Drivers after a minor car accident at a city intersection

What Is Car Insurance and How Does It Work?

Content

Picture this: you're driving home from work when someone runs a red light and crashes into your car. Within seconds, you're facing thousands in repair bills, medical expenses, and potentially a lawsuit. Without car insurance, you'd be writing checks out of your own bank account—possibly draining your savings or worse. That's exactly why car insurance exists.

Think of car insurance as a promise backed by money. Each month, you pay your insurance company a fee (your premium), and they promise to handle the financial fallout if something goes wrong with your vehicle. Maybe someone steals your car. Maybe hail the size of golf balls dents your hood. Maybe you accidentally rear-end someone at a stoplight. Your insurance company steps in to pay these bills according to what's written in your policy.

Here's the catch most new drivers miss: nearly every state legally requires you to carry at least basic coverage. Drive without it, and you're risking fines, license suspension, and personal financial catastrophe. But beyond just following the law, understanding the nuts and bolts of car insurance—from what different coverage types actually do to how claims work in real life—helps you avoid overpaying while staying properly protected.

Car Insurance Definition and Purpose

So what exactly counts as car insurance? In plain terms, it's a binding contract where an insurance company agrees to pay for specific vehicle-related financial losses. You commit to paying regular premiums, and they commit to covering damages spelled out in your policy documents. These damages might include fixing your car after a crash, paying someone else's medical bills if you injure them, covering legal defense costs if you get sued, or replacing your vehicle if it's stolen.

Why does this system even exist? Three big reasons.

Your bank account needs protection. Imagine causing an accident that puts two people in the hospital. Their combined medical care easily tops $200,000, plus there's vehicle damage, lost wages while they recover, and possibly pain-and-suffering claims. Without insurance, you'd be personally on the hook for every dollar. Many people would face bankruptcy. Your insurance policy absorbs these costs instead.

Innocent victims need compensation. If someone else crashes into you through no fault of your own, their insurance pays for your repairs and medical care. This system ensures that people injured in accidents can actually recover their losses rather than hoping the at-fault driver happens to have money saved.

The law demands it. Drive through any state except New Hampshire or Virginia, and you're legally required to carry minimum liability coverage. Even those two states impose strict financial responsibility standards—if you can't prove you can cover accident damages yourself, you'll face serious penalties. Virginia lets you pay an annual $500 fee to skip insurance, but you're still personally liable for any damage you cause, which could cost hundreds of thousands.

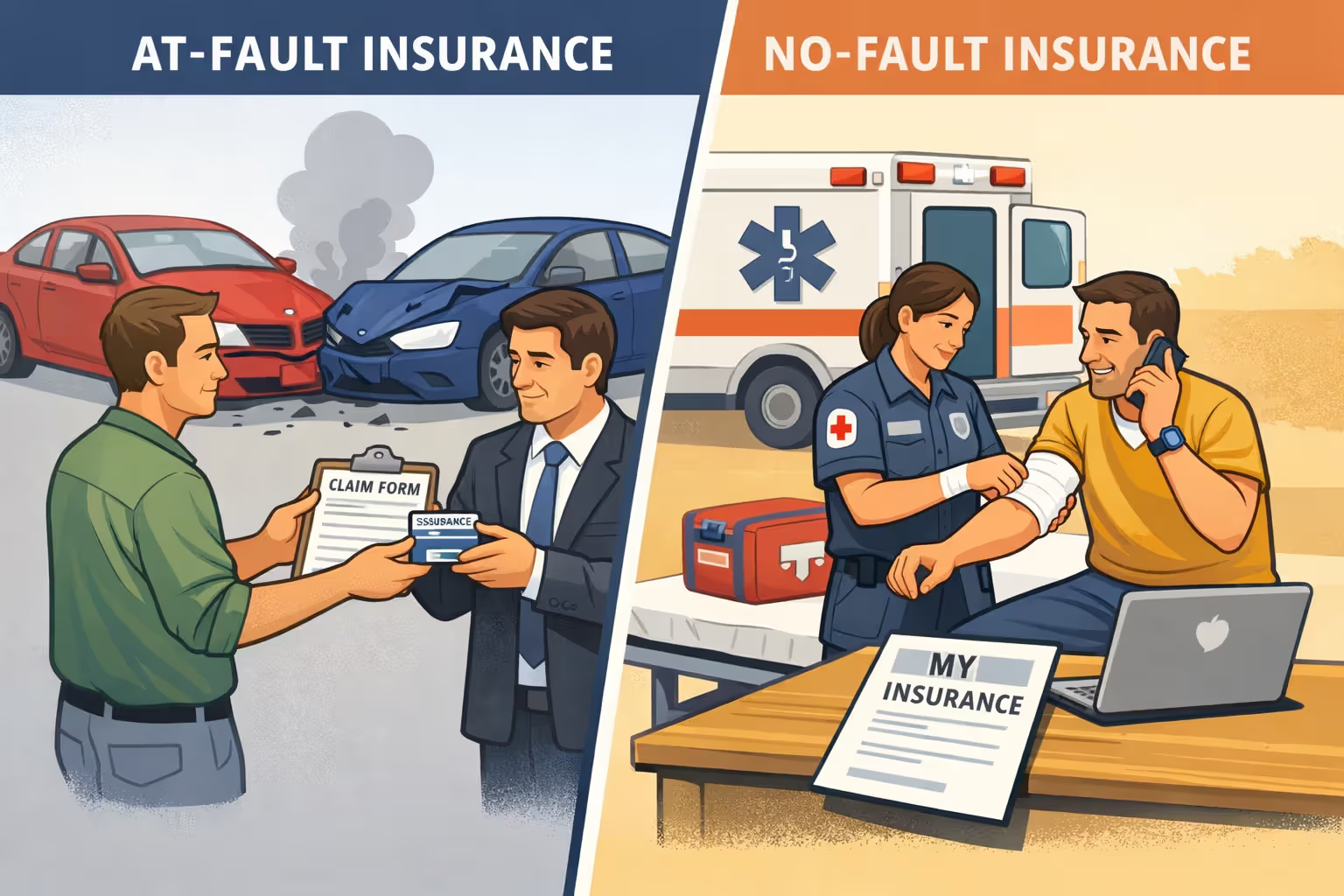

State requirements vary dramatically. Most states follow traditional "tort" systems where the at-fault driver's insurance pays everyone's damages. A dozen states use "no-fault" systems where your own insurance covers your medical bills regardless of who caused the crash. Minimum coverage requirements range from embarrassingly low (some states require just $25,000 per accident) to more reasonable levels. We'll dig into why state minimums are rarely adequate later.

Author: Caroline Halstead;

Source: talero.spotpariz.net

How Car Insurance Works

Your premium—the bill you pay monthly or twice yearly—keeps your policy active. Insurers don't pull premium amounts out of thin air. They calculate risk using dozens of factors about you personally. Your age matters (teens pay triple what middle-aged drivers pay). Your driving record counts heavily (one DUI can double your rates). Where you live makes a huge difference (Detroit premiums run four times higher than those in rural Wyoming). Even your credit score affects pricing in most states, since insurers have found that people with lower credit tend to file more claims.

The vehicle itself changes your costs dramatically. Insuring a practical Honda Accord costs far less than covering a Dodge Challenger Hellcat, not just because the Hellcat costs more to repair but because statistically, Hellcat drivers get into more accidents and file more comprehensive claims for theft. Insurers track claim histories for every vehicle model.

When you buy a policy, you're entering a contract for a set period—typically six months or a year. During that term, your premium stays fixed unless you make changes like buying a new car or adding a teenage driver. The policy itself is a hefty document spelling out exactly which situations trigger coverage, which scenarios are excluded, your deductible amounts, and maximum payout limits.

Here's how the business model works behind the scenes: insurers collect premiums from thousands of drivers, most of whom never file major claims. Those collected premiums fund payouts for the minority who total their cars or cause serious accidents. It's risk-pooling on a massive scale. This is why your clean driving record earns you lower rates—you're subsidizing the high-risk drivers less than they subsidize themselves.

Your policy auto-renews unless someone cancels it. At renewal time, expect your premium to change. Filed a claim this year? Your rate jumps. Turned 25? Your rate drops. Got married? Rate drops. Added a teenage son to your policy? Rate skyrockets. Insurers also adjust rates based on broader trends—if they're paying out more claims nationwide due to higher vehicle repair costs, everyone's premiums edge upward.

Smart drivers shop around at every renewal. Insurance companies fight hard for new customers with attractive rates but often raise premiums on loyal long-term policyholders who don't bother shopping. Comparing quotes from three or four insurers every couple years can save you hundreds annually.

What Does Car Insurance Cover

Here's where car insurance gets modular. You're not buying one product—you're selecting from a menu of coverage types, each protecting against different risks. Understanding what each type actually does prevents nasty surprises when you file a claim.

Liability Coverage

Liability coverage forms the foundation of every car insurance policy and represents the only coverage most states legally require. This coverage divides into two distinct parts: bodily injury liability and property damage liability.

Bodily injury liability handles the medical costs, lost income, pain-and-suffering claims, and legal defense fees when you hurt someone in a crash you caused. Let's say you're merging onto the highway, misjudge your speed, and sideswipe another vehicle. The other driver breaks their collarbone and misses six weeks of work. Your bodily injury coverage pays their hospital bills, orthopedic care, physical therapy, lost wages, and if they sue you, the attorney fees to defend you in court.

Property damage liability covers the cost of fixing or replacing other people's property you damage with your vehicle. This obviously includes other cars, but it extends further. Swerve off the road and demolish a mailbox? That's covered. Crash through someone's fence and into their garage? Covered. Knock over a utility pole? Covered (and utility poles can cost $15,000+ to replace).

Here's the critical detail many drivers miss: liability coverage pays zero dollars toward your own injuries or vehicle damage. It only protects others. This confuses people who assume their "insurance" means everything is covered. It's not.

Collision and Comprehensive Coverage

Collision coverage handles repairs to your own vehicle after a crash, regardless of who caused it. You rear-end someone because you were checking your phone? Collision pays. Someone runs a stop sign and T-bones you? Collision pays (though you might also file a claim against their liability insurance). You take a turn too fast on a mountain road and roll your car? Collision pays. The key word is "collision"—your vehicle colliding with another vehicle or object.

Comprehensive coverage protects your car from basically everything else: theft, vandalism, fire, flood, hail damage, hitting a deer, falling tree branches, riots, or even random acts of nature like a sinkhole swallowing your parked car. People sometimes call this "other-than-collision" coverage, which describes it perfectly.

Both coverage types are optional unless you're financing your vehicle. Lenders require them because they own your car until you finish paying off the loan, and they want their asset protected. Once you own your car outright and its value drops below about $3,000 to $4,000, many drivers drop these coverages. After all, if your 15-year-old car is worth $2,000 and you're paying $600 yearly for collision and comprehensive, you're essentially insuring yourself into the ground.

Author: Caroline Halstead;

Source: talero.spotpariz.net

Personal Injury Protection and Medical Payments

Personal Injury Protection—everyone calls it PIP—is mandatory in no-fault states (Florida, Michigan, New Jersey, and about nine others). PIP covers your medical bills, lost wages, and sometimes essential services like childcare if you're too injured to care for your kids. The key feature: it pays regardless of who caused the accident. You don't wait around for fault determination or fight with the other driver's insurance. Your own PIP kicks in immediately, covering expenses up to your policy limit (commonly $10,000 to $50,000).

Medical Payments coverage (MedPay) works similarly but simpler. Available in tort states, it pays medical and funeral expenses for you and your passengers after any accident, regardless of fault. Unlike PIP, MedPay doesn't cover lost wages or services—it's purely medical. Coverage limits run lower too, typically $1,000 to $10,000. Think of it as supplemental health insurance for car accidents. It pays your health insurance deductibles and co-pays that your regular health coverage doesn't handle.

Uninsured/Underinsured Motorist Coverage

Ready for a disturbing statistic? About one in eight drivers nationwide carries zero insurance, despite legal requirements. In some states like Mississippi and Michigan, uninsured rates hit 25%. Even more drivers carry only bare-minimum liability limits that won't come close to covering a serious accident.

Uninsured motorist coverage (UM) protects you when someone without insurance crashes into you and causes injuries or damage. The at-fault driver should pay, but they can't because they have no coverage. Your UM coverage steps in and pays instead.

Underinsured motorist coverage (UIM) activates when the at-fault driver has insurance, but their policy limits are too low. Suppose someone with $25,000 in liability coverage causes a crash that leaves you with $80,000 in medical bills. Their insurance maxes out at $25,000, leaving you $55,000 short. Your UIM coverage pays that gap (up to your UIM limit).

These coverages essentially provide liability protection that works in reverse—covering you when someone else should be paying but can't. Some states mandate UM/UIM coverage; others make it optional. Given how many uninsured and underinsured drivers exist, skipping this coverage is frankly reckless, especially since it's relatively cheap compared to other coverage types.

| Coverage Type | What It Protects Against | Situations It Covers | Annual Premium Range |

| Liability | Harm you cause to others' bodies and property | When you're responsible for a crash | $400–$1,200 |

| Collision | Your vehicle damage from crashes | Any impact with vehicles or objects | $300–$900 |

| Comprehensive | Your vehicle damage from non-crash events | Theft, weather damage, vandalism, animal strikes | $150–$500 |

| PIP/MedPay | Your medical costs and income loss | Any accident regardless of fault | $100–$400 |

| Uninsured Motorist | Your injuries when others lack coverage | At-fault driver has no insurance or flees the scene | $100–$300 |

Car Insurance Deductible Explained

Your deductible represents the amount you personally pay before insurance contributes anything to a claim. Deductibles apply only to collision and comprehensive coverage—not to liability, since liability pays other people, not you.

Here's how it works in practice. Your car gets keyed in a parking lot, causing $2,000 in paint damage. You have a $500 deductible on comprehensive coverage. You pay the first $500 toward repairs, and your insurer covers the remaining $1,500. Now imagine the damage costs only $350. Since that falls below your $500 deductible, you'd pay everything yourself—filing a claim wouldn't make sense.

Typical deductible options range from $250 on the low end to $2,000 on the high end, with $500 and $1,000 being most common. Choosing a higher deductible directly lowers your premium because you're accepting more financial risk yourself. A driver selecting a $1,000 deductible instead of $500 might save $300 yearly on premiums. Over five accident-free years, that's $1,500 saved—more than enough to cover the higher deductible if a claim eventually happens.

The trade-off is cash availability. Could you comfortably write a $1,000 check tomorrow if you crashed your car today? If that would strain your finances, stick with a lower deductible despite the higher premium. Many financially savvy drivers maintain emergency funds equal to their deductibles, ensuring they can handle claims without stress.

You pay your deductible per claim, not per policy period. File three separate comprehensive claims in one year (hailstorm, deer strike, theft), and you'll pay your deductible three times. Some insurers offer "vanishing deductibles" that decrease $50 to $100 annually for every year you avoid filing claims—a nice reward for safe driving.

Author: Caroline Halstead;

Source: talero.spotpariz.net

Understanding Coverage Limits

Every coverage type includes a maximum payout amount called your policy limit. Choosing appropriate limits ranks among your most important insurance decisions, yet many drivers barely understand what their limits mean.

Liability limits appear as three numbers separated by slashes, like 50/100/50. Breaking this down: the first number ($50,000) represents the maximum your insurer pays for one person's bodily injuries in an accident. The second number ($100,000) represents the total available for all injured people combined in one accident. The third number ($50,000) caps property damage payments per accident. Insurance pros call this "split limits" format.

Some insurers offer "combined single limits" (CSL) instead—one number like $300,000 that can be used for bodily injury or property damage in any combination. CSL provides flexibility. If you severely injure one person, the entire limit can go toward their care without being constrained by per-person caps.

State-mandated minimums are disturbingly inadequate. Many states require only 25/50/25 coverage. That's $25,000 for one person's injuries—an amount that wouldn't cover a moderate injury requiring surgery. A multi-vehicle pileup with several injured people could easily generate $500,000 or more in medical claims. When your liability limits run dry, you become personally responsible for excess damages. Plaintiffs can garