Person reviewing health insurance documents with medical items on a desk

What Is Health Insurance and How Does It Work?

Content

Health insurance functions as your financial shield against medical costs. Each month, you send payment to an insurance company. When illness strikes or injury occurs, that company shares the financial burden of your medical bills. Consider the alternative: pneumonia requiring a three-day hospital stay could drain $25,000 from your bank account. Emergency treatment for a broken leg might demand $7,500 in immediate payment. A serious car accident needing surgical intervention could leave most American households facing bankruptcy.

The financial mechanics work like this: insurance carriers gather monthly payments from millions of members. The vast majority won't require expensive medical interventions this year. However, certain members will battle cancer, undergo emergency operations, or manage chronic conditions generating medical bills in the hundreds of thousands. Premium payments from currently healthy members build a financial reserve that covers members experiencing serious medical events. Your protection exists because everyone chips in, spreading the financial impact across the entire membership rather than crushing individuals who face medical emergencies.

Understanding Health Insurance Basics

The health insurance definition breaks down into three key players. You serve as the policyholder—the person purchasing the coverage. Your insurance company enters a contractual commitment to share payment of your medical expenses according to specific terms. Healthcare providers including doctors, hospitals, and clinics deliver actual treatment and generate bills for their work.

Picture a triangular relationship. Your commitment includes paying monthly premiums and adhering to plan guidelines. The insurance carrier commits to funding certain medical costs based on policy language. Medical professionals provide the healthcare services and receive payment from you, the insurance company, or shared between both parties.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Risk pooling creates the foundation for this entire system. Consider ten individuals, each facing a 10% probability of requiring a $50,000 surgical procedure this year. When everyone contributes $5,500 to a collective fund, that generates $55,000—sufficient resources to cover whichever member needs the operation. No single person needed to stockpile $50,000 independently. Insurance carriers apply this identical mathematical principle across millions of members, employing complex actuarial analysis to set premium prices ensuring total collections cover all submitted claims plus operational expenses and profit margins.

Your policy represents a binding legal document outlining covered medical services, your financial obligations, and the insurer's payment responsibilities. Plan designs vary dramatically. One might feature a $500 deductible paired with $50 copays when seeing specialists. Another carries a $5,000 deductible while demanding lower monthly premium payments. Reviewing your policy documentation before requiring medical attention prevents shocking billing surprises and enables realistic budgeting for healthcare expenses.

How Health Insurance Works in Practice

You start by sending that monthly premium payment—essentially your membership dues for maintaining active coverage. This financial obligation exists regardless of whether you schedule any doctor appointments that month. Missing premium payments gives your insurer grounds to terminate your coverage, exposing you to 100% personal liability for any medical expenses.

With active coverage, you can access physicians and receive medical treatment. Following your appointment, the doctor's billing department transmits a claim to your insurance carrier. Your insurer examines it, determines what falls under coverage based on your particular plan design, and forwards payment directly to the healthcare provider for their approved portion. Your responsibility includes any deductible amounts, copayment fees, or coinsurance percentages—collected either during your visit or through subsequent provider billing.

The typical sequence flows like this: book appointment → obtain medical services → provider transmits claim to insurance company → insurer evaluates and compensates provider → you receive an Explanation of Benefits displaying charged amounts, insurance payments, and your balance. When you question the insurance company's determination, the appeals process offers recourse.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Premiums, Copays, and Coinsurance

Your monthly premium serves merely as the admission price. A copayment represents a fixed dollar sum you remit for particular services—perhaps $25 for primary care visits or $10 for generic medications. Copays deliver predictability and typically fall outside deductible calculations.

Coinsurance means splitting expenses with your insurer through percentages once you've satisfied your deductible requirement. Imagine your plan carries 20% coinsurance. You schedule a $1,000 MRI scan. Your payment equals $200 while insurance handles $800. This percentage-based division continues until reaching your annual out-of-pocket maximum.

Certain plans eliminate all expenses for preventive care—yearly physical exams, influenza vaccinations, mammogram screenings. You remit zero copayment, zero coinsurance, and these appointments don't reduce your deductible. The reasoning? Identifying problems early (like discovering high blood pressure before it triggers a stroke) reduces expenses for both you and the insurance carrier long-term.

In-Network vs. Out-of-Network Providers

Your insurer establishes negotiated discount arrangements with specific doctors, hospitals, and medical facilities. These providers constitute your network. Remaining in-network delivers optimal rates plus complete coverage advantages. Venturing out-of-network exposes you to steeper bills because those providers haven't accepted discounted fee schedules—and your insurance may contribute less or deny payment entirely.

Concrete example: An in-network orthopedic surgeon might require a $40 copay for consultation appointments. That identical visit out-of-network could generate $250 in charges after your insurance contributes only minimal amounts or rejects the claim completely. HMO plan designs typically refuse covering out-of-network care except during genuine emergencies. PPO plans will provide coverage, though you'll shoulder substantially higher costs.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Prior to any non-emergency medical appointments, confirm the provider participates in your network. Networks undergo constant changes—that dermatologist accepting your insurance last year might have exited the network three months ago. Consult your insurer's digital directory, telephone to verify current status, then reconfirm with the medical office directly. A brief phone conversation can prevent thousands in unexpected medical bills.

What Does Health Insurance Cover

Federal regulations mandate most plans cover ten fundamental categories. Coverage includes physician consultations for illness, hospital treatment (both admitted stays and outpatient procedures), emergency department services, laboratory testing and diagnostic imaging such as X-rays or CT scans, prescription medications, mental health therapy and addiction treatment programs, pregnancy and infant care, pediatric services including dental and vision for children, and preventive medical care like cancer screenings and immunizations.

Preventive services receive special consideration. Following the Affordable Care Act, insurers must provide recommended preventive care without any cost to you—no copayment, no deductible applies. This encompasses annual wellness visits, blood pressure monitoring, cholesterol panels, mammography, colonoscopy procedures, and standard vaccinations. Utilizing these no-cost services can identify serious conditions like diabetes or colon cancer during highly treatable early stages.

Most plans exclude cosmetic procedures (face lifts, abdominoplasty), elective operations lacking medical necessity, experimental treatments, and numerous alternative therapies. Acupuncture or chiropractic treatment might receive restricted coverage—possibly 12 appointments annually. Adult dental and vision benefits usually require purchasing separate insurance contracts, although certain marketplace plans bundle basic services.

Coverage specifics fluctuate significantly between plan options. One might provide brand-name medication coverage while demanding a $75 copay. Another mandates attempting generic alternatives before authorizing brand-name versions. Your Summary of Benefits and Coverage—a standardized disclosure document every plan must supply—clarifies precisely what receives coverage. Review it before enrollment, not after receiving an unexpected bill.

Health Insurance Deductibles Explained

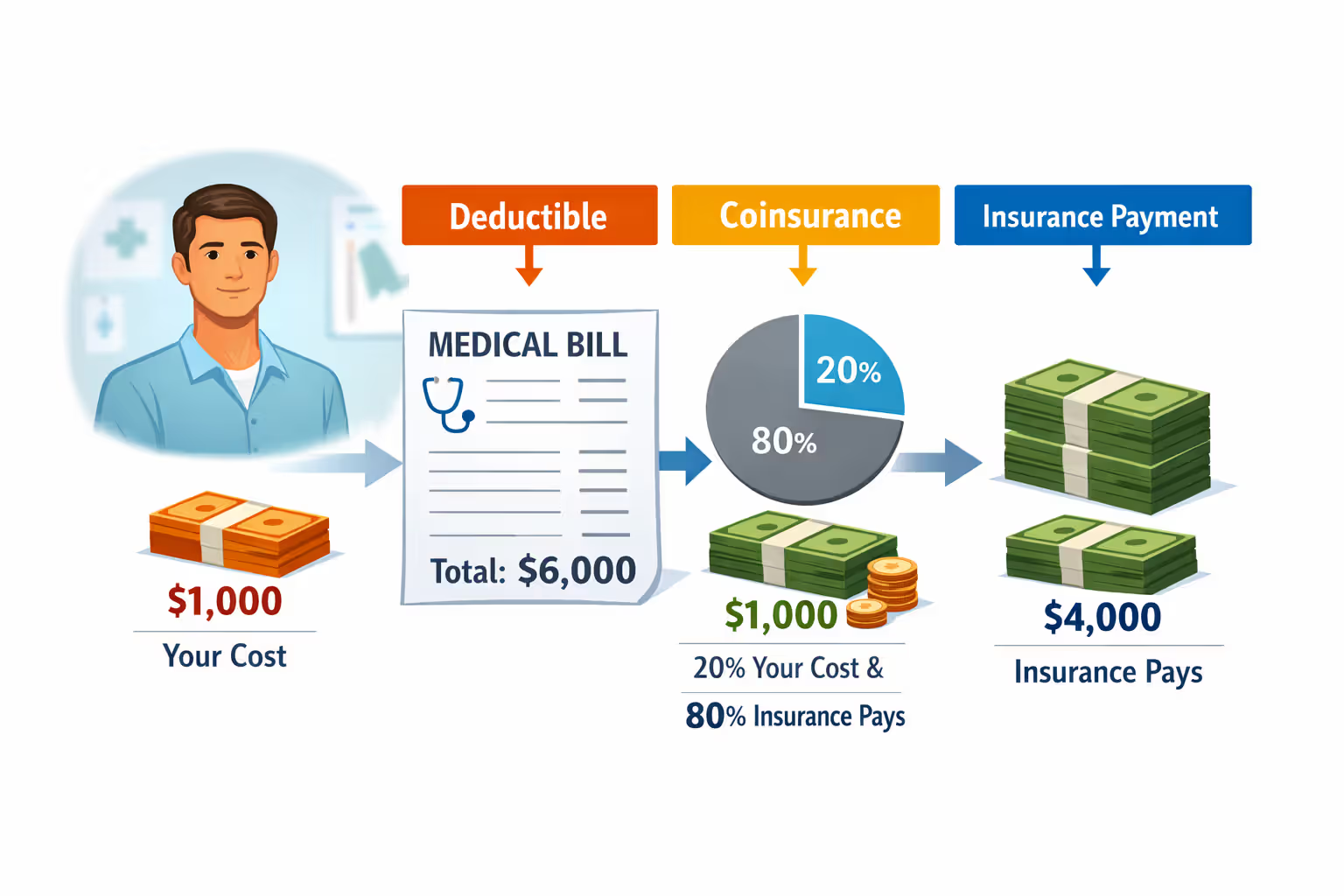

Your deductible represents the sum you personally fund each year before insurance begins contributing toward costs. Suppose you carry a $2,000 deductible. You bear financial responsibility for the initial $2,000 in covered medical services annually. After spending $2,000, your insurance activates and begins funding care based on your plan's copayment or coinsurance structure.

Deductibles restart annually—typically January 1st for marketplace plans or matching your employer's plan anniversary date. Money applied toward your deductible in December doesn't transfer to January. The tracking mechanism returns to zero. This timing explains why certain people rush scheduling procedures in December after satisfying their deductible—they want maximizing that advantage before the annual reset.

Concrete example: Your plan includes a $1,500 deductible with 20% coinsurance. During March, you fracture your arm. Emergency room care totals $3,000. You fund the first $1,500 (meeting your deductible). From the remaining $1,500, you contribute 20% ($300) while insurance provides 80% ($1,200). Your complete bill: $1,800. Throughout that year's remainder, you'll exclusively pay coinsurance on covered medical services because you already fulfilled your deductible.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

High-deductible health plans establish minimum deductibles of $1,650 for individual coverage ($3,300 for family plans) in 2026. Monthly premium costs run lower, though you fund more expenses before coverage begins. These pair effectively with Health Savings Accounts, allowing tax-free savings specifically for medical costs. Low-deductible plans charge steeper monthly premiums yet begin covering expenses sooner—preferable when managing ongoing health conditions or desiring predictable spending.

Selecting between high and low deductible options depends on your health situation and financial comfort with risk. Healthy individuals rarely requiring medical care often select high-deductible plans for premium savings. Someone controlling diabetes or families with young children might favor a low deductible despite premium increases, recognizing they'll probably reach that deductible threshold anyway.

Coverage Limits and Out-of-Pocket Maximums

Your out-of-pocket maximum establishes the ceiling on your spending for covered medical care annually. Upon reaching this threshold, insurance funds 100% of covered medical services through that year's conclusion. For 2026, federal regulations cap out-of-pocket maximums at $9,450 for individual plans and $18,900 for family coverage on marketplace plans, though numerous plans establish lower thresholds.

This maximum encompasses your deductible, copayments, and coinsurance—excluding your monthly premium costs. When your out-of-pocket max reaches $7,000 and you hit that in June, your insurer covers all subsequent costs through December without additional payments from you.

Let me illustrate a realistic scenario: You receive a leukemia diagnosis in February. Your plan design includes a $2,000 deductible, 20% coinsurance, and $6,500 out-of-pocket maximum. Treatment expenses total $150,000 for the year. You fund the complete $2,000 deductible initially. Then you contribute 20% of continuing costs until your cumulative spending (deductible plus coinsurance) hits $6,500. Beyond that point, insurance covers the remaining $143,500 without charging you. Your total annual cost: $6,500 plus your monthly premium obligations.

Annual limits restrict insurance payments for specific services within one year—such as 30 physical therapy appointments or $2,000 toward hearing aids. Lifetime limits would cap total benefit payments across your entire enrollment period. The Affordable Care Act prohibited lifetime limits on essential health benefits, preventing insurers from terminating coverage after you've consumed a particular dollar threshold. Limits may still apply to non-essential services like fertility treatments.

Out-of-pocket maximums shield you from financial ruin. Without these protections, serious medical conditions could evaporate your savings despite carrying insurance. When evaluating plans, examine the out-of-pocket max alongside premiums and deductibles—an inexpensive $200/month premium combined with a $9,000 out-of-pocket max could cost you substantially more during a difficult health year than a $400/month premium featuring a $4,000 maximum.

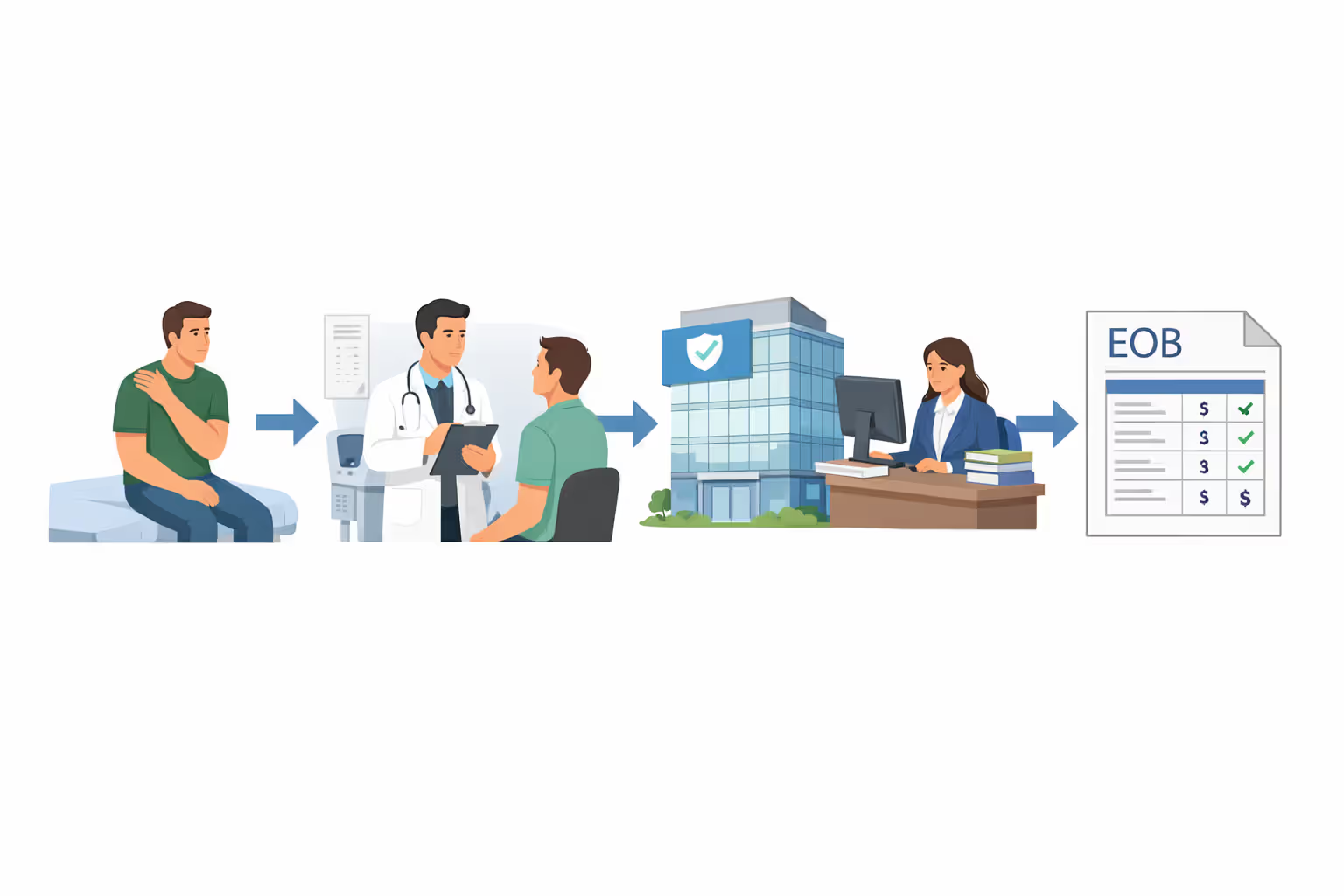

The Health Insurance Claim Process

The claims process initiates when you obtain medical services. For standard appointments, you simply present your insurance card and the medical office manages everything else. Understanding each step helps you identify billing mistakes and challenge denials effectively.

Step 1: Obtaining medical services. Your provider documents everything using standardized coding systems—ICD codes for medical diagnoses, CPT codes for performed procedures. Precise coding matters significantly because mistakes regularly trigger claim rejections.

Step 2: Provider transmits the claim. The physician's office or hospital facility forwards an electronic claim to your insurer detailing rendered services and associated charges. This typically occurs within days or weeks following your appointment.

Step 3: Insurer evaluates the claim. Your insurance company verifies whether services fall under your policy coverage, whether they represented medical necessity, whether the provider participates in-network, and whether you've satisfied your deductible. Complicated claims can require 30 days or longer.

Step 4: You obtain an EOB. Your Explanation of Benefits (not an invoice!) displays what the provider charged, the negotiated discount rate (frequently much lower), what insurance funded, and your remaining balance. It details how your deductible, copayment, or coinsurance was determined. Scrutinize every EOB carefully—billing mistakes occur frequently.

