believed they were in-network, missing prior authorization, or simple billing code errors. Call customer service on your card to understand why they denied the claim and what documentation might overturn the decision. Your doctor's office can help by submitting clinical notes or letters explaining medical necessity.

Prior authorization requirements mandate advance approval before receiving certain services—typically expensive drugs, imaging like MRIs or PET scans, surgeries, or specialty treatments. Your doctor's office normally handles this paperwork burden by faxing clinical documentation justifying why you need the service. Approvals can take 2-14 business days, so factor this delay into scheduling non-emergency procedures. Receiving services without required authorization often results in the insurer denying the entire claim, leaving you with bills potentially reaching tens of thousands of dollars.

Prescription drug coverage operates through formularies—tiered lists of covered medications. Tier 1 generics cost $5-$20 per prescription, Tier 2 preferred brands run $35-$70, Tier 3 non-preferred brands cost $80-$175, and Tier 4 specialty drugs can require 25-33% coinsurance potentially reaching hundreds or thousands monthly. If your medication lands in an expensive tier or isn't covered at all, ask your doctor about therapeutic substitutes in lower tiers. Many insurers offer mail-order pharmacy services delivering 90-day supplies at reduced copays compared to monthly refills at retail pharmacies.

People treat health insurance like they treat car insurance—purchase it and forget about it until something breaks. That mindset costs money. Smart insurance use means actively managing benefits: knowing coverage details inside out, staying in-network, maximizing free preventive services, and appealing denied claims when insurers make mistakes

— Sarah Thompson

Common Mistakes When Getting Health Insurance

Even careful shoppers stumble over these frequent errors:

Missing enrollment deadlines leaves you uninsured for extended periods. Marketplace open enrollment lasts only 10-11 weeks yearly. Set multiple phone reminders starting in October and don't wait until mid-January—rushed applications contain mistakes that delay coverage. Miss the deadline completely and you'll need a qualifying life event to access special enrollment.

Choosing plans based solely on monthly premiums backfires when you need medical care. That Bronze plan charging $235/month looks attractive until you're facing a $6,500 deductible. Calculate total yearly exposure by adding premiums to anticipated medical expenses based on your health situation. Take four prescriptions monthly and see specialists quarterly? Mid-tier Gold plans often cost less overall despite higher monthly premiums.

Ignoring subsidy eligibility leaves thousands of dollars on the table. Approximately half of marketplace enrollees qualify for premium tax credits reducing monthly costs, sometimes below $75. The subsidy calculator at Healthcare.gov takes under five minutes and could save $250-$450 monthly. Income thresholds are surprisingly high—a family of four earning up to $120,000 might qualify for assistance in 2026.

Skipping provider network verification creates surprise medical bills. That orthopedist your primary doctor recommended might not contract with your plan, costing you thousands extra. Always verify network participation before scheduling appointments, and reconfirm the morning of your visit—provider networks change mid-year as insurers renegotiate contracts.

Underestimating healthcare needs leaves you financially vulnerable. Healthy people in their 30s often grab minimal plans assuming they won't need medical attention, then face financial disaster when a motorcycle accident, sudden appendicitis, or unexpected cancer diagnosis occurs. Anyone can become sick or injured regardless of age or fitness level. Balance optimism about your health with realistic financial protection.

Forgetting to update marketplace applications when income shifts creates tax-time problems. Get a promotion or new job mid-year? Report income changes to the marketplace within 30 days. The system adjusts your subsidy to prevent owing back thousands when filing taxes the following April.

Frequently Asked Questions About Getting Health Insurance

Getting health insurance in America requires navigating multiple pathways with distinct rules, but the core process follows predictable patterns: determine which coverage channels you can access, evaluate options during specific enrollment periods, understand the cost-sharing structure of your selected plan, and use coverage strategically once active.

Start by checking employer coverage availability, since workplace plans typically deliver the best value. Without employer access, explore marketplace plans where income-based subsidies often make quality coverage affordable, or pursue Medicaid if your earnings qualify. Don't let decision paralysis prevent enrollment—even Bronze-tier coverage protects you from medical bankruptcies that devastate household finances following serious illness or accidents.

Mark November on your calendar for annual open enrollment, gather necessary paperwork in advance, and evaluate plans based on total yearly spending rather than focusing exclusively on monthly premiums. Confirm your preferred doctors and hospitals participate in the plan's network, understand your deductible and out-of-pocket maximum clearly, and take advantage of free preventive care services.

Going without coverage carries serious consequences—delayed medical treatment, crushing debt from unexpected health crises, and persistent anxiety about one accident derailing your financial security. The effort invested in securing coverage pales compared to these risks. With the information in this guide, you're equipped to make informed decisions protecting both your health and financial stability.