Suburban house with a newly replaced roof viewed from the street

Does Getting a New Roof Lower Home Insurance?

Content

You've probably heard neighbors mention their insurance bills dropping after a roof replacement. Is this real, or just another home improvement myth? Here's the truth: yes, a new roof can slash your premiums—but you'll need to navigate some specific requirements first.

Most homeowners spend $8,000 to $25,000 on roof replacement. That's serious money. If you're thinking about this project partly because of potential insurance savings, you should know exactly what discounts you qualify for and how to actually get them. Insurance companies won't just hand you a discount because you mention your new shingles during a phone call.

The connection between your roof and insurance costs makes perfect sense when you think about it. Your roof stops water, wind, and hail from destroying everything inside your home. A failing roof means higher claim risk. A brand-new, storm-resistant roof? That's money staying in the insurance company's pocket instead of going toward your claim check.

How Insurance Companies Evaluate Your Roof

Three things matter when underwriters look at your roof: how old it is, what it's made from, and whether it's falling apart.

Let's start with age. Your roof hits certain birthdays that insurance companies really care about. A five-year-old roof? No problem. A fifteen-year-old roof? They're watching it. A twenty-five-year-old roof? You might get a letter saying "replace this or we're canceling your policy." These aren't arbitrary numbers—they're based on when different roofing materials typically start failing.

Standard asphalt shingles last about 20-25 years in ideal conditions. Once you hit year 15, insurers start getting nervous. State Farm, Allstate, and other major carriers often add surcharges starting at the 15-year mark. By year 20, some companies simply won't renew your policy until you've installed a new roof.

What your roof is made from matters just as much as its age. Basic three-tab asphalt shingles are the Honda Civic of roofing—they work fine, but nobody's giving you bonus points. Metal roofing is like driving a Volvo: insurers love the safety factor and give you credit for it. Clay tile? Depends on where you live. In California's fire country, tile roofs get you major discounts. In Texas hail territory, that same tile might cost you extra because hailstones crack tiles like eggs.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Condition assessments have gotten weird lately. Since 2023, most insurance companies don't send actual humans to look at your roof anymore. Instead, they buy satellite photos and drone footage. Some company analyst in an office three states away zooms in on your house and decides whether your shingles look acceptable. You might not even know this happened until you get a letter demanding repairs.

When they do send physical inspectors (usually only if the photos raise red flags), these folks crawl around examining everything. They're checking flashing around your chimney, looking for granule loss on shingles, measuring sag in your roofline, and photographing any spots that look questionable. Their report goes straight to underwriting and determines whether you keep your coverage.

Geography plays a huge role here too. A roof in coastal Florida faces completely different evaluation standards than one in rural Pennsylvania. Wind resistance matters most in hurricane zones. Impact ratings dominate in the hail corridor running from north Texas through Oklahoma and Kansas. California properties get scrutinized for fire-resistant materials if they're anywhere near wildland areas.

When a New Roof Reduces Insurance Costs

Not every new roof triggers premium reductions. Sometimes you're just swapping out worn shingles for fresh ones without changing your rate.

