Driver comparing full coverage car insurance quotes next to a parked car

How Much Is Full Coverage Car Insurance?

Content

Most Americans spend around $2,314 annually on full coverage car insurance, though your actual bill might land anywhere from $1,200 to over $4,500 depending on your location and personal factors. Getting a handle on insurance pricing—and what you're actually purchasing—puts you in control of your coverage decisions without wasting money.

What Does Full Coverage Car Insurance Actually Mean

There's no standardized insurance product called "full coverage"—you won't spot this term in your official policy paperwork or state regulations. It's simply shorthand that drivers have adopted to describe protection that extends beyond their state's basic requirements.

This creates confusion because everyone defines "full" differently. Some people assume it means complete protection against any possible loss—a misconception that leads to claim disappointments. Others think it represents an identical package at every insurance company, when it's really a customized bundle you select.

When most drivers reference full coverage, they're talking about three components working together: liability protection (covers harm you cause others), collision protection (repairs your vehicle after crashes), and comprehensive protection (addresses non-collision incidents such as weather damage or theft). Lenders financing your vehicle will insist you maintain these three coverage types.

What gets left out? Your medical expenses after an accident—that requires separate medical payments or personal injury protection riders. Need a temporary vehicle during repairs? That demands specific rental reimbursement add-ons. Aftermarket wheels or a premium sound system? Such customizations need special policy endorsements. This gap between the word "full" and actual policy provisions catches many drivers off guard at claim time.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

