Person reviewing health insurance bills and plan options at home

How Much Is Health Insurance in the US?

Content

When Americans talk about their biggest monthly bills, health insurance always makes the top three. But here's what makes it tricky: that premium you pay every month? That's just your entry ticket. The real cost includes deductibles you'll hit before coverage kicks in, copays at every doctor visit, and coinsurance that keeps taking a percentage until you've maxed out. Where you live, how old you are, and which plan you pick—all of it creates a price tag that shifts wildly from person to person.

Average Health Insurance Costs in 2026

Let's talk premiums first, since that's what hits your bank account every month. If you get insurance through work, you're probably paying somewhere around $145 monthly for solo coverage. Your employer? They're kicking in roughly $565—something most people don't realize. Family coverage gets pricier fast: expect to pay about $520 from your paycheck while your company covers $1,480.

Now, if you're shopping on the Affordable Care Act marketplace without help from subsidies, brace yourself. Individual plans run anywhere from $450 to $650 each month. Which number you land on depends heavily on your state and whether you're going Bronze, Silver, Gold, or Platinum. Family plans? You're looking at $1,200 to $2,100 monthly before any tax credits reduce that amount.

Buying directly from insurance companies instead of through the marketplace usually tacks on another 10-15%. Why? You're losing access to those tax credits. Picture a 40-year-old who doesn't smoke: they might pay $525 for a marketplace Silver plan but $605 for basically the same coverage purchased straight from the insurer's website.

Here's something that catches people off guard: geography matters more than almost anything. Take that same 40-year-old. In Wyoming, a benchmark Silver plan costs around $720 monthly. Over in Massachusetts? About $420. States with multiple insurers competing tend to offer lower premiums, though you'll want to double-check network quality and deductibles—cheaper premiums sometimes mean fewer doctors to choose from.

Author: Caroline Halstead;

Source: talero.spotpariz.net

What Affects Your Health Insurance Costs

Six factors dominate what you'll pay, and they're worth understanding if you want to find savings or at least avoid sticker shock.

Age hits harder than most people expect. Insurance companies can charge someone who's 64 up to three times what they bill a 21-year-old for identical coverage. So that Silver plan running $280 monthly for someone in their early twenties? It jumps to $840 for someone approaching Medicare age in the exact same zip code. This multiplier applies to marketplace and private plans, but interestingly, it doesn't affect what you pay through an employer.

Location creates price swings because healthcare itself costs different amounts depending on where you live. Cities with several competing hospital systems usually mean lower premiums than rural counties with one medical center. State regulations pile on too—some states mandate coverage for specific services, which pushes baseline costs up across the board.

Tobacco use will cost you big. Most states let insurers add up to a 50% surcharge if you've used tobacco within the past six months. That $400 premium becomes $600 instantly. A handful of states ban this practice, and some employer plans substitute wellness programs instead of hitting you with direct surcharges.

Plan category determines your baseline premium, though it works inversely with what you'll pay when you actually need care. Bronze plans feature the smallest monthly bills but the biggest deductibles. Platinum flips that entirely.

Family size multiplies your costs, though not always in a straight line. Adding your spouse typically doubles premiums. But here's an interesting quirk: many insurers discount the third child and beyond. Some even cap family premiums at what three kids would cost, even if you've got five.

Income level technically doesn't change what the plan costs—but it determines whether subsidies slash your monthly payment. Households earning between 100% and 400% of federal poverty level qualify for premium tax credits through the marketplace. We're talking real money here: some lower earners selecting Bronze plans pay zero monthly after credits apply.

Plan Metal Tiers and Pricing

The Affordable Care Act established these four metal tiers based on something called actuarial value—basically, what percentage of your total healthcare costs the plan covers versus what comes out of your pocket.

Bronze plans handle 60% of costs and carry the smallest premiums but the steepest deductibles—think $6,000 to $8,500 before coverage really starts. A 30-year-old typically pays $320 to $420 monthly. These work great if you're healthy and mainly need preventive care covered, or if you can handle significant out-of-pocket costs but want catastrophic protection.

Silver plans split costs 70/30 and dominate marketplace enrollment, partly because they're the only tier where cost-sharing reductions apply for qualifying households. Those reductions actually lower your deductibles and copays—basically giving you Gold-level coverage at Silver prices if you qualify. A 30-year-old averages $400 to $550 monthly, with deductibles between $3,500 and $5,500. This tier balances affordable premiums against reasonable financial exposure.

Gold plans cover 80% of your costs, which means premiums run 25-35% higher than comparable Silver options—roughly $520 to $700 monthly for a 30-year-old. But deductibles drop to $1,500 to $3,000. If you're seeing specialists regularly or managing expensive prescriptions, the higher premium often pays for itself after your fourth or fifth appointment.

Platinum plans handle 90% of costs and charge the highest premiums, typically $650 to $850 monthly for a 30-year-old. In exchange, deductibles drop to $0 to $1,000, and copays usually run just $10 to $20. These rarely make sense unless you've got chronic conditions requiring constant care or you know you're facing major medical expenses like surgery or childbirth.

Interestingly, the price gap shrinks as you age. A 60-year-old might find only $80 separating Bronze from Gold premiums, making higher tiers relatively more attractive than they appear to younger buyers.

Author: Caroline Halstead;

Source: talero.spotpariz.net

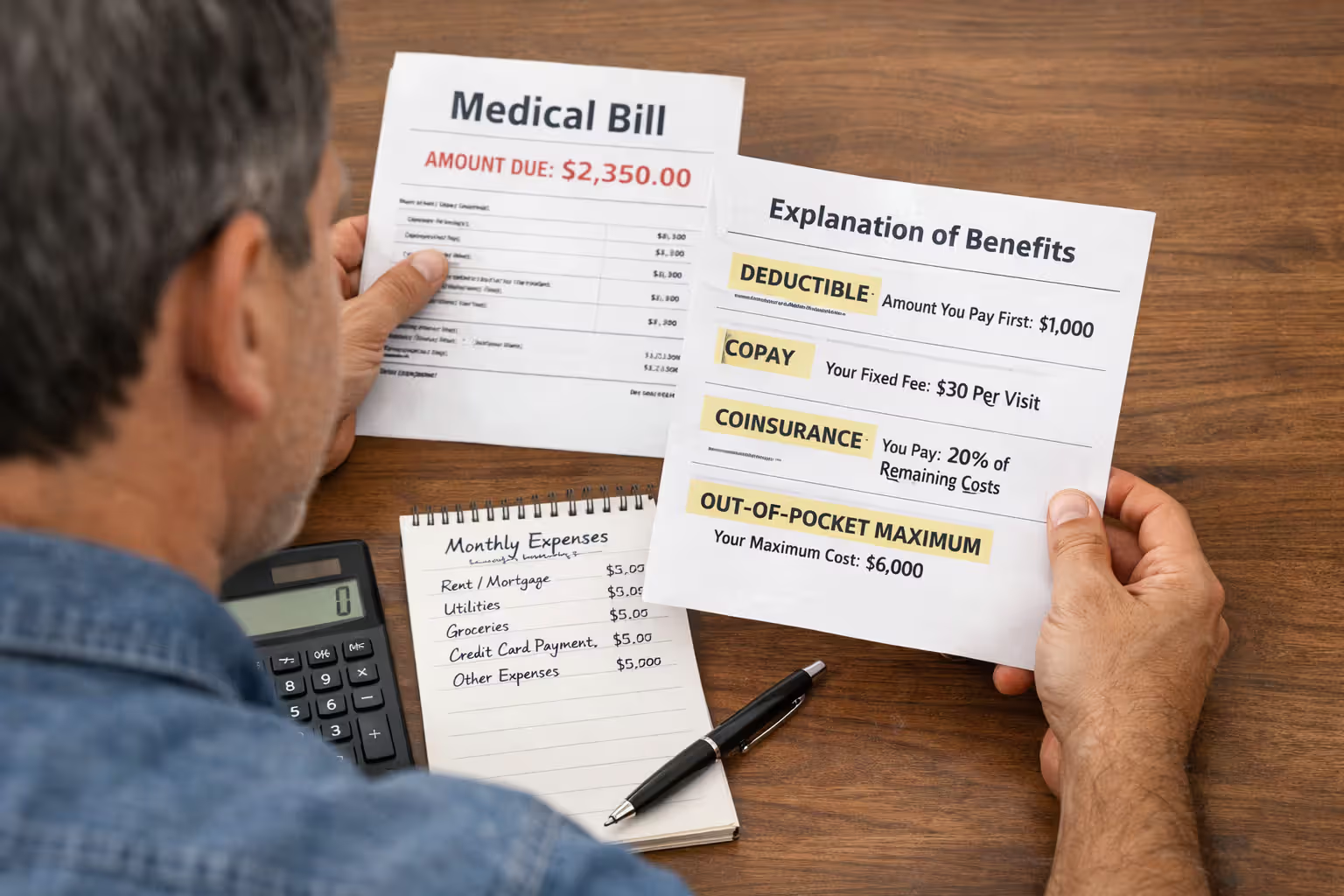

Understanding Deductibles and Out-of-Pocket Costs

Your deductible is what you'll pay for covered services before insurance starts chipping in. Hit a $4,000 deductible and you're covering that entire first $4,000 yourself—except for preventive care, which plans must cover completely regardless of deductible status.

Deductible amounts move opposite of premiums. Bronze plans average $6,500 deductibles, Silver lands around $4,500, Gold drops to $2,000, and Platinum hits roughly $500. Family deductibles typically double individual amounts, though some plans use embedded deductibles where coverage starts once any single family member reaches the individual threshold, even if the family total hasn't been met.

Copays are set dollar amounts for specific services—maybe $30 for your regular doctor, $50 for a specialist, $100 for the ER. These typically don't chip away at your deductible, though they do count toward your annual out-of-pocket maximum. Some plans waive deductibles entirely for certain services, applying only copays.