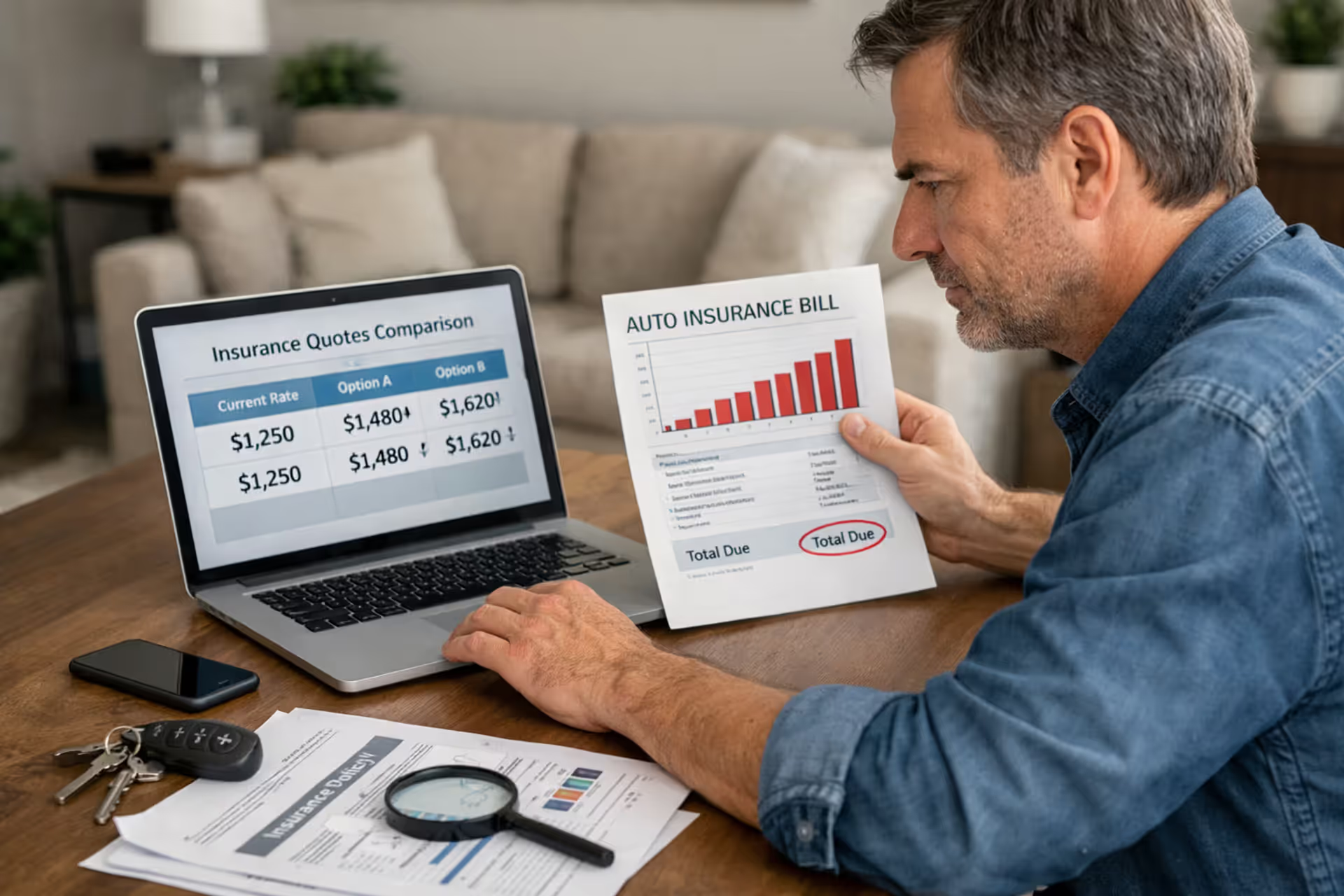

The biggest savings happen when your current roof has already triggered age-based surcharges. Let's say you're paying an extra 20% because your roof turned 22 years old. Installing a new roof wipes out that penalty immediately. You're not getting a "discount" exactly—you're removing a surcharge. But the effect on your wallet is the same.

Actual new roof discounts (not just surcharge removal) typically range from 5% to 15% in the first decade after installation. Companies like USAA, Nationwide, and State Farm offer these in most states, though the exact percentage depends on where you live. After ten years, these discounts usually start phasing out as your roof ages.

Timing this right can save you thousands over the life of your roof. Replace too early—say when your roof is only 12 years old and still in decent shape—and you miss out on years of discounts you could have gotten. Wait too long, and you're stuck paying surcharges while scrambling to find contractors during the busy season.

The sweet spot? Right before your roof hits the surcharge threshold. For most carriers with asphalt shingles, that's around year 13-15. You avoid emergency replacement, get your pick of contractors, and maximize your discount years.

Here's where things get tricky: if your current roof is young and healthy, replacement won't help your premiums much. You can't discount your way below standard rates by replacing a perfectly good 10-year-old roof. The math only works when you're either facing surcharges or upgrading to superior materials in high-risk areas.

