Car sale with keys and insurance documents being exchanged

When to Cancel Insurance After Selling Car?

Content

You've found a buyer for your car and agreed on a price. Great! But here's where many sellers trip up: they either cancel their insurance immediately—thinking they're done—or forget about it entirely and keep paying for months. Neither approach works out well. The real question isn't whether to cancel, but exactly when. Get this timing wrong and you're either exposed to serious liability or throwing money away on coverage for a car sitting in someone else's driveway.

Why Timing Matters When Canceling Car Insurance

That stretch of time between shaking hands on a deal and watching the new owner drive away? It's messier than most people realize. Your insurance stays active, which sounds good until you're paying $80-$120 for another month you didn't need.

Here's the problem with jumping the gun: let's say you cancel Tuesday morning, and that afternoon a buyer takes your car for a test drive and rear-ends someone at a stoplight. Guess who's getting the lawsuit? In most states, you're still the registered owner until the DMV processes that title transfer. No insurance means you're covering those medical bills and car repairs out of pocket—we're talking potentially $50,000 to $100,000 or more.

Your state doesn't care that you "sold" the car. Registration records show it's yours, and that means you need active coverage. Period. California will suspend your license for coverage lapses. New York hits you with registration holds. Florida charges reinstatement fees up to $500. These penalties stick around even after you explain you'd already sold the vehicle.

But wait too long and watch your money vanish. Your cousin canceled his policy three weeks after selling his truck—turned out the buyer registered it the same day. He paid $95 in premiums for coverage on a vehicle he hadn't owned for 21 days. Insurance companies don't refund based on when you stopped owning the car; they refund from your cancellation date.

The math gets worse with refund penalties. When you cancel mid-policy, some insurers use "short-rate" cancellation—they keep 10-20% as an administrative fee. So that $300 refund you expected? Now it's $240-$270. Other companies offer "pro-rata" refunds, returning every penny of unused premium. Which one you get often depends on whether you're buying another policy with them.

Each state writes its own rules here, naturally making things more complicated. California mandates 10 days' notice before cancellation takes effect unless you're replacing the car. New York won't let you cancel without showing proof of sale or registration transfer. Mess these up and you'll spend hours on the phone untangling bureaucratic knots.

Author: Caroline Halstead;

Source: talero.spotpariz.net

The Right Time to Cancel Your Policy After a Sale

How you're selling determines when you can safely pull the plug on coverage. Selling to your neighbor looks different than trading in at a dealership.

Private Sale Timeline

With private sales, you're waiting on the buyer to handle DMV paperwork—and people procrastinate. Smart sellers keep insurance active until they've confirmed (not assumed) that the title transferred.

Here's your playbook: Finalize the sale. Remove your plates if your state requires it (about 20 states make plates stay with the owner). Hand over the signed title and bill of sale. Then wait. Don't cancel yet.

Check your state DMV's website—most now let you track title transfers online. Michigan shows it within 24-48 hours. Texas takes up to two weeks. Once you see the new owner's name on the registration, you're clear. Call your insurer that day.

Now here's a money-saving trick: Most insurance companies will backdate your cancellation to the actual sale date if you ask and provide documentation. Sold your car on March 3rd, but the buyer didn't register it until March 17th? Request cancellation effective March 3rd and submit your bill of sale as proof. You'll get those two weeks of premium refunded. Not every insurer allows this, but it's worth asking—we're talking $40-$70 back in your pocket.

What if the buyer never registers it? Keep following up. After 30 days, file an abandoned vehicle report with your local police and submit a Notice of Transfer to your DMV. This officially removes the car from your record even if the buyer ghosted the registration process.

Author: Caroline Halstead;

Source: talero.spotpariz.net

Trade-In or Dealer Sale Timeline

Dealerships make this simpler because they process title work immediately—it's literally part of their business model. When you sign over the title at the dealer, they assume ownership right then.

Before leaving the lot, grab your bill of sale showing today's date. Many dealers print this automatically with their final paperwork. Some will even call your insurance company for you as a courtesy, though don't count on it—they're salespeople, not your personal assistant.

You can cancel same-day with a trade-in. I've done it from the dealership parking lot: called my insurer, told them I just traded the car, read them the VIN from my bill of sale, and had cancellation confirmed in eight minutes. Refund check showed up 12 days later.

