Person looking worried while reviewing a car insurance bill at home

Why Is My Car Insurance So High?

Content

Staring at your car insurance bill and wondering where all those extra dollars went? You're not alone. Millions of American drivers face sticker shock when they see their premiums—and the reasons aren't always obvious. Your rate reflects a complex calculation that weighs dozens of factors, some within your control and others completely beyond it.

Insurance companies use sophisticated algorithms to predict risk, and even small changes in your profile can trigger significant rate adjustments. Understanding what drives your premium higher empowers you to make informed decisions about coverage and identify opportunities to reduce costs.

Common Factors That Raise Your Car Insurance Rates

Car insurance pricing operates on risk assessment. Insurers analyze your likelihood of filing a claim and price accordingly. The question "why is my car insurance so high" usually traces back to several interconnected factors.

Your age plays a substantial role. Drivers under 25 typically face premiums two to three times higher than middle-aged drivers because statistics show younger motorists have more accidents. Senior drivers over 70 also see increases as reaction times slow and accident rates climb.

Your driving record acts as a direct window into your risk profile. A single at-fault accident can raise rates for three to five years. Multiple violations signal pattern behavior that insurers price aggressively.

Location matters more than most people realize. Your ZIP code determines exposure to theft, vandalism, uninsured motorists, weather events, and litigation trends. Someone driving the same car with an identical record can pay vastly different premiums simply by living across a state line.

Credit-based insurance scores affect rates in most states. Insurers have found statistical correlations between credit behavior and claim frequency, though the relationship remains controversial. A drop in your credit score can trigger premium increases even with a spotless driving record.

The vehicle you drive influences replacement costs, repair expenses, safety performance, and theft attractiveness. A $70,000 luxury sedan costs more to insure than a $25,000 economy car, but the relationship isn't always linear—some affordable models have surprisingly high rates due to theft popularity or expensive parts.

Coverage levels you select directly impact premiums. Higher liability limits, lower deductibles, and additional protections like comprehensive and collision coverage all increase what you pay. Many drivers unknowingly carry coverage configurations that don't match their actual needs.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

How Your Driving History Affects Your Premium

Insurance companies view your past driving behavior as the strongest predictor of future claims. Every interaction with law enforcement and every accident gets recorded and weighted in your rate calculation.

At-fault accidents deliver the biggest premium hit. Expect increases of 40-60% after causing a collision, with the surcharge lasting three to five years depending on your state and insurer. Rear-ending someone at a stoplight can cost you thousands in extra premiums over time, far exceeding the immediate claim payout.

Moving violations carry varying weight. A simple speeding ticket 10 mph over the limit might raise your rate 15-25%, while reckless driving or excessive speed can double your premium. DUI convictions represent catastrophic events for insurance pricing—expect rate increases of 80-100% or more, and some insurers will drop you entirely, forcing you into high-risk markets.

Claims history extends beyond accidents. Filing multiple comprehensive claims for theft, vandalism, or weather damage signals higher risk even when you weren't at fault for any collision. Some insurers apply surcharges after just two claims in three years, regardless of type.

Years of licensed driving experience work in your favor. A 30-year-old with 14 years of driving history pays less than a 30-year-old who just got licensed, even with identical recent records. Insurers reward the stability that comes with experience.

Gaps in coverage create red flags. If you let insurance lapse even briefly, you'll face higher rates when you return to the market. Continuous coverage demonstrates responsibility and often unlocks loyalty discounts.

Coverage Types and Limits That Increase Costs

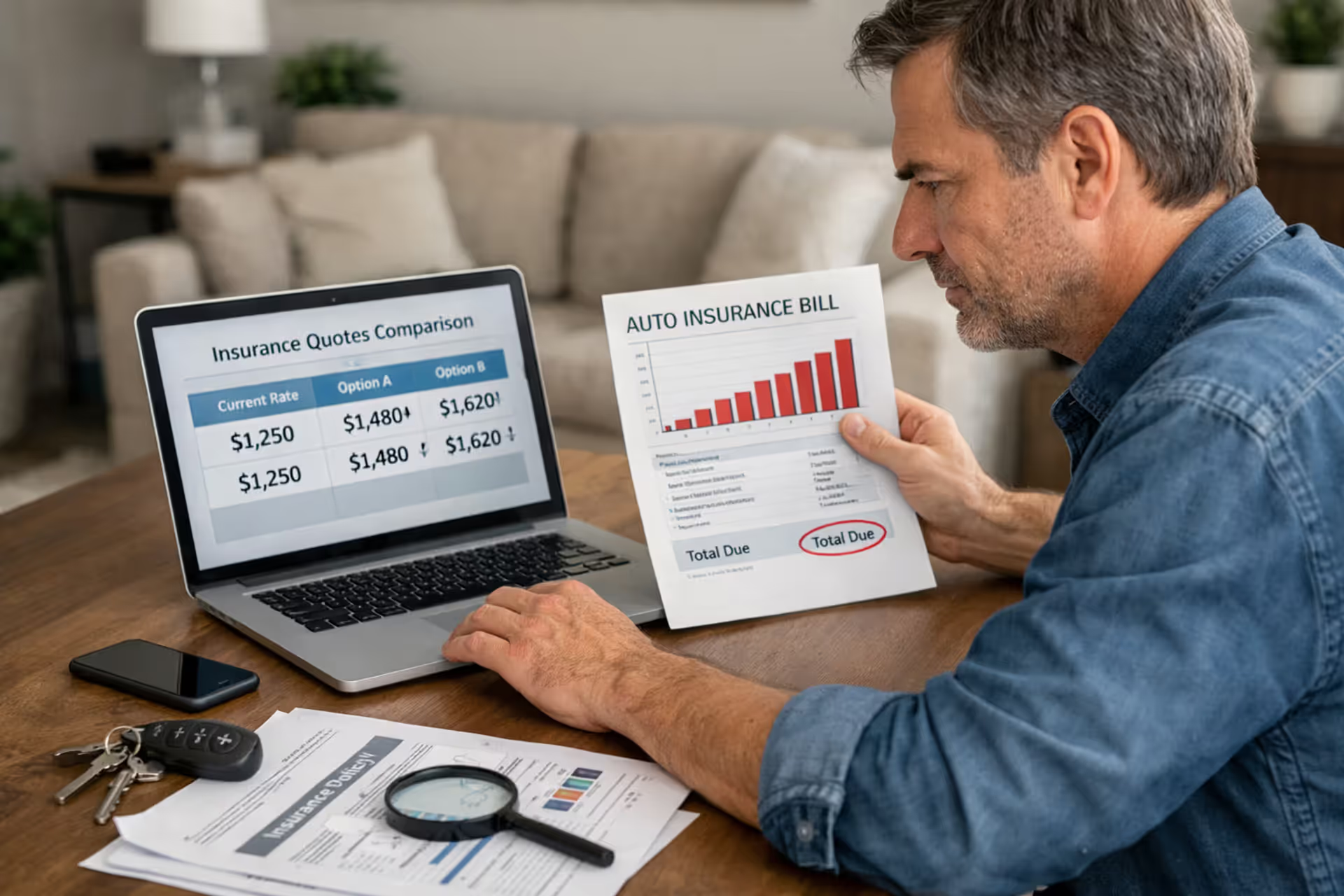

Understanding what does why is my car insurance so high cover requires examining each component of your policy. Most drivers carry several distinct coverage types bundled together, each adding to the total premium.

Liability coverage forms the foundation. This pays for damage and injuries you cause to others. State minimums often sit at 25/50/25 ($25,000 per person for injury, $50,000 per accident, $25,000 for property damage), but these limits leave you exposed to lawsuits. Increasing to 100/300/100 or higher adds cost but provides crucial protection. The premium difference between minimum and adequate coverage often surprises people—it's usually less than they expect.

Collision coverage pays to repair your vehicle after an accident regardless of fault. This coverage gets expensive for newer, valuable vehicles because the potential payout is higher. If you drive a 12-year-old car worth $3,000, paying $800 annually for collision coverage makes little financial sense.

Comprehensive coverage handles non-collision events: theft, vandalism, fire, flooding, hail, animal strikes. Your location heavily influences this cost. Park your car on a street in a high-theft urban neighborhood and comprehensive coverage will cost significantly more than garaging it in a rural area.

Uninsured/underinsured motorist coverage protects you when someone without adequate insurance hits you. In states where 15-20% of drivers lack insurance, this coverage becomes essential but adds to your premium.

Personal injury protection (PIP) or medical payments coverage handles your medical bills after an accident. Requirements vary by state, with no-fault states mandating PIP coverage that can substantially increase premiums.

Why is my car insurance so high coverage limits directly correlate with premium costs. Doubling your liability limits doesn't double your premium—the increase is usually modest—but each enhancement adds incremental cost.

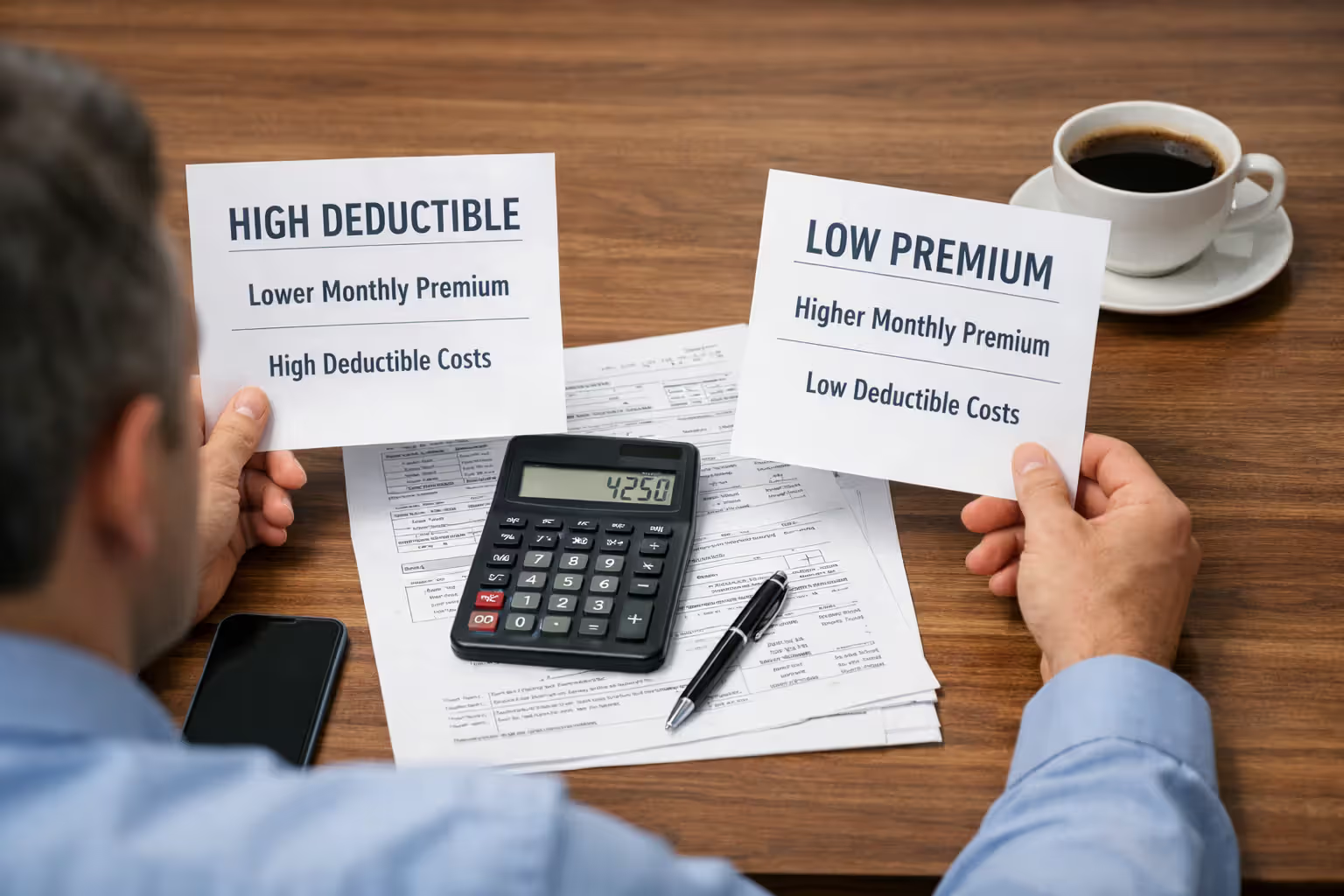

Understanding Deductibles and Premium Trade-offs

Your deductible represents the amount you pay out-of-pocket before insurance kicks in. This creates an inverse relationship with premiums: higher deductibles mean lower monthly costs.

Standard deductible options range from $250 to $2,000 for collision and comprehensive coverage. Choosing a $1,000 deductible instead of $250 typically reduces your premium 15-30%, translating to $200-400 in annual savings for many drivers.

Why is my car insurance so high deductible explained comes down to risk transfer. By accepting more financial responsibility for small claims, you reduce the insurer's exposure. They reward this with lower premiums.

The optimal deductible depends on your financial cushion. If a $1,000 unexpected expense would create hardship, stick with a lower deductible despite higher premiums. If you maintain an emergency fund that could easily absorb $1,000-2,000, choosing higher deductibles makes mathematical sense.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Consider your claiming behavior. If you rarely file claims and only would for major damage, high deductibles work well. Drivers who claim frequently for minor damage pay more in premiums over time than they would have with higher deductibles and fewer claims.

Run the break-even calculation: divide the annual premium savings by the deductible increase. If raising your deductible from $500 to $1,000 saves $300 annually, you break even in 1.7 years of claim-free driving ($500 difference ÷ $300 savings).

Location-Based Factors You Can't Control

Where you live and park your car overnight dramatically affects your premium through factors completely outside your control. Insurers analyze ZIP-code-level data to assess risk concentrations.

State insurance regulations create baseline differences. Michigan's unique no-fault system produces the nation's highest average premiums, while states like Idaho and Maine feature much lower costs. Mandatory coverage requirements, lawsuit environments, and fraud rates all vary by state.

Urban versus rural distinctions matter significantly. City drivers face higher premiums due to increased accident frequency, theft rates, and vandalism. More cars on the road mean more collision opportunities. A driver in downtown Los Angeles pays substantially more than someone in rural Montana for identical coverage on the same vehicle.

ZIP code risk ratings drill down further. Even within the same city, premiums fluctuate block by block. Insurers map theft patterns, accident intersections, and claim frequency to specific areas. Moving just a few miles can change your rate 20-30%.

Uninsured motorist prevalence in your area affects costs. If you live where many drivers skip insurance, your uninsured motorist coverage costs more and overall premiums rise because insurers face higher uncompensated losses.

Weather and natural disaster exposure influences comprehensive coverage pricing. Florida's hurricane risk, Texas's hail storms, and California's wildfire zones all push premiums higher in affected regions.

Legal environment and litigation trends matter. States with plaintiff-friendly courts and high jury awards see elevated premiums as insurers price in lawsuit costs. Louisiana and Michigan top lists for expensive litigation environments.

Vehicle Characteristics That Impact Insurance Pricing

How why is my car insurance so high works involves understanding that your vehicle choice directly impacts what you pay. Insurers maintain detailed databases on every make and model, analyzing repair costs, safety performance, and theft rates.

Vehicle value affects collision and comprehensive premiums. A $60,000 car costs more to repair or replace than a $20,000 car, so coverage costs more. However, the relationship isn't perfectly linear—some luxury brands have surprisingly affordable parts and repair networks.

Safety ratings influence rates. Vehicles with top IIHS and NHTSA crash test scores often qualify for discounts because they better protect occupants, reducing injury claim severity. Advanced safety features like automatic emergency braking, lane departure warning, and blind-spot monitoring can lower premiums.

Repair costs vary dramatically by vehicle. Some cars use expensive proprietary parts or require specialized labor. Aluminum body panels cost more to fix than steel. Luxury brands with complex electronics generate higher repair bills even for minor accidents.

Theft likelihood creates significant premium differences. The Honda Civic and Honda Accord consistently rank among most-stolen vehicles, raising comprehensive coverage costs. Rare, expensive sports cars also face high theft risk. Conversely, vehicles with strong anti-theft systems and low theft appeal cost less to insure.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Vehicle age cuts both ways. Older cars have lower values, making collision and comprehensive coverage less necessary, but they may lack modern safety features that qualify for discounts. A 10-year-old car might have cheap comprehensive coverage but higher liability premiums due to absent safety technology.

Performance characteristics matter. Sports cars and high-horsepower vehicles attract higher premiums because statistics show they're involved in more accidents and speeding violations. A 400-horsepower muscle car costs more to insure than a 180-horsepower family sedan, even at similar price points.

Vehicle size and weight influence injury claim costs. Larger SUVs and trucks generally cause more damage and injuries in collisions with smaller vehicles, potentially raising liability premiums, though their occupants fare better in crashes.

Ways to Lower Your Car Insurance Costs

One of the most counterintuitive aspects of car insurance pricing is that loyal customers often pay significantly more than new customers for identical coverage.Insurers use sophisticated pricing algorithms that identify customers unlikely to shop around and gradually increase their rates over time. Meanwhile, they offer aggressive discounts to attract new business. This 'loyalty penalty' can result in long-term customers paying 20-40% more than they would as new customers. The best defense is shopping your policy every 12-18 months, even if you're satisfied with your current insurer. Competition remains the most powerful tool consumers have to control insurance costs

— Robert Hunter

Once you understand why premiums run high, you can take strategic action to reduce costs without sacrificing necessary protection.

Shop around regularly. Insurance pricing changes constantly. Loyalty doesn't pay—insurers often raise rates on long-term customers while offering aggressive pricing to new customers. Compare quotes from at least five insurers every 12-18 months. Many drivers save $500-800 by switching.

Bundle policies. Combining auto and homeowners or renters insurance with one company typically unlocks 15-25% discounts on both policies. The savings often exceed $400 annually.

Improve your credit score. In states where credit-based insurance scoring is allowed, improving your credit from fair to good can reduce premiums 20-30%. Pay bills on time, reduce credit utilization, and correct errors on your credit report.

Ask about all available discounts. Insurers offer dozens of discounts that many customers miss: good student discounts for young drivers with B averages or better, low-mileage discounts for driving under 7,500 miles annually, defensive driving course completion, professional association memberships, military service, and more. Simply asking can uncover $200-500 in annual savings.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Adjust coverage strategically. If you drive an older vehicle worth less than $3,000-4,000, consider dropping collision and comprehensive coverage. The premiums may exceed the potential payout. Increase deductibles on vehicles you can afford to repair out-of-pocket.

Take a defensive driving course. Many states and insurers offer 5-15% discounts for completing approved defensive driving courses. The time investment of 4-8 hours can yield multi-year savings.

Reduce mileage. If you started working from home, notify your insurer. Lower annual mileage reduces accident risk and often qualifies for discounts. Some insurers offer usage-based programs that monitor driving and reward safe habits with discounts up to 30%.

Maintain continuous coverage. Never let your policy lapse, even if you temporarily stop driving. A lapse creates a coverage gap that raises future rates. If you won't drive for months, ask about suspended coverage or storage rates.

Choose vehicles wisely. Before buying, research insurance costs for models you're considering. A seemingly minor difference in trim level or model year can create significant premium variations.

Increase your liability limits strategically. The cost difference between 50/100/50 and 100/300/100 liability coverage is often just $100-200 annually, but the protection difference is substantial. This is usually money well spent.

Review your policy annually. Life changes affect insurance needs. When your car ages, when teenagers move out, when you relocate, or when your driving patterns change, your coverage should adjust accordingly.

Average Annual Premium Increase by Factor

| Factor | Typical Premium Increase |

| At-fault accident | +40% to +60% |

| DUI/DWI conviction | +80% to +100% |

| Reckless driving citation | +50% to +75% |

| Speeding ticket (15+ mph over) | +20% to +30% |

| Poor credit score | +50% to +70% |

| Urban location vs. rural | +20% to +35% |

| Sports car vs. sedan | +25% to +50% |

| Young driver (under 25) | +100% to +200% |

| Multiple claims (2-3 in 3 years) | +40% to +70% |

| Coverage lapse (30+ days) | +30% to +50% |

Note: Actual increases vary by insurer, state, and individual circumstances. Percentages represent industry averages for 2026.

Frequently Asked Questions

High car insurance premiums stem from a complex web of factors—some you control, others you don't. Your driving record, vehicle choice, coverage selections, and credit score offer opportunities for reduction through strategic decisions. Meanwhile, your age, location, and state regulations create baseline costs you must accept.

The key to managing insurance expenses lies in understanding what drives your specific rate and taking action where possible. Shop competitively every year or two, maintain a clean driving record, optimize your coverage and deductibles, and ask about every available discount. Small adjustments compound into significant savings over time.

Insurance protects your financial future from catastrophic loss. Finding the balance between adequate protection and affordable premiums requires ongoing attention, but the effort pays dividends. Drivers who actively manage their insurance rather than passively accepting renewal notices typically save hundreds to thousands of dollars annually while maintaining the coverage they need.