Person reviewing health insurance documents and medical bills at a desk

What Is Out of Pocket Maximum for Health Insurance?

Content

Your out-of-pocket maximum represents your annual spending ceiling for covered medical care. After your healthcare expenses hit this dollar amount, your insurance picks up the entire tab—every single bill—until your plan year ends and the cycle starts fresh.

Here's what makes this number so valuable: imagine facing a cancer diagnosis, serious car accident, or complicated pregnancy. Medical bills could easily climb into six figures, but your personal financial responsibility stops at your out-of-pocket maximum. After that threshold? Your insurer handles everything else at no additional cost to you.

For 2026, federal law caps this maximum at $9,450 for individual plans and $18,900 for family coverage—though plenty of plans set lower limits. Your specific plan documents spell out your exact number.

Understanding this ceiling matters when comparing insurance options. You might spot a plan charging $250 monthly with a $9,000 maximum, while another costs $450 monthly but caps your expenses at $4,500. Which saves you money? That depends entirely on how much care you'll actually need. The low-premium plan gambles you'll stay healthy; the high-premium option protects you if things go sideways.

How the Out of Pocket Maximum Works

Think of this maximum as a meter running all year long. Each deductible payment, every copay, all coinsurance—they add up automatically as your insurance company processes claims. You're not manually submitting anything special to track this; the system does it behind the scenes.

Let me walk you through a real example. Sarah carries a plan with a $6,000 ceiling. March brings surgery requiring her full $1,500 deductible plus $800 in coinsurance—she's now at $2,300. June's physical therapy sessions add $1,200 in copays, bringing her to $3,500. By September, specialist appointments and medications push her total to $6,000. What happens next? From September through December 31, Sarah doesn't pay another cent for covered care. No copays at the pharmacy. No coinsurance for follow-up appointments. Nothing.

But here's the catch: January 1 rolls around and that meter resets to zero. Doesn't matter if you maxed out in February or November—everyone starts from scratch each year.

You won't receive a congratulatory letter or updated insurance card when you hit your maximum. The transition happens automatically in your insurer's computer system. Your provider's office sees your coverage jumped to 100% and stops billing you for copays or coinsurance. Simple as that.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Family plans add complexity with dual maximums. Each person has an individual limit (usually half the family total), and the family shares an overall limit. Hit either threshold and you've triggered full coverage—for that person or everyone, depending which maximum got reached first.

What Counts Toward Your Out of Pocket Maximum

These expenses all chip away at your annual limit:

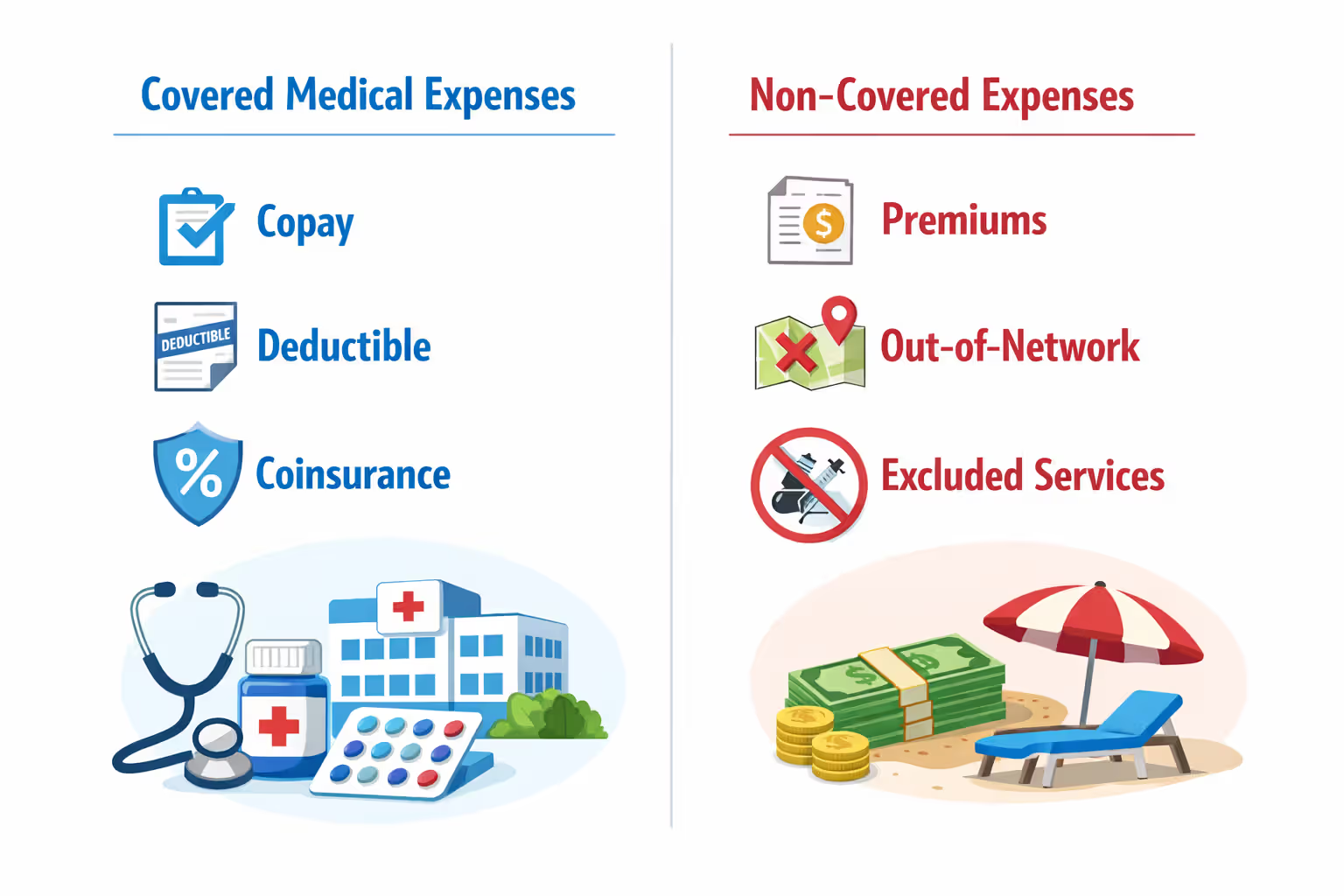

Deductibles: That initial chunk you pay before insurance kicks in? It counts dollar-for-dollar. Pay $2,000 to satisfy your deductible, and you're already $2,000 closer to your maximum.

Copayments: Every $30 primary care visit, $50 specialist appointment, $15 prescription—all of it accumulates. These small amounts seem insignificant until you're managing a chronic condition with weekly appointments and multiple medications. Then they add up fast.

Coinsurance: After satisfying your deductible, you split costs with your insurer. If that split leaves you paying 20% of a $10,000 surgery ($2,000), your entire share counts toward the maximum.

Covered prescription costs: Drug copays and coinsurance for medications your plan covers contribute to your total. The keyword here is "covered"—your plan's formulary determines what qualifies.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

What Doesn't Count Toward Your Out of Pocket Maximum

Several categories of spending exist completely outside this protection:

Monthly premiums: Your regular insurance payment—whether $200 or $800 monthly—doesn't move the needle on your out-of-pocket maximum. You could spend $9,600 annually on premiums, but from your maximum's perspective, you're still at zero.

Out-of-network care: Choose a doctor outside your network and you're playing a different game entirely. That $3,000 you paid an out-of-network specialist? Typically worthless for reaching your in-network maximum. Some plans offer separate out-of-network maximums, but they're astronomical by comparison.

Excluded services: Your plan doesn't cover fertility treatments? Cosmetic procedures? Those expenses might as well be invisible. Spend $10,000 on treatments your policy excludes and you've made zero progress toward your maximum.

Balance billing amounts: When out-of-network providers charge beyond your insurance's approved rates and bill you the difference, those extra charges generally don't count. Recent laws have reduced surprise billing in emergencies, but gaps remain.

Services exceeding plan limits: Maybe your plan covers 30 chiropractic visits yearly. Need 40 visits? Those last 10 you're funding entirely out-of-pocket don't contribute to your maximum.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Out of Pocket Maximum vs. Deductible

People constantly mix up these terms, but they're measuring different things. Your deductible comes first—it's what you'll pay before your insurance starts sharing costs. Your out-of-pocket maximum includes that deductible plus everything else you'll pay until you hit the annual ceiling.

Michael's plan illustrates this perfectly: $3,000 deductible, $7,000 out-of-pocket maximum. He breaks his leg in January. First, he covers that entire $3,000 deductible. Then his plan starts paying 80% while he pays 20% coinsurance on additional care. That 20% continues adding up—along with any copays—until his combined spending (deductible plus cost-sharing) reaches $7,000. Cross that line and his insurance handles 100% of covered services through year's end.

Your deductible always sits inside your out-of-pocket maximum, never separate. You can't have a situation where you pay a $5,000 deductible and then face an additional $5,000 maximum on top—the maximum encompasses everything.

| Feature | Deductible | Out of Pocket Maximum |

| What it means | Your upfront costs before insurance shares the bill | Your absolute spending limit for covered care annually |

| Payment timing | Right away when you start using your plan | Continuously until you reach the annual cap |

| Contributing expenses | Only initial costs before cost-sharing begins | Your deductible plus copays plus coinsurance combined |

| Annual restart | Resets January 1 each year | Resets January 1 each year |

| Common amounts (2026) | $1,500–$5,000 individual plans | $5,000–$9,450 individual plans |

| How they connect | Forms part of your out-of-pocket maximum | Contains your deductible plus all other cost-sharing |

Here's something that trips people up: some plans waive your deductible for certain services. Preventive care like annual checkups costs nothing regardless of your deductible status. Many plans charge just a copay for primary care visits before you've met your deductible. But those copays? They're still marching you toward your out-of-pocket maximum.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

What Does the Out of Pocket Maximum Cover

Your maximum protects you for essential health benefits defined under the Affordable Care Act. Hit that ceiling and your insurer covers 100% of these services:

Medical care: Hospital admissions, surgical procedures, emergency room treatment, urgent care visits, physician appointments, specialist consultations, diagnostic testing, laboratory work, and imaging studies all qualify. Need an MRI, comprehensive bloodwork, and three specialist follow-ups after maxing out? You're not paying a dime.

Prescription medications: Drugs on your plan's formulary—both generic and brand-name—receive full coverage once you've hit the threshold. Your $300-per-month specialty medication suddenly costs zero.

Mental health and substance abuse services: Therapy appointments, psychiatric care, inpatient behavioral health treatment, and addiction recovery programs qualify as essential benefits. They receive identical protection as physical healthcare.

Pregnancy and newborn services: Prenatal appointments, delivery costs, postnatal checkups, and infant care all fall under the maximum. Max out your plan during pregnancy? The rest of your maternity care costs nothing.

Preventive care: These services typically cost nothing anyway (free regardless of deductible or maximum status), but any cost-sharing that somehow applies would count toward your limit.

But this protection comes with boundaries. You're only covered for in-network providers delivering services your plan actually covers. Choose an out-of-network hospital or receive excluded treatments, and your out-of-pocket maximum offers zero protection. You must also follow plan requirements—getting prior authorization when mandated, using designated pharmacies, obtaining referrals if required.

Annual Limits and Coverage Caps

Federal regulations set the absolute ceiling for ACA-compliant plans, but insurers can choose any amount below that maximum. For 2026, federal caps sit at $9,450 individual/$18,900 family. These numbers adjust yearly based on healthcare inflation and economic trends.

Individual plans often undercut federal limits to attract members. You'll find marketplace options with $6,000 individual maximums or employer coverage with $5,000 caps. Lower maximums mean superior financial protection, but expect higher monthly premiums in exchange. You're essentially prepaying for cost certainty.

Family coverage operates with more complexity than most people realize. Your family plan includes both an aggregate family maximum and embedded individual maximums. The family's combined expenses might trigger the family threshold first, covering everyone at 100%. Alternatively, one person's costs could reach the embedded individual limit (no more than $9,450 in 2026), giving just that family member full coverage while others continue paying cost-sharing.

The Martinez family demonstrates this perfectly. Their plan sets a $9,000 individual embedded maximum and $18,000 family aggregate maximum. Their son needs extensive treatment, racking up $9,000 by June. He now gets 100% coverage through December, even though the family hasn't touched $18,000 yet. If other family members need care and collectively everyone hits $18,000, the entire family receives full coverage.

Plan categories significantly influence these limits. High-deductible health plans (HDHPs) compatible with Health Savings Accounts follow different federal rules. For 2026, HDHPs must carry minimum deductibles of $1,650 individual/$3,300 family, with out-of-pocket maximums capped at $8,300/$16,600 respectively—actually lower than standard ACA limits.

Grandfathered plans predating the ACA aren't bound by these requirements. Catastrophic plans available to young adults sometimes feature different structures. Never assume your plan matches federal maximums—always verify your specific policy's limits.

How to Use Your Out of Pocket Maximum When Filing Claims

Claims filing mostly happens without your involvement. Visit an in-network provider and they handle everything—submitting claims, receiving payment determinations, calculating your portion, updating your annual accumulation. You'll get an Explanation of Benefits (EOB) showing the math.

Your job focuses on vigilant tracking. Most insurers offer online portals or mobile apps displaying your year-to-date progress toward the maximum. Check monthly to confirm their numbers match your records. Insurance companies make mistakes—copays get missed, claims process incorrectly, bills disappear into administrative black holes.

Maintain your own records. Build a simple spreadsheet: date, provider name, service type, amount paid, running total. File every receipt, EOB, and payment confirmation. Approaching your maximum makes this documentation critical for resolving discrepancies.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Hitting your out-of-pocket maximum shouldn't feel like anything special. No new card arrives. No ceremony occurs. Your insurance card stays identical. Present it normally at appointments. The provider's billing system should recognize your 100% coverage status and stop requesting copays or coinsurance.

If a provider demands copays after you've maxed out, pause before paying. Politely mention you've reached your annual limit and ask them to verify with your insurance company. Most billing departments can confirm this instantly. If they insist on collecting payment, pay under written protest and immediately file a dispute with your insurer.

Denied claims demand persistence. Your insurer denies a claim and excludes it from your maximum accumulation? You've got appeal rights. Request detailed written denial reasoning. Common culprits include billing code errors, missing prior authorization paperwork, or services deemed medically unnecessary. Proper documentation from your provider overturns many denials.

File appeals in writing with comprehensive supporting documentation, respecting deadlines (typically 180 days for initial appeals). Internal appeals that fail qualify for external review by independent organizations. This external review costs you nothing and frequently reverses insurer decisions.

Out-of-network care often requires manual claim filing. Get itemized bills from providers, complete your insurer's claim forms, and submit everything via mail or online portal. Even if these costs don't benefit your in-network maximum, filing creates documentation and might contribute to a separate out-of-network maximum if your plan offers one.

Common Mistakes People Make With Out of Pocket Maximums

Counting premiums as out-of-pocket expenses: People often calculate they're spending $9,600 annually on a plan charging $800 monthly premiums and assume they're close to a typical maximum. But premiums exist in a completely separate universe from your out-of-pocket maximum. That $9,600 in premiums contributes exactly zero toward your limit.

Ignoring network boundaries: Choosing an out-of-network specialist for their stellar reputation or convenient location can wreck your financial planning. Those out-of-network expenses usually accomplish nothing toward your in-network maximum. You might drop $4,000 on out-of-network care while your in-network accumulation sits stubbornly at zero. Unless you're facing an emergency or genuinely no in-network alternatives exist, straying outside your network exposes you financially.

Trusting insurance company tracking blindly: Relying exclusively on your insurer's tracking system invites problems. Billing mistakes, processing delays, and coding errors can leave your accumulation wildly inaccurate. Discovering in November that your insurer's records miss $2,000 creates unnecessary panic and potential financial harm.

Shopping plans based purely on monthly cost: A plan charging $300 monthly with a $9,000 maximum looks cheaper than one costing $500 monthly with a $5,000 maximum, right? Run the worst-case numbers: Plan A totals $12,600 annually ($3,600 premiums plus $9,000 maximum); Plan B totals $11,000 ($6,000 premiums plus $5,000 maximum). For anyone anticipating significant medical needs, Plan B actually costs less. Always calculate total potential exposure, not just monthly premium costs.

Forgetting the annual reset: Maxing out in October delivers just three months of worry-free coverage. Come January 1, you're starting from scratch regardless of when you hit your limit last year. If you've got ongoing care needs, strategically timing elective procedures before December 31 can maximize your coverage value. Otherwise, that expensive medication or weekly therapy restarts cost-sharing requirements once the new year begins.

Misunderstanding family maximum mechanics: Parents sometimes believe each family member gets an individual maximum equal to the family total. Reality works differently—the family maximum represents combined spending for everyone. One member's catastrophic illness might consume the entire family maximum, inadvertently triggering full coverage for everyone else. Grasping this dynamic helps strategically plan care across multiple family members.

Your out-of-pocket maximum represents the single most important number in your entire health plan, yet it's the feature people understand least clearly. I've watched families select plans purely based on premium costs—low monthly payments, sky-high maximums—then face devastating financial consequences when serious illness strikes. Always evaluate insurance options assuming worst-case medical scenarios rather than hoping for the best. Your out-of-pocket maximum defines your true financial risk exposure

— Jennifer Martinez

Frequently Asked Questions About Out of Pocket Maximums

Your out-of-pocket maximum functions as crucial financial protection, establishing the absolute ceiling on your annual spending for covered healthcare services. Mastering how this limit operates, understanding what expenses contribute to it, and recognizing how it differs from your deductible gives you power to make informed insurance choices and manage healthcare costs more effectively.

When comparing health plans, resist the temptation to focus exclusively on monthly premiums. Calculate your worst-case total exposure by adding annual premiums to your out-of-pocket maximum—that sum represents your absolute maximum spending if serious illness or injury strikes. During healthy years, you might never approach this ceiling, but having robust protection matters most when facing major health challenges.

Monitor your accumulation throughout the year, maintain detailed personal records, and regularly verify your insurance company's tracking matches your documentation. Stick with in-network providers whenever medically reasonable, since out-of-network care often provides zero credit toward your maximum while exposing you to potentially unlimited expenses. After reaching your maximum, take full advantage of complete coverage for any necessary care before year's end and the counter resets.

Your out-of-pocket maximum transforms unpredictable, potentially catastrophic healthcare expenses into manageable, capped costs. Understanding this essential protection helps you navigate the healthcare system with substantially greater confidence and financial security.