Roof Replacement Discounts by Material Type

Your material choice directly affects both your upfront costs and your ongoing insurance bills. Standard three-tab shingles set the baseline—everything else gets measured against them.

Architectural shingles (the thicker, fancier-looking ones) typically earn you an extra 2-5% off compared to basic three-tabs. They resist wind better and last longer, which underwriters appreciate enough to trim your premium slightly.

Metal roofing hits the discount jackpot in most markets. Expect 10-20% reductions, sometimes more. Why? Metal doesn't burn, it sheds snow easily, it handles wind brilliantly, and it lasts 40-70 years. In wildfire zones like Colorado's Front Range or California's Sierra foothills, metal roof discounts can exceed 25%. You're looking at a $15,000-$30,000 installation cost, but the insurance savings help justify that expense.

Tile roofing is complicated. In fire-prone areas, Class A fire-rated tile can save you 15-30% annually. But in hail country? Some insurers actually charge more for tile because hail cracks it so easily. I've seen Texas homeowners get quoted higher premiums after installing expensive concrete tile, much to their shock. The weight issue matters too—older homes often need structural reinforcement to support tile, adding $5,000-$15,000 to your project cost.

Slate looks impressive and lasts over 100 years, but it doesn't generate proportional insurance savings. Yes, underwriters like the durability. However, they worry about repair costs when something does go wrong. Very few contractors work with slate anymore, which means expensive repairs and higher claim severity. You might save 8-12%, which doesn't match slate's premium price tag.

Impact-Resistant Roofing Discounts

Class 4 impact-resistant shingles undergo serious testing—manufacturers literally shoot 2-inch steel balls at them from 20 feet up. If the shingle survives without cracking or tearing, it earns the UL 2218 Class 4 rating.

States with serious hail problems—Texas, Colorado, Oklahoma, Kansas, Missouri—legally require insurance companies to offer discounts for Class 4 roofing. We're talking 15-35% savings in many cases. That discount often exceeds what you paid extra for the impact-resistant materials, making this a no-brainer financial decision.

One catch: read the fine print on these discounts. Some carriers apply the 30% to your entire premium. Others only discount the wind/hail portion of coverage, which might be 25-40% of your total bill. A "30% discount" on 30% of your premium means you're actually saving 9% overall. Still good, but not as good as it sounds in the marketing materials.

CertainTeed's Integrity Roof System, GAF's Timberline HDZ, and Owens Corning's Duration Storm are popular Class 4 products. They cost $50-$100 more per square (100 square feet) than standard shingles. On a typical 2,000 square foot roof, that's an extra $1,000-$2,000 upfront. But if you're saving $400-$600 annually on insurance, you break even in 2-4 years.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Wind and Hail Rating Considerations

Wind ratings tell you how fast the wind can blow before your shingles start flying off. Most products carry ratings from 60 mph (pretty weak) to 130 mph (Category 3 hurricane territory).

Coastal folks care intensely about wind ratings. Florida building code sets different requirements for different zones—Miami needs better protection than Tallahassee. Installing a roof rated for 130 mph winds in an area requiring only 110 mph can knock 5-15% off your premium.

Proper installation matters more than most people realize. A high-wind-rated shingle installed incorrectly performs worse than a standard shingle installed correctly. Six nails per shingle instead of four, sealed tabs, and proper starter strips make huge differences. Some carriers require certification from your contractor that they followed enhanced installation patterns. Without that certification, you don't get the full discount.

Here's something confusing: hail ratings and wind ratings don't always match up. You can buy Class 4 impact-resistant shingles with mediocre wind ratings, or high-wind shingles that won't survive hail well. Properties facing multiple threats need to prioritize. An Oklahoma home probably needs impact resistance first (hail happens there constantly) and wind resistance second. A Texas Gulf Coast home reverses those priorities—hurricanes threaten more than hail.

How Much You Can Save on Premiums

I usually see clients save 8-18% after roof replacement, assuming they had an older roof getting surcharged. The homeowners who save the most are those who combine a new roof with other upgrades like impact-resistant windows or a reinforced roof deck. I've watched total premiums drop 40% when someone takes a comprehensive approach to property hardening

— Sarah Mitchell

Real-world savings run anywhere from 5% to 35% annually, depending on what you're replacing and what you're installing.

Here's a concrete example. Sarah owns a home in suburban Denver. Her 22-year-old asphalt roof triggered a 15% age surcharge last year, bumping her premium from $1,800 to $2,070. She installed a Class 4 impact-resistant roof last month for $16,500. Her insurer (State Farm) removed the age surcharge and applied a 22% impact-resistant discount. Her new premium: $1,404 annually. She's saving $666 per year.

Now the hard part: that $16,500 roof replacement takes 25 years to pay for itself through insurance savings alone. This illustrates why insurance discounts shouldn't drive your replacement decision by themselves. Sarah needed a new roof regardless—her old one was leaking. The insurance savings just make the pill easier to swallow.

Geography creates massive variations in potential savings. Coastal properties see dramatic premium swings. A Jacksonville, Florida homeowner might pay $5,200 yearly with an aging roof but only $3,100 after installing a new impact-resistant, high-wind-rated system. That $2,100 annual savings changes the payback calculation completely—now the roof pays for itself through insurance savings in 8-10 years.

Meanwhile, someone in rural Minnesota with low weather risk might only drop their $1,100 premium to $1,000 with a new roof. That $100 yearly saving is nice, but it's not influencing the replacement decision.

Here's a comparison of typical discount ranges by material and age:

| Roofing Material Type | Brand New (0-5 Years) | Newer (6-10 Years) | Aging (11-15 Years) | Old (16+ Years) |

| Basic Asphalt (3-Tab) | 0-5% credit | 0-3% credit | Standard rate | 10-20% surcharge |

| Architectural Asphalt | 2-7% credit | 2-5% credit | Standard rate | 10-20% surcharge |

| Class 4 Impact-Resistant | 15-35% credit | 12-30% credit | 5-15% credit | 5-15% surcharge |

| Metal Roofing Systems | 10-25% credit | 8-20% credit | 5-15% credit | Standard rate |

| Tile (Wildfire Zones) | 15-30% credit | 12-25% credit | 8-18% credit | Standard rate |

| Tile (Hail Zones) | 5% surcharge | 5% surcharge | Standard rate | 10-20% surcharge |

These percentages show how insurers adjust your rate compared to baseline pricing. Surcharges mean you pay extra, credits mean you pay less.

Steps to Get Your Insurance Discount After Replacement

Your insurance company won't magically discover your new roof and send you a refund check. You need to actively request the discount with proper documentation.

Start by calling your agent before you even get contractor quotes. Ask these specific questions: "What new roof discounts do you offer?" "Which materials qualify for maximum discounts?" "Do I need to use specific contractors?" "What documentation will you require afterward?" This five-minute conversation prevents expensive mistakes like using materials your insurer won't recognize.

Before work begins, secure all required building permits. Every municipality handles this differently—some charge $50, others charge based on project value. Skipping permits to save $200 can cost you thousands if your insurer discovers unpermitted work and denies your discount (or worse, questions your coverage).

During installation, make absolutely certain your contractor follows the manufacturer's specifications exactly. Those installation manuals aren't suggestions—they're requirements. Deviation from prescribed methods voids product warranties. Since insurers verify warranty status when processing discount requests, improper installation kills your savings despite using approved materials.

After your contractor finishes, collect these documents:

- Signed-off final inspection from your city/county building department

- Itemized paid invoice showing specific materials used, installation date, contractor details

- Full manufacturer warranty paperwork (they should register this for you)

- Before and after photos from multiple angles

- Contractor's license number and proof of insurance

- Wind mitigation inspection report if you're in Florida, Texas, or other states where these are standard

Package everything together and submit it to your insurance company within 30 days of completion. Don't just email random documents—call first, ask where to send documentation, get a specific claims adjuster or customer service rep's name, and confirm they received everything.