Buying a replacement vehicle the same day? Tell your agent to transfer coverage to the new car first, then cancel the old policy. This seamless handoff prevents any gap and usually gets you better refund treatment. Plus, most states give you 14-30 days to add a new car to existing coverage, so you're protected driving it home regardless.

| Scenario | When to Cancel | Required Documentation | Refund Timeline |

| Private sale with immediate buyer registration | Same day after verifying DMV transfer online | Bill of sale, title copy, screenshot of DMV transfer confirmation | 14-30 days |

| Private sale with delayed buyer registration | After confirming registration (check DMV portal weekly) | Bill of sale, documentation of buyer's new registration | 14-30 days |

| Trade-in at dealership | Same day you complete transaction | Dealer's bill of sale showing transaction date | 10-21 days |

| Dealer purchase replacing your vehicle | Transfer to new vehicle first, then cancel old policy immediately | Registration for new car, dealer transaction documents | 10-21 days |

How the Insurance Cancellation Process Works

Calling your insurance company and saying "I sold my car" won't cut it. They need proof, and they're particular about what counts.

Round up your paperwork first: bill of sale with the date, buyer's name, and purchase price. Copy of the title showing your signature in the seller spot. If you've got it, confirmation from the DMV that registration transferred. Some states give you a tear-off portion of the title certificate specifically for keeping sale records—that works perfectly.

Author: Caroline Halstead;

Source: talero.spotpariz.net

Now contact your insurer. Some still take phone calls for cancellations (State Farm, Allstate generally do), but many now push you to their website portal or mobile app. Progressive and GEICO both require written requests through their platforms. Have your policy number ready, along with the VIN.

Be specific about your cancellation date. Don't say "I sold it last week"—give them the exact date from your bill of sale. Want it backdated? Say so upfront: "I'm requesting cancellation effective March 15th, which is the sale date shown on my bill of sale."

Upload or email your documents immediately. Waiting three days to send proof can push your cancellation date forward, costing you those three days of premium. Most insurers give you a dedicated email address or portal upload option specifically for cancellation documents.

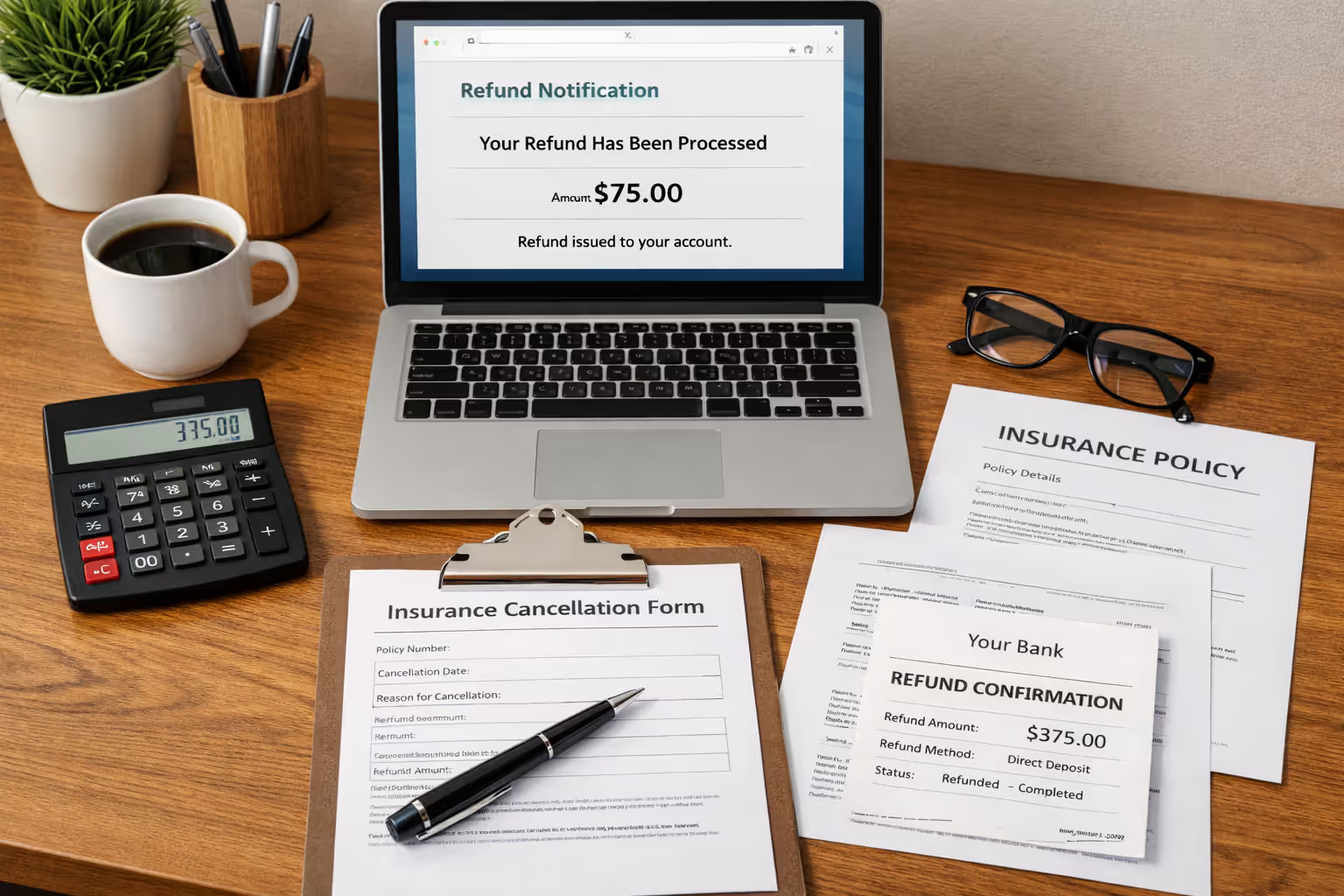

Within 24-72 hours (business days), you'll get written confirmation. Review it carefully. Does the effective date match what you requested? Is the refund amount what you calculated? My sister caught an error where they'd listed the wrong cancellation date, shorting her refund by $63. One quick call fixed it.

Refund checks typically arrive 10-30 days after confirmation. Timeline varies by company—USAA tends to be fastest at 7-10 days, while smaller regional carriers sometimes take the full month. Some insurers offer direct deposit if you'd set up bank information previously, which cuts 5-7 days off delivery time.

Insurance doesn't cancel itself when you sell a car—that's a dangerous myth. You need to actively contact your company with documentation proving the sale. We see thousands of complaints annually from consumers who assumed cancellation was automatic and ended up paying for months of unnecessary coverage or, worse, driving their next vehicle thinking they had coverage when the old policy was still active on the sold car

— Jennifer Hartman

What Your Policy Covers Until Cancellation

Don't make assumptions about what's covered during that transition period—some scenarios might surprise you.

Test drives with potential buyers? Covered under your liability insurance. If someone test driving your Honda Civic slides through a stop sign and T-bones another car, your policy handles the claim up to your liability limits. But—and this is crucial—only while you still legally own the vehicle. Sign that title over and your coverage stops, even if the policy hasn't officially canceled yet.

That gap between sale completion and title transfer is where things get weird. You've handed over the keys, accepted payment, and signed the title. But DMV records still show you as the owner. Most states follow the "registered owner" rule for liability, meaning if that buyer crashes on their way home and hasn't registered the car yet, you could still get pulled into the mess. Your insurance would likely respond since you're technically still the owner on paper. This exact situation is why you maintain coverage until confirmed transfer.

The new owner driving your former car after taking possession? Not covered by your policy, even if the title hasn't transferred. Your insurance covers you and permitted drivers while you own the vehicle. Once you've completed the sale and they've driven away, they need their own coverage. If they crash it that evening, your policy won't pay their claim.

Comprehensive and collision coverage ends the moment you cancel. Let's say you cancel Tuesday, but the title doesn't transfer until Thursday. If the car gets stolen Wednesday night, you're out of luck—no claim, no payout. This creates a narrow risk window for private sales where you're maintaining liability coverage for legal reasons but have no physical damage protection.

Your limits stay unchanged until that cancellation processes. Carried $250,000 in liability? That's your coverage amount for any incidents right up until cancellation takes effect. Same with deductibles—if something happens the day before cancellation and you need to file a claim, you'll still pay your full $500 or $1,000 deductible.

Common Mistakes to Avoid When Canceling Coverage

People make the same errors repeatedly, and it costs them. Skip these traps.

Canceling before title transfer completes is the biggest blunder. You assume the buyer will register it "soon," so you cancel the day of sale to maximize your refund. Then three weeks pass. Four weeks. You're now the registered owner of an uninsured vehicle, violating state law. Worse, if the buyer crashes it, you're facing liability as the legal owner with zero insurance coverage. I know someone who paid $18,000 to settle an accident claim in exactly this scenario.

Not getting written refund confirmation leaves you guessing. Always request documentation showing the refund amount and when you'll receive it. Without this, you can't prove what the company promised if the check never arrives or comes up short.

Forgetting to notify your DMV separately causes headaches for months. Insurance cancellation doesn't automatically tell the DMV you sold the vehicle. In Virginia, California, Texas, and about 30 other states, you must file a "Notice of Transfer and Release of Liability" within 5-10 days. Skip this and you'll get parking tickets, toll bills, and red light camera citations for a car you haven't owned in weeks. One guy I know accumulated $450 in tickets because he ignored this step.

Assuming the policy cancels itself when you stop payments creates a different nightmare. Insurance companies don't immediately cancel for non-payment. They send notices. Apply late fees. Eventually cancel with a "lapse due to non-payment" notation on your record. That lapse can spike your next insurance rate 25-50%—costing you $300-$700 more per year for three years. It's literally cheaper to cancel properly than ghost your payments.

Canceling without securing your next policy first creates a gap that haunts your rates. Even 30 days without coverage classifies you as "high risk" to insurers. Planning to buy another car next month? Keep your current policy active or start a new one immediately. That gap can cost you $200-$500 extra annually for the next three years—far more than you'd save by canceling early.

Leaving license plates on the car in states where plates belong to the owner, not the vehicle. About 20 states (including Pennsylvania, New York, and Ohio) require you to keep your plates. If you leave them on and the buyer racks up toll violations or parking tickets, you're getting those bills. Remove plates before the buyer leaves your driveway.

Author: Caroline Halstead;

Source: talero.spotpariz.net

Getting a Refund on Your Premium

Getting money back sounds straightforward until you hit the fine print about refund calculations.

Pro-rata refunds return your exact unused premium—the fair method. Paid $900 for six months of coverage but canceling after four months? You get $300 back, simple as that. Most insurers use this calculation when you cancel for legitimate reasons like selling your vehicle, provided you submit proper documentation.

Short-rate refunds penalize you by keeping 10-20% as an administrative fee. Instead of that $300, you'd get $240-$270. Companies apply this when they view the cancellation as "voluntary without qualifying reason," or if you've canceled multiple policies with them recently. They argue the penalty covers their acquisition costs and administrative work. Always ask which method applies before finalizing your cancellation—it's often negotiable if you're firm about it.

Deductibles don't directly reduce your refund calculation, but they matter if you've got pending claims. Filed a collision claim last week and the adjuster hasn't settled it yet? The insurer might hold back your deductible amount from your refund until they close that claim. Once they finish processing it and cut the repair shop a check, they'll send your remaining refund separately.

Processing timeframes vary wildly. I've received refunds in nine days from one company and waited 38 days for another. Most fall in the 14-30 day range after cancellation confirmation. State laws set maximum timeframes—California requires refunds within 30 days, Texas allows 60 days, New York mandates 45 days. If you're past the deadline, call customer service and mention your state's insurance code section (they hate this because it signals you might file a formal complaint).

How you paid affects how you get refunded. Paid by check or cash? You're getting a check mailed to your address. Credit card payments sometimes get credited back to your card, though many insurers still issue checks even for card payers. Set up automatic payments? Expect a check unless you specifically enrolled in direct deposit for refunds.

Your state's regulations make substantial differences. New York and California prohibit short-rate cancellations for personal auto policies, requiring pro-rata refunds for all customer-initiated cancellations. Other states let insurers choose their method. Florida, Texas, and Georgia allow more insurer discretion. Knowing your state's rules helps you push back if they try applying a penalty when they shouldn't.

Author: Caroline Halstead;

Source: talero.spotpariz.net

Frequently Asked Questions About Canceling Car Insurance After Selling

Selling your car involves more moving parts than just negotiating a price and collecting payment. The insurance piece trips up even experienced car owners because it requires balancing legal protection against unnecessary costs.

The safest approach? Prioritize protection over saving a few days of premium. Keep coverage active until you've confirmed—actually verified, not just assumed—that the buyer registered the vehicle. Then cancel immediately with documentation ready. You'll eliminate liability exposure while still getting a refund for unused coverage.

Save copies of everything: bill of sale, title, cancellation confirmation, refund documentation. These records protect you if disputes arise about ownership, liability for violations the new owner commits, or refund amounts. They also prove continuous coverage history when you buy your next vehicle, which keeps your rates low.

Between cars right now? Consider your timeline. Buying another vehicle within 30 days? Canceling creates a coverage gap that insurance companies penalize heavily—sometimes adding $300-$600 to your annual premium for the next three years. That's far more than you'd save by canceling early. Some insurers offer suspended coverage or storage rates that maintain your policy at reduced cost while you're not actively driving, preserving your continuous coverage record without paying for full protection you don't need.

Spending 10 minutes to properly time your cancellation and gather documentation can save you hundreds of dollars and prevent legal complications that take months to resolve. Treat the insurance cancellation with the same attention you gave the sale itself, and you'll close this chapter cleanly—with money back in your account and no bureaucratic loose ends creating future headaches.