Driver reviewing rising car insurance costs at home with laptop and policy documents

How to Lower Car Insurance Costs?

Content

If you've opened your car insurance bill lately, you've probably done a double-take. Premium increases of 20%, 30%, even 50% have become common over the past three years. A policy that cost $1,200 in 2021 might now run $1,800 or more—for identical coverage, same car, same driver.

But here's something most people don't realize: your premium isn't set in stone. Insurance companies calculate rates using dozens of factors, and you can influence many of them. Some changes take five minutes—a phone call to ask about a forgotten discount. Others require a bit more effort, like improving your credit or comparing offers from six different carriers. Either way, most drivers can trim 15-30% off their bills, sometimes more.

What follows is a detailed roadmap for cutting your insurance costs this year. We'll cover everything from smart ways to compare quotes to coverage adjustments that make financial sense, plus the discounts hiding in plain sight that could save you hundreds.

Why Car Insurance Premiums Are So High Right Now

Let's start with context, because understanding why rates jumped helps you see which savings strategies work best.

Today's cars cost a fortune to fix. That Honda Accord isn't just steel and glass anymore. It's got front-collision sensors, lane-departure cameras, parking radar, adaptive cruise control. Tap someone's bumper at 5 mph, and you might face a $3,500 repair bill—not for frame damage, but to replace and recalibrate all those sensors. Parts that used to arrive next-day now take weeks because of supply chain snarls. Body shop technicians are in short supply, and the ones still working command premium wages. Insurers foot these bills, then pass the cost to everyone.

Medical expenses keep climbing. When someone gets hurt in an accident, their treatment might involve emergency room visits, surgery, physical therapy, specialist consultations. Those bills have grown 4-6% annually for years. Bodily injury liability claims represent the biggest chunk of what insurers pay out, and medical inflation directly feeds into your premium.

More people are crashing again. After a brief dip during pandemic lockdowns, accident rates bounced back as traffic returned to normal levels. Distracted driving—phones, mostly—remains a massive problem. More crashes mean more claims, which means higher rates for everyone in your area.

Everything got more expensive for insurers too. Court judgments, legal fees, administrative costs, even the salaries they pay adjusters—all of it increased with broader inflation. When an insurer's costs rise 15%, they can't keep premiums flat without losing money.

These trends explain the sticker shock. They don't mean you're stuck paying whatever your current company demands. You've got leverage, especially if you haven't shopped your policy in a while.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Compare Quotes from Multiple Insurance Companies