Coinsurance is your percentage share after you've cleared the deductible. With 20% coinsurance, a $1,000 procedure means you pay $200 and insurance covers $800. This cost-sharing arrangement stays in effect until you hit your out-of-pocket maximum.

The out-of-pocket maximum caps your annual spending on covered services. For 2026, ACA-compliant plans can't exceed $9,450 for individuals or $18,900 for families. Once you reach this ceiling, insurance pays 100% of covered services for the rest of the year. Important note: your premiums don't count toward this limit, and neither do out-of-network costs in most plans.

Here's a real-world scenario: You've chosen a Silver plan with a $4,500 deductible, 20% coinsurance, and an $8,700 out-of-pocket maximum. You break your leg and need surgery totaling $35,000. You'll pay that first $4,500 to meet your deductible. Then you'd owe 20% of the remaining $30,500 (which equals $6,100), but your out-of-pocket maximum stops you at $8,700 total. So you pay another $4,200 after the deductible, hitting your $8,700 cap. Insurance picks up the remaining $26,300.

Understanding this math helps you decide whether paying higher premiums for lower out-of-pocket exposure makes sense, or whether you'd rather accept more financial risk in exchange for monthly savings.

Author: Caroline Halstead;

Source: talero.spotpariz.net

What Health Insurance Plans Cover

Every ACA-compliant plan must include ten essential health benefits: ambulatory patient services, emergency services, hospitalization, pregnancy and childbirth care, mental health and substance use services, prescription medications, rehabilitative services, laboratory services, preventive and wellness services, plus pediatric services that include dental and vision for kids.

Preventive care gets covered at 100%—no deductible, no copay, no coinsurance. We're talking annual physicals, vaccinations, cancer screenings, blood pressure checks, diabetes screening, and contraceptive services. Catch is you've got to use in-network providers.

Prescription drug coverage operates on formulary tiers. Generic drugs typically run $10 to $25 copays, preferred brand-names hit $50 to $80, non-preferred brands reach $100 to $150, and specialty medications often involve 25-35% coinsurance that can climb into hundreds per refill. Some plans make you meet the deductible for all prescriptions; others waive it for generics and preferred brands.

Mental health services must receive equal treatment with physical health coverage—insurers can't impose tighter restrictions on therapy sessions or psychiatric care than they do on other medical services. Most plans cover outpatient therapy at specialist copay rates ($40 to $75), though actually finding in-network therapists proves challenging in many regions.

Hospitalization includes your room, surgery, anesthesia, and medical supplies. You'll typically face your deductible plus coinsurance. A three-day hospital stay running $45,000 might cost you $4,500 out-of-pocket with a Silver plan carrying a $4,500 deductible and 20% coinsurance—though you'd never exceed your out-of-pocket maximum.

Services typically excluded include cosmetic procedures, most alternative medicine (though acupuncture coverage varies by state and plan), routine dental and vision care for adults, hearing aids in many states, weight loss programs, and fertility treatments beyond basic diagnostics. Some insurers offer these as optional add-ons for extra premiums.

Out-of-network care gets sharply reduced coverage or none at all. PPO plans typically cover 40-60% of out-of-network costs after a separate, higher deductible applies. HMO and EPO plans? They won't cover out-of-network care at all except in emergencies. Verifying whether your doctors and preferred hospitals participate in a plan's network matters just as much as understanding coverage details.

How to Lower Your Health Insurance Costs

Premium tax credits deliver the biggest savings opportunity for marketplace shoppers. Households earning up to 400% of federal poverty level ($60,240 for individuals, $124,800 for a family of four in 2026) qualify for subsidies reducing monthly premiums. A family earning $85,000 might watch their $1,400 monthly premium drop to $650 after credits apply. You can either receive credits immediately on monthly bills or claim them when filing taxes.

Cost-sharing reductions cut your deductibles, copays, and out-of-pocket maximums if you're earning up to 250% of poverty level and you select a Silver plan. That standard Silver plan with its $4,500 deductible transforms into a $1,500 deductible plan if you qualify for CSRs—essentially Gold-level coverage at Silver prices.

Employer contributions typically handle 70-80% of premium costs for employee-only coverage. If your employer offers health insurance, compare their subsidized premium against marketplace options even if you'd qualify for tax credits. Employer coverage usually wins, though not always for family coverage where employer contributions often shrink as a percentage—worth comparing both during open enrollment if you've got the choice.

Health Savings Accounts pair exclusively with high-deductible health plans to create triple tax advantages. Contributions reduce your taxable income, money grows tax-free, and withdrawals for qualified medical expenses carry no tax penalty. For 2026, contribution limits hit $4,300 individually or $8,550 for families. Think of HSAs as healthcare retirement accounts—unused funds roll over forever and can even supplement retirement income after age 65.

Plan selection strategy carries more weight than most people realize. Healthy and rarely need care beyond preventive checkups? A Bronze plan saves $1,500 to $2,400 yearly in premiums compared to Gold, and you'll probably sidestep that higher deductible entirely. But if you're taking three maintenance medications and seeing specialists quarterly, Gold or Platinum plans often cost less overall despite steeper premiums because lower copays and deductibles reduce your per-visit spending.

Timing enrollment strategically can yield substantial savings. Approaching 26 and aging off a parent's plan? Compare whether jumping into an employer plan immediately or waiting for the next marketplace open enrollment period (using COBRA as a bridge) produces better rates. Similarly, if you're 64 and eyeing retirement, staying employed until 65 when Medicare starts might save thousands compared to purchasing individual coverage for that final year.

Tobacco cessation eliminates that brutal 50% surcharge many insurers apply. Quit smoking six months before your next enrollment period and you could save $2,400 to $3,600 annually on premiums alone.

Author: Caroline Halstead;

Source: talero.spotpariz.net

Filing and Managing Health Insurance Claims

Most health insurance claims process automatically without requiring any action from you. Visit a doctor or hospital within your plan's network, and the provider submits the claim electronically—usually within 48 hours. The insurer processes it, applies your deductible and coinsurance calculations, then pays the provider directly.

You'll receive an Explanation of Benefits (EOB) roughly 10-20 days after claim processing. Here's what confuses people: EOBs aren't bills. They show what the provider charged, what the insurer's negotiated rate allowed, what you owe, and what insurance paid. Always compare your EOB against any bills from the provider—it's your best defense against billing errors.

Claim processing timelines average 30 days for straightforward claims, though complex cases requiring medical review can stretch to 60-90 days. Insurers must acknowledge receipt within 15 business days and deliver approval or denial decisions within 30 days for post-service claims. Urgent care claims require decisions within 72 hours by law.

Common claim issues include coding errors where providers use wrong procedure codes triggering denials, balance billing when out-of-network providers charge above the insurer's allowed amount, and coordination of benefits problems when multiple insurance policies exist. Roughly 15-20% of claims contain errors—reviewing EOBs carefully actually matters.

Claim denied? You've got appeal rights. You must submit internal appeals within 180 days of receiving denial. Insurers must respond within 30 days for standard appeals, 72 hours for urgent situations. If the internal appeal fails, you can pursue an external review by an independent third party at zero cost to you. External reviewers overturn insurer denials approximately 40% of the time—worth pursuing.

Reimbursement claims come into play when you've paid out-of-pocket for covered services—maybe you visited an out-of-network provider or paid upfront for a service. Submit the itemized receipt, proof of payment, and a completed claim form (download from your insurer's website) within one year of service. Reimbursement checks typically arrive 30-45 days after submission.

Keeping organized records helps immensely when disputes arise. Save all EOBs, bills, receipts, and correspondence with insurers and providers. Many insurers now offer mobile apps that track claims in real-time and store digital EOB copies, making record-keeping significantly easier.

Comparing Average Health Insurance Costs by Plan Type

| Plan Tier | Individual Monthly Premium | Family Monthly Premium | Typical Individual Deductible | Typical Out-of-Pocket Maximum | Works Best For |

| Bronze | $380–$480 | $1,100–$1,400 | $6,500 | $9,100 | Healthy people wanting catastrophic protection |

| Silver | $480–$620 | $1,400–$1,800 | $4,500 | $8,700 | Moderate healthcare needs, eligible for subsidies |

| Gold | $600–$780 | $1,750–$2,200 | $2,000 | $8,150 | Regular care needed, managing chronic conditions |

| Platinum | $750–$950 | $2,200–$2,800 | $500 | $6,850 | Frequent healthcare users, predictable budgets wanted |

These premiums reflect rates for a 35-year-old non-smoker. Your actual costs shift based on location, insurer, and specific plan design.

The sticker shock of health insurance premiums obscures a more important calculation: total cost of care.A Bronze plan saving you $200 monthly costs $2,400 less in premiums annually, but if you need just two specialist visits and one urgent care trip, the higher deductible and copays could eliminate those savings entirely. Most Americans would benefit from matching their plan tier to their actual utilization patterns rather than defaulting to the lowest premium option

— Dr. Michael Chernew

Frequently Asked Questions About Health Insurance Costs

Health insurance expenses stretch far beyond that monthly premium. The right plan balances premium costs against your anticipated healthcare needs while factoring in deductibles, copays, and coverage limits. That Bronze plan costing $380 monthly might look attractive compared to a $620 Silver plan, but two specialist visits and one prescription could wipe out that $240 monthly savings pretty fast.

Start by estimating your annual healthcare utilization—how many doctor visits you typically need, whether you take regular medications, your likelihood of requiring surgery or other major services. Match that projection against total cost (premiums plus expected out-of-pocket spending) for each plan tier available to you.

Don't sleep on subsidy eligibility. Nearly 90% of marketplace enrollees qualify for premium tax credits dramatically reducing monthly costs. A family earning $75,000 might pay $450 monthly for Silver coverage instead of $1,600—that's $13,800 in annual savings.

Review your plan annually during open enrollment. Changes in income, health status, or available plans might make a different tier more cost-effective. Last year's perfect plan might not be optimal this year.

Finally, use your coverage strategically. Take advantage of free preventive care, opt for generic medications when available, stay within your network, and address health issues early before they become expensive emergencies. The best health insurance strategy combines appropriate coverage selection with smart healthcare consumption.