Step 5: Funding your portion. The provider invoices you separately for your responsibility. Cross-reference this invoice against your EOB to verify matching amounts. Notice discrepancies? Contact both the provider and insurer to achieve resolution.

Step 6: Pursuing appeals when necessary. Received a denial? You possess appeal rights. Frequent denial justifications include services determined lacking medical necessity, claims submitted incorrectly, or treatments requiring prior authorization that wasn't secured. Your insurer must clarify their denial reasoning and outline the appeals pathway. Numerous denials get reversed through appeals, particularly when your physician supplies supporting clinical documentation.

Monitor for frequent mistakes: providers entering incorrect codes, insurers assigning charges to the wrong family member's deductible, or duplicate billing. Maintain comprehensive records of all appointments, EOBs, and invoices. Challenge anything appearing incorrect immediately—billing disputes grow substantially harder resolving after 90 days pass.

Common Health Insurance Plan Types

Different plan structures provide varying degrees of flexibility and expense. Which performs best depends on your healthcare requirements, financial resources, and whether you have established physicians you want continuing to see.

| Plan Structure | Premium Expense | Provider Selection | Referral Requirement? | Out-of-Network Benefits |

| HMO | Most affordable | Must remain in network | Yes, through primary physician | Emergency situations only |

| PPO | Most expensive | Broad flexibility | No requirement | Yes, though significantly costlier |

| EPO | Moderate | Network only | No requirement | Emergency situations only |

| POS | Moderate | Network preferred, can venture out | Yes, through primary physician | Yes, though significantly costlier |

HMO plans require selecting a primary care physician who orchestrates all your medical care and supplies referrals to specialists. You must remain in-network except during emergencies. The advantage: most affordable premiums and predictable copayment fees.

PPO plans grant you maximum independence. Consult any physician without referrals, and out-of-network care receives coverage (though you'll contribute more). The compromise: steeper premiums and more intricate cost-sharing arrangements.

EPO plans merge HMO and PPO characteristics. No referrals needed for specialist consultations, though you must stay in-network. Premiums position between HMOs and PPOs.

POS plans unite elements from HMOs and PPOs. You designate a primary care coordinator, yet you can visit out-of-network providers when accepting higher costs.

Most employer-sponsored plans are PPOs or HMOs. Marketplace plans present all four structures. When you regularly see a particular specialist, verify they participate in-network before selecting a plan—switching plans to maintain your physician relationship might save money versus funding extremely high out-of-network charges.

Far too many consumers shop for health insurance examining solely the monthly premium without grasping how deductibles, copayments, and provider networks will impact their real-world costs. A plan appearing affordable can transform into an extremely expensive choice once you require medical care and realize you're unprepared for the cost-sharing structure. Invest time understanding the terminology—particularly what 'out-of-pocket maximum' genuinely means—before enrolling. That education can prevent thousands of dollars in expenses and tremendous stress when a health emergency strike

— Karen Pollitz

Frequently Asked Questions About Health Insurance

Health insurance converts unpredictable, potentially catastrophic medical expenses into manageable monthly obligations. Grasping how premiums, deductibles, copays, and out-of-pocket maximums function together helps you select coverage matching both your health requirements and financial capacity. The claims process might appear confusing initially, though knowing these steps enables you to identify billing errors and contest unjust denials.

No plan provides universal coverage or eliminates all expenses. Every plan balances monthly premium expenses, cost-sharing when requiring care, and flexibility in selecting providers. The optimal choice depends on your health condition, financial circumstances, and comfort with risk. Evaluate your options thoroughly during open enrollment, examine the details in your Summary of Benefits and Coverage, and confirm your preferred providers participate in-network before enrolling.

Healthcare carries high costs in the United States, yet insurance delivers essential financial protection. Whether you're comparing employer plan alternatives, exploring the marketplace, or assisting a family member understand their options, the time invested understanding these fundamentals pays dividends when you require medical treatment. Your health and financial security merit this attention.