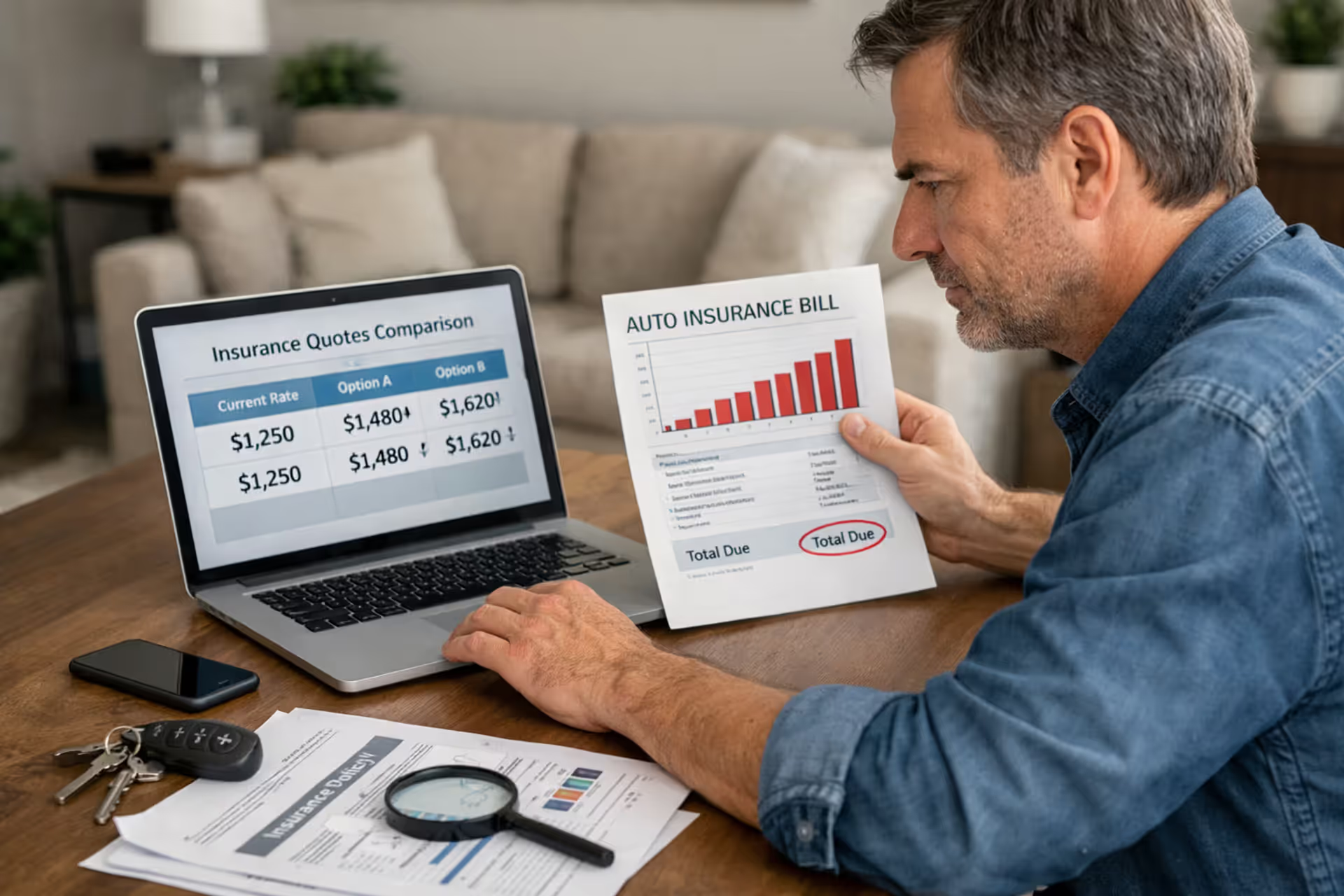

Let's get tactical. Shopping around isn't just helpful—it's often worth $500 to $1,500 per year for identical coverage. Same driver, same car, same address, but wildly different prices.

Why does this happen? Each company builds its own risk model. Progressive might care heavily about your credit score. State Farm might weight your job title differently. Geico specializes in certain demographics and offers them better rates. Your current insurer might have reclassified your neighborhood as higher-risk based on recent theft data, while a competitor uses older statistics that work in your favor. These models shift constantly as companies analyze new claims data and adjust their formulas.

Here's how to shop without wasting time:

Pull out your current policy. You need your exact coverage limits—like 100/300/100 liability, $500 collision deductible, $100 comprehensive deductible—so you're comparing identical protection, not accidentally quoting state minimums when you actually carry full coverage.

Get quotes from at least five companies. Mix it up: include a couple of direct-to-consumer brands (often cheaper premiums, but you handle everything online), an independent agent who represents multiple carriers (helpful if you want guidance), and maybe a well-known national brand. Don't assume the company with the cute commercials offers the best rate. Often they don't.

Timing matters more than you'd think. Start shopping 30-45 days before your renewal date. This gives you breathing room to compare carefully without your current policy lapsing. Most insurers reserve their most aggressive pricing for new customers—one recent analysis found that people who'd been with the same company for five-plus years paid 18% more on average than new customers buying identical coverage. Insurance companies bet on inertia. Don't reward that bet.

One caution: cheap isn't always best. Before you switch, check the company's financial stability rating (A.M. Best publishes these) and read customer reviews about their claims process. A policy that costs $200 less annually means nothing if they drag their feet for months when you file a claim or deny coverage on dubious grounds.

Adjust Your Coverage and Deductible Settings

After you've shopped competitors, look at your policy structure. How you configure your coverage and deductibles dramatically affects your premium—but these decisions involve trade-offs you need to understand.

Understanding Deductible Trade-offs

Your deductible is the amount you pay before insurance covers the rest. Higher deductible means lower premium, because you're shouldering more of the financial risk.

Here's what that looks like in practice:

| Deductible Amount | What You'd Pay Annually | Annual Savings Compared to $250 | What You Pay if You File a Claim |

| $250 | $1,800 | baseline | $250 |

| $500 | $1,550 | $250 | $500 |

| $1,000 | $1,350 | $450 | $1,000 |

| $2,000 | $1,200 | $600 | $2,000 |

These numbers are representative averages. Your actual figures depend on where you live, your vehicle, and your insurer's pricing model.

Do the math on your own situation. If bumping your deductible from $250 to $1,000 saves you $450 each year, you'll break even after roughly 20 months if you need to file a claim. Go three years without an accident, and you've pocketed $1,350 in savings—enough to cover that higher deductible plus an extra $350.

Practical advice: Pick the highest deductible you could pay from savings tomorrow without financial stress. If coming up with $1,000 in an emergency would require putting it on a credit card, stick with $500. If you've got a solid emergency fund, $1,000 or $2,000 makes mathematical sense.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

When to Drop Collision or Comprehensive Coverage

Collision pays to fix your car after an accident, regardless of who caused it. Comprehensive handles everything else—theft, hail damage, hitting a deer, vandalism. Both are optional once you've paid off your car loan (lenders require them while you're financing).

The question becomes: does the coverage cost more than it's worth?

Say your 12-year-old sedan has a market value of $3,500. You're paying $750 per year for collision and comprehensive, with a $1,000 deductible. Maximum payout if the car gets totaled: $2,500 after the deductible. You're spending 21% of the car's value annually for coverage that pays out less than the vehicle's worth. In four years of premiums, you'll have paid $3,000—nearly what the car's worth—without filing a single claim.

Consider dropping these coverages when: - Your vehicle's Kelley Blue Book value drops below $3,000-$4,000 - Annual premium plus deductible exceeds half the car's value - You've got savings earmarked for buying a replacement if your current car gets totaled

Keep comprehensive even on older cars if you live somewhere with high vehicle theft or severe weather risks (hail, floods). It's usually much cheaper than collision and protects against scenarios completely outside your control.

Unlock Discounts You May Be Missing

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Insurance companies offer more discounts than they actively promote. You have to ask. Many drivers leave hundreds of dollars on the table every year by not requesting discounts they qualify for.

Bundling your policies: Combine your auto insurance with homeowners or renters coverage at the same company. This typically cuts 15-25% off your auto premium. It's the single biggest discount most insurers offer, yet plenty of people keep their policies scattered across different companies.

Low mileage: Drive under 7,500 miles per year? Many insurers knock 5-15% off your rate. Remote work made this newly relevant for millions of people post-2020. Some companies now verify mileage through odometer photos or apps instead of taking your word for it, so be honest—but do claim it if you qualify.

Telematics programs: These involve an app or plug-in device monitoring your driving—how hard you brake, whether you speed, what time of day you drive. Safe drivers can earn discounts up to 30%. The catch is privacy; your insurer tracks everywhere you go. But if you brake gently and avoid rushing around at 2 AM, the savings add up fast.

Paying upfront: Pay your full six-month or annual premium in one shot instead of monthly installments. Typical savings: 5-10%, because you're avoiding financing charges the insurer would otherwise collect.

Affinity programs: Your employer, college alumni association, professional organization, or union might have negotiated group rates. Check your benefits portal or ask HR whether your company has an insurance partnership.

Good student discount: Full-time students under 25 with at least a B average usually save 10-25%. You'll need to submit a transcript or report card, but that's 20 minutes of effort for hundreds in savings.

Defensive driving courses: Complete an approved course (often available online) and many insurers shave 5-10% off your rate, especially if you're over 55. Some states legally require insurers to offer this discount.

Vehicle safety equipment: Anti-theft systems, anti-lock brakes, multiple airbags, automatic emergency braking—each can trim a few percentage points. Newer vehicles often qualify for several of these simultaneously.

Military affiliation: Active duty, veterans, and often their families qualify for substantial discounts at USAA and several other carriers that compete for military business.

Loyalty programs (proceed cautiously): Some insurers reward customers who stick around for years. But here's the catch: that 5% loyalty discount rarely offsets the 15-20% premium increase you'd avoid by switching to a competitor's new-customer rate. Always compare.

Stack four or five of these, and you might cut your premium by a third or more. The key is explicitly asking about each one and providing whatever documentation they require—don't assume they'll automatically apply discounts you qualify for.

The biggest mistake drivers make is treating car insurance like a fixed bill, when in reality it’s one of the most negotiable expenses in a household budget

— Daniel Harper

Improve Your Driving Record and Credit Score

Two factors you control directly have enormous impact on what you pay: your driving history and (in most states) your credit.

Your driving record: Tickets and at-fault accidents spike your rates significantly. A single speeding ticket can boost premiums 20-30% for the next three to five years. An at-fault accident? Often 40-50% or more, depending on severity. How insurers calculate your rate depends heavily on maintaining a clean record.

What you can do about it: - Fight tickets if you've got a legitimate defense. Even getting a major violation reduced to a minor one saves substantial money. - Ask about accident forgiveness. Some insurers waive the rate increase from your first at-fault accident if you've been claim-free for several years. - Take defensive driving after a ticket. Some states let you keep violations off your record or reduce points by completing an approved course. - Wait it out. Violations typically affect your rates for three to five years, with the impact declining as they age. That ticket from 2020 hurts less in 2025.

Your credit: Most states allow insurers to use credit-based insurance scores when setting rates. The logic: statistical analysis shows people with lower credit file more claims on average. Whether that's fair is debatable. Whether it's legal in your state—except California, Hawaii, Massachusetts, and Michigan, which restrict or ban the practice—is not.

Boosting your credit score can cut your premium by 20% or more. Here's what matters most:

- Pay everything on time, every time. Payment history represents the largest component of your score.

- Keep credit card balances well below your limits. Using more than 30% of your available credit hurts your score.

- Don't close old accounts. Length of credit history factors into your score, and closing accounts shortens your average account age.

- Avoid opening multiple new accounts quickly. Each application triggers a hard inquiry, temporarily dinging your score.

Check your credit reports annually at annualcreditreport.com (the only truly free source) and dispute any errors. Moving from "fair" to "good" credit can save you more on insurance than you'd pay in interest on a small personal loan. Treat credit improvement as an insurance-reduction strategy, because in most states, that's exactly what it is.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Review Your Policy Annually and After Life Changes

Set a recurring reminder to review your car insurance once a year, even if your premium stayed flat. Your circumstances change. Your vehicle ages. Your neighborhood's risk profile shifts. What made sense 18 months ago might not make sense now.

Specific events that should trigger an immediate policy review:

Getting married or divorced: Married drivers typically pay 5-15% less than single drivers, all else equal—insurers view marriage as a stability indicator that correlates with fewer claims. Got married? Call your insurer the same week. Getting divorced? Your rate might increase, and you definitely need to remove your ex-spouse from the policy to avoid covering their accidents.

Moving to a new address: Premiums vary wildly by ZIP code based on local accident rates, vehicle theft statistics, and lawsuit trends. Moving from downtown Chicago to a suburb 30 minutes away might cut your rate 25%. Relocating from a low-crime neighborhood to a higher-crime area will increase it. Either way, you must notify your insurer—it's typically a policy requirement, and if you don't update your address and then file a claim, coverage might be denied.

Buying or selling a vehicle: Newer, more expensive cars cost more to insure. Older, cheaper vehicles cost less. If you sold your 2023 SUV and bought a 2015 sedan, your rate should drop significantly. If you paid off your car loan, you now have the option to drop collision and comprehensive if the vehicle's value justifies it.

Driving less: Started working remotely? Retired? Moved closer to your office? Your annual mileage affects your rate. If you dropped from 15,000 miles per year to 7,000, tell your insurer and request a mileage-based adjustment. Some companies offer per-mile policies that could save you 30-40% if you rarely drive.

Kids moving out: If your 22-year-old graduated and moved across the country with their car, remove them from your policy. Your premium will drop substantially. If they're away at college more than 100 miles from home without a car, ask about a "student away at school" discount—you'll save money while maintaining coverage for when they visit.

Changing careers: Certain professions—teachers, engineers, nurses, scientists—qualify for occupation-based discounts at many insurers. If you switched jobs, ask whether your new role affects your rate.

Failing to update your insurer about major life changes means you're either overpaying or risking coverage gaps. Make it a habit: significant life event happens, update your insurance within 30 days.

Common Mistakes That Keep Your Premiums High

Even careful drivers make errors that cost them hundreds each year. Here's what to avoid:

Setting up autopay and forgetting the policy exists: Insurers count on you not noticing when your rate creeps up 8% at renewal, then another 6% the next year. If you're not opening those renewal notices, you won't catch it until you've overpaid for years. Review every renewal document, even if your payment happens automatically.

Never asking about new discounts: Finished a degree? Installed a home security system? Hit a low-mileage threshold? Insurers won't always call to tell you these qualify for discounts. When something in your life changes, call and specifically ask whether it affects your rate.

Paying for rental car coverage you don't need: Many premium credit cards include rental car insurance as a cardholder benefit. If yours does, you're wasting $30-$60 annually on redundant coverage through your auto policy. Check your card's benefits guide and drop the duplicate coverage.

Letting your policy lapse, even briefly: Miss a payment by a few days and your coverage gets canceled? That gap—even 24 hours—can label you "high-risk" in insurers' eyes and spike your rates for the next three to five years. When switching companies, make absolutely certain your new policy starts the same day your old one ends, not a day later.

Filing small claims that cost you more in the long run: Every claim you file typically increases your rate for three to five years, even if you weren't at fault (in many states). If you have $800 in damage and a $500 deductible, you'll collect $300 from insurance—then pay an extra $400-$500 annually in increased premiums for years. Do the math before filing. Sometimes paying out-of-pocket costs less than filing and accepting the rate increase. Understanding when to use your insurance versus paying yourself is part of managing long-term costs strategically.

Ignoring credit problems: In states where credit affects insurance pricing, letting your score deteriorate can cost you far more in premium increases than you'd lose in loan interest. A 40-point credit score drop might boost your insurance bill $300 per year. Monitor your credit and maintain it as an insurance expense-control measure.

Staying with your agent out of loyalty or convenience: Personal relationships matter, but not $800 per year. If your agent's companies no longer offer competitive rates for your risk profile, and they're not aggressively shopping your policy, you're paying hundreds for that convenience. Friendship is valuable. Overpaying for years isn't.

Frequently Asked Questions

Cutting your car insurance costs in 2025 doesn't require insider connections or secret loopholes. It requires treating insurance as an active financial decision rather than a set-it-and-forget-it expense. Shop your coverage annually, because rates change and loyalty rarely pays off. Adjust your deductibles and coverage to match your actual financial situation and risk tolerance. Claim every discount you qualify for—insurers won't always volunteer them. Maintain a clean driving record and healthy credit score, since both directly determine what you'll pay. Review your policy after major life changes, and avoid the common mistakes that quietly cost hundreds each year.

Drivers who pay the least aren't necessarily the safest or lowest-risk. They're the ones who dedicate a few hours annually to managing their insurance strategically. Follow the steps outlined here, and you'll likely save enough to fund a vacation, boost retirement contributions, or simply reduce the financial stress of rising expenses everywhere else. These strategies work—but only when you actually implement them, not just read about them.