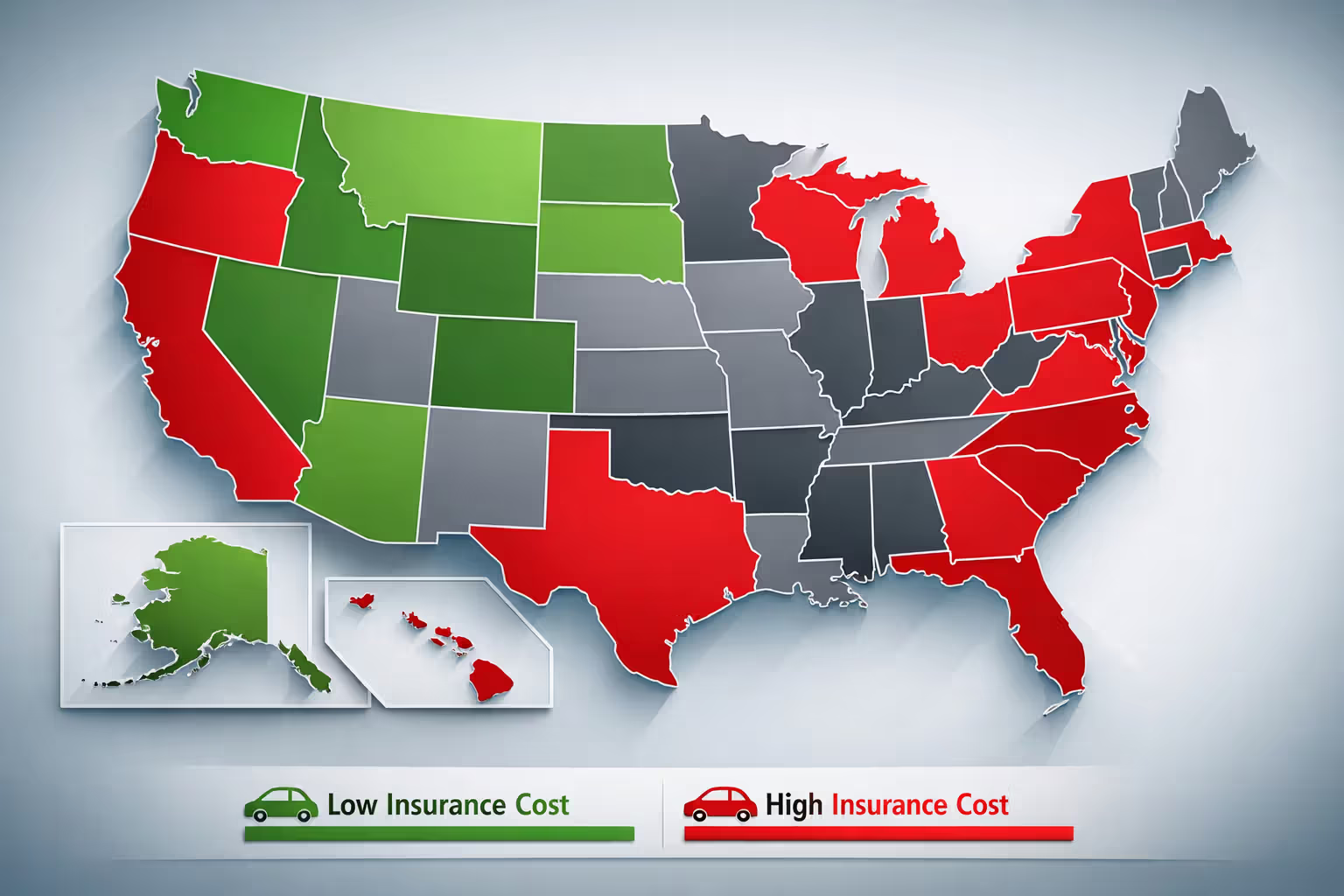

Average Cost of Full Coverage Car Insurance by State

Your home address influences premiums as powerfully as your vehicle choice. Someone in Idaho with an excellent record might spend $1,100 yearly for identical coverage that costs $3,800 in Michigan. These dramatic variations stem from state regulations, regional accident frequencies, climate-related risks, legal environments, and local rates of uninsured motorists.

| State | Yearly Cost | Monthly Cost |

| Alabama | $2,156 | $180 |

| Alaska | $2,089 | $174 |

| Arizona | $2,267 | $189 |

| Arkansas | $2,398 | $200 |

| California | $2,551 | $213 |

| Colorado | $2,619 | $218 |

| Connecticut | $2,447 | $204 |

| Delaware | $2,512 | $209 |

| Florida | $3,183 | $265 |

| Georgia | $2,334 | $195 |

| Hawaii | $1,877 | $156 |

| Idaho | $1,512 | $126 |

| Illinois | $2,156 | $180 |

| Indiana | $1,923 | $160 |

| Iowa | $1,734 | $145 |

| Kansas | $2,089 | $174 |

| Kentucky | $2,445 | $204 |

| Louisiana | $3,456 | $288 |

| Maine | $1,645 | $137 |

| Maryland | $2,398 | $200 |

| Massachusetts | $2,334 | $195 |

| Michigan | $3,012 | $251 |

| Minnesota | $1,989 | $166 |

| Mississippi | $2,467 | $206 |

| Missouri | $2,234 | $186 |

| Montana | $2,156 | $180 |

| Nebraska | $2,001 | $167 |

| Nevada | $2,789 | $232 |

| New Hampshire | $1,823 | $152 |

| New Jersey | $2,678 | $223 |

| New Mexico | $2,445 | $204 |

| New York | $2,912 | $243 |

| North Carolina | $1,867 | $156 |

| North Dakota | $1,734 | $145 |

| Ohio | $1,956 | $163 |

| Oklahoma | $2,567 | $214 |

| Oregon | $2,178 | $182 |

| Pennsylvania | $2,289 | $191 |

| Rhode Island | $2,556 | $213 |

| South Carolina | $2,334 | $195 |

| South Dakota | $1,889 | $157 |

| Tennessee | $2,267 | $189 |

| Texas | $2,623 | $219 |

| Utah | $2,112 | $176 |

| Vermont | $1,756 | $146 |

| Virginia | $2,001 | $167 |

| Washington | $2,234 | $186 |

| West Virginia | $2,178 | $182 |

| Wisconsin | $1,812 | $151 |

| Wyoming | $1,923 | $160 |

| District of Columbia | $2,456 | $205 |

No-fault insurance states such as Florida and Michigan typically command higher premiums. In these locations, insurers pay their own policyholders' claims first, bypassing the traditional fault-determination process that delays but sometimes reduces overall costs. Regions with significant uninsured driver populations force everyone's rates upward to compensate for unpaid claims. Metropolitan areas naturally experience more accidents than rural communities, resulting in elevated urban pricing.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

What Factors Determine Your Full Coverage Premium

Insurance companies analyze numerous variables when setting your rate. While some factors remain outside your influence, others respond to deliberate changes. Understanding which elements carry substantial weight helps you concentrate efforts where they'll produce real savings.

Driver-Related Factors

Age significantly shapes your premium structure. Drivers under 25—particularly males—face steep costs because statistical data shows elevated crash rates in this demographic. A 19-year-old man could pay $4,800 yearly for protection a 45-year-old secures for just $1,800. Premiums generally decline throughout your twenties and thirties, stabilize during middle age, then increase modestly beyond age 70.

Your driving history exerts the strongest influence on costs. A single at-fault accident can spike rates 20-50% for three to five years afterward. DUI convictions may double or triple your premium—some carriers will refuse coverage entirely. Minor speeding violations boost costs 10-25%. Maintaining a clean record for three consecutive years unlocks preferential pricing.

Credit scores affect insurance pricing in most states. Insurers discovered that financially responsible individuals statistically file fewer claims. Excellent credit can reduce premiums 30-50% compared to poor credit scores, even with otherwise identical profiles. California, Hawaii, and Massachusetts prohibit this practice.

Occupation and education level sometimes influence rates. Teachers, engineers, and scientists frequently receive favorable pricing because claims data reveals lower accident involvement for these professions. Holding a college degree may reduce premiums 5-10% at select insurers.

Vehicle-Related Factors

Your car choice dramatically impacts full coverage costs since collision and comprehensive pricing reflects repair expenses and theft attractiveness. A Honda Civic costs substantially less to insure than a BMW 3-Series—parts run cheaper and thieves show less interest. High-performance cars and luxury brands command premium rates. Large SUVs increase costs because they inflict greater damage during collisions.

Vehicle age affects pricing in nuanced ways. A five-year-old model costs less than brand new because depreciated value means lower collision and comprehensive premiums. However, very old vehicles lacking contemporary safety technology miss out on discounts newer models receive.

Safety equipment and anti-theft systems reduce premiums. Forward collision warning, lane departure alerts, and adaptive cruise control can decrease costs 5-15%. Anti-lock brakes and multiple airbags are now standard but already factored into baseline calculations. Alarm systems and tracking devices lower comprehensive charges.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Coverage Limits and Deductibles

Your chosen liability limits directly affect premium amounts. State minimums cost less initially but provide inadequate protection. Increasing from 50/100/50 limits (meaning $50,000 per injured person, $100,000 total accident maximum, $50,000 property damage) to 100/300/100 might add $150-300 yearly—reasonable protection against catastrophic lawsuit exposure.

Deductible selection creates the most transparent cost relationship. Selecting $1,000 deductibles rather than $250 could save $300-500 annually. Drivers who rarely submit claims benefit financially from assuming greater deductible risk. You must maintain adequate cash reserves to handle that deductible if an incident occurs tomorrow.

Consumers often focus exclusively on monthly premium costs without thoroughly examining their coverage limits and deductible obligations. This approach leads to significant unexpected expenses during the claims process that slightly elevated premiums and properly structured coverage would have prevented

— J.D. Power's U.S. Auto Insurance Study

What Full Coverage Car Insurance Covers

Grasping precisely what your policy includes (and excludes) prevents unpleasant discoveries during claim situations. Each full coverage component addresses distinct protection needs.

All states except New Hampshire mandate liability insurance as the foundational legal requirement. This coverage pays for injuries and property damage you inflict on others when responsible for an accident. If you fail to yield at an intersection and strike another vehicle, liability handles their medical treatment, rehabilitation expenses, wage replacement, vehicle repairs, and attorney fees if litigation follows. It provides zero compensation for your injuries or vehicle damage—collision and comprehensive serve those purposes.

Collision coverage repairs or replaces your vehicle following accidents regardless of fault determination. Whether you strike another car from behind, get hit from the side, crash into a barrier, or flip your vehicle, collision addresses repair costs after deductible payment. Totaled vehicles trigger payment based on actual cash value (pre-accident worth, not purchase price or remaining loan balance).

Comprehensive coverage addresses all non-collision vehicle damage: theft, vandalism, fire, flooding, hail, falling objects, and animal collisions. If someone breaks your window to steal belongings, comprehensive applies. Strike a deer while driving at night? Despite involving a collision-type event, insurers categorize this as comprehensive. Both collision and comprehensive require initial deductible payment.

Critical limitation: collision and comprehensive coverage caps at your vehicle's actual cash value—insurers won't exceed total vehicle worth. Liability limits establish maximum per-accident payments. For example, carrying 100/300/100 limits when causing a crash injuring three people with medical costs of $75,000, $125,000, and $50,000 means your insurer pays maximum amounts of $75,000, $100,000, and $50,000 respectively, leaving you personally liable for the $150,000 shortfall.

Standard full coverage excludes medical payments coverage (Med Pay) or personal injury protection (PIP) for treating your own injuries. It doesn't include uninsured/underinsured motorist protection—coverage for hits by drivers with inadequate insurance. Rental reimbursement and roadside assistance require separate additions. Gap insurance covering the difference between vehicle value and outstanding loans demands independent purchase.

How Deductibles Affect Your Full Coverage Cost

Deductibles represent your initial contribution before insurance payments begin. With $500 collision deductible and $3,000 in repairs, you contribute the first $500 while your insurer covers the remaining $2,500.

Standard deductible ranges span $250 to $2,000, with $500 or $1,000 being most prevalent. You can select different amounts for collision versus comprehensive—perhaps $500 for collision but $250 for comprehensive if accident concerns outweigh weather damage worries.

Elevated deductibles produce reduced premiums because you assume additional financial risk. Increasing your deductible from $250 to $500 might save $200 yearly. Advancing from $500 to $1,000 could save another $250-400 annually. Simple calculation: remain claim-free three years and your savings surpass the increased deductible exposure.

Financial reality requires honest assessment. Can you access $1,000 immediately if you damage your car tomorrow morning? If that $1,000 means high-interest credit card debt, lower deductibles make better sense. With robust emergency savings easily covering deductible amounts, choose higher levels and capture annual savings.

Common mistake: selecting varied deductibles across multiple vehicles. Owning two cars doesn't require maintaining two separate deductible amounts in emergency funds—simultaneous crashes are extremely unlikely, so one deductible reserve suffices.

How to File a Full Coverage Insurance Claim

Efficient claim filing accelerates settlements and reduces frustration. The process follows predictable steps, though timing varies by company and claim complexity.

Immediately following an accident, assess injuries and contact emergency services for any medical concerns, substantial damage, or fault disputes. Exchange information with other drivers: names, contact numbers, insurance carriers, and registration details. Photograph all damage, accident locations, road signs, and traffic control devices. Avoid admitting responsibility or apologizing—provide only factual information.

Notify your insurer quickly, ideally within 24 hours. Many companies offer mobile applications enabling immediate claim initiation with direct photo uploads from accident scenes. Provide accurate incident details focusing exclusively on facts without speculation. They'll issue a claim number and assign an adjuster.

Your adjuster contacts you to discuss circumstances and schedule vehicle inspection. Minor damage may only require photograph submission. Extensive damage needs in-person assessment, either at your location or approved repair facilities. Adjusters evaluate damage severity, determine repair feasibility, and calculate appropriate repair costs.

For repairable vehicles, your insurer compensates the repair shop (minus deductible). Some insurers mandate network shop usage; others permit free selection. Typical repairs require one to three weeks depending on parts procurement and facility workload.

Totaled vehicles (repairs exceeding vehicle worth) generate settlement offers reflecting comparable local market vehicles. You can negotiate perceived low offers by documenting higher comparable sale prices. Accepting settlement transfers ownership to the insurer.

Common claim errors include delayed reporting (risking denial), accepting initial settlement offers without research, inadequate damage documentation, or authorizing repairs pre-inspection. Retain all receipts, correspondence, and documents until complete settlement.

Purchased rental reimbursement coverage typically activates once repairs commence, continuing until completion or reaching coverage maximums (frequently $30-50 daily for up to 30 days).

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Ways to Lower Your Full Coverage Insurance Cost

You can substantially reduce premiums without sacrificing essential protection through strategic shopping and maximizing available discounts.

Compare rates annually, potentially twice yearly. Insurance pricing fluctuates constantly as different companies compete aggressively across varying markets. Today's best deal may not remain optimal two years forward. Obtain quotes from at least five insurers—major national carriers and regional specialists. Online comparison platforms provide quick estimates, though agent consultations can reveal additional discount opportunities.

Bundle multiple policies with single insurers. Combining auto with homeowners or renters insurance typically saves 15-25% on both policies. Multi-vehicle discounts of 10-20% apply when insuring several cars together.

Inquire about every available discount. Common options include good driver (violation-free and accident-free), good student (teenagers maintaining B averages or higher), defensive driving course completion, military service, professional organization memberships, full payment (versus installment plans), paperless billing, and automatic payment enrollment. Some insurers operate telematics programs using plug-in devices or smartphone applications monitoring driving behavior—safe drivers can save 10-30%.

Improve your credit rating. Since most states permit credit-based insurance scoring, advancing from fair to good credit can reduce premiums 20% or more. Maintain timely bill payments, decrease credit card balances, and review credit reports for inaccuracies.

Evaluate dropping collision and comprehensive on aging vehicles. When your car's worth falls below $3,000 while you're paying $800 yearly for collision and comprehensive with $500 deductibles, you're essentially insuring $2,500 of actual value. After several years, premium payments exceed potential claim recovery. Only pursue this if you can afford self-funded replacement.

Increase deductibles incrementally. Moving from $250 to $500 feels less dramatic than jumping directly to $1,000, while still capturing meaningful savings. As emergency funds grow, gradually raise deductibles higher.

Maintain uninterrupted coverage. Insurance history gaps signal elevated risk to underwriters and increase rates. When selling a car without immediate replacement, purchase a non-owner policy preserving your coverage continuity.

Reduce annual mileage. Many insurers discount premiums for drivers logging under 7,500 or 10,000 annual miles. Remote work arrangements have made low-mileage qualifications more attainable.

Review your policy annually. Life changes affect insurance costs. Did your teenager establish independent residence? Remove them as listed drivers. Completed your auto loan? Collision and comprehensive become elective rather than mandatory. Relocated to a lower-crime neighborhood? Your rates may decrease accordingly.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Frequently Asked Questions About Full Coverage Car Insurance

That $2,314 national average represents merely a baseline reference. Your actual cost reflects your state, driving history, vehicle selection, coverage choices, and numerous other variables that insurers evaluate through proprietary formulas. Clean-record Idaho residents might spend $1,100 while comparable Louisiana drivers pay $3,400 for similar protection levels.

Concentrate on controllable factors: maintain violation-free records, enhance credit scores, compare rates regularly, and select deductibles matching your financial capacity. Don't assume "full coverage" shields you from every possible loss—understand precisely what's included and what requires additional riders. Balance premium savings against increased out-of-pocket exposure when filing claims.

The lowest available price doesn't always deliver optimal value. Saving $300 annually by reducing liability limits from 100/300/100 to state minimums exposes you to financial catastrophe when causing serious accidents. Similarly, selecting $2,000 deductibles to save $400 yearly backfires when you lack that cash during repair needs.

Reassess coverage annually as circumstances evolve. The full coverage justifying new car financing becomes questionable once that vehicle reaches eight years old with loan satisfaction. The minimum liability limits appearing adequate at 25 leave you dangerously vulnerable at 45 after accumulating substantial assets requiring protection.

Full coverage costs fluctuate dramatically, but comprehending cost drivers—and what protection you're actually purchasing—enables informed decisions safeguarding both your vehicle and financial security.