Most carriers need to re-inspect before applying discounts. This inspection confirms your roof's condition, verifies proper installation, and documents specific features qualifying you for credits. Schedule this quickly. Every month you delay is a month you're overpaying.

In wind mitigation states, you'll need a licensed wind mitigation inspector to complete specialized forms (the OIR-B1-1802 in Florida, for example). This costs $75-$150 but often unlocks $300-$800 in annual savings. The inspector documents roof deck attachment, roof-to-wall connections, roof geometry, and other technical factors.

Follow up aggressively if your next bill doesn't reflect the changes. Insurance companies make mistakes constantly. I've seen situations where everything was approved but the billing department never updated the customer's rate. Check your declarations page carefully—verify they've updated your roof age and material type correctly.

Common Mistakes That Prevent Insurance Savings

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Several common errors can eliminate your savings or create coverage problems.

The biggest mistake? Never telling your insurance company about the new roof. Some folks assume their carrier will eventually notice during routine reviews. Bad assumption. If you file a claim and your policy still lists a 20-year-old roof when you actually have a 2-year-old roof, the carrier will question everything. They might investigate for misrepresentation or coverage fraud. Just tell them immediately and avoid this mess.

Choosing cheap materials without considering insurance impacts costs you money long-term. Maybe you saved $2,500 by going with basic shingles instead of Class 4 impact-resistant ones. But if those Class 4 shingles would have saved you $400 annually, you break even in six years and lose money every year after that.

Hiring unlicensed contractors creates multiple problems. Many insurers specifically require licensed contractors to perform work before they'll apply discounts. Plus, if your unlicensed contractor damages your property or disappears before finishing, you have limited legal recourse. Always verify licensing through your state's contractor licensing board, confirm they carry both liability and workers comp insurance, and check references.

Skipping permits might save you a couple hundred dollars and some hassle. It will cost you thousands in lost discounts and potentially void your coverage. Most carriers specifically ask about permits when you request new roof discounts. Some policy terms explicitly state that unpermitted work voids coverage for claims related to that work.

Waiting to contact your insurer until renewal wastes months of savings. Finish your roof in April, wait until your November renewal to mention it, and you've thrown away seven months of reduced premiums. Call them the week after completion to get immediate mid-term policy adjustments.

Assuming every insurance company offers identical discounts leads to missed opportunities. Your roof replacement is actually perfect timing to shop for new insurance coverage. If your current carrier offers a weak 5% new roof discount, competitors might offer 20% for the exact same roof. Get quotes from at least three different companies after your roof is complete.

Failing to increase your dwelling coverage limits after replacement causes problems during claims. Your new $18,000 roof just increased your home's replacement cost value. If you don't bump up your coverage limits to match, you're underinsured. Don't reduce coverage limits trying to keep premiums low after spending serious money improving your property.

Frequently Asked Questions

Can a new roof lower your home insurance? Absolutely. Most homeowners see savings between 5-35% depending on what they're replacing, what materials they choose, and where they live. The biggest reductions happen when you're replacing an old roof that's already triggering age-based surcharges, especially if you upgrade to impact-resistant or high-wind-rated materials in areas where storms happen frequently.

That said, insurance savings alone rarely justify spending $8,000-$30,000 on roof replacement. Make this decision based on your roof's actual condition and remaining lifespan first. The premium reductions are a nice bonus, not the main reason to pull the trigger.

When you do replace your roof, maximize your insurance benefits by choosing materials that qualify for your carrier's best discount programs, hiring properly licensed and insured contractors, pulling all required permits, and immediately notifying your insurer with complete documentation. Don't assume anything happens automatically.

Also, don't assume your current insurance company offers the best rate for your improved property. Shop around after installation. Your brand-new storm-resistant roof makes you an attractive customer that competing insurers want to win over. The combination of a properly installed new roof and competitively priced insurance coverage optimized for your specific situation gives you both physical protection and financial protection that accurately reflects your home's actual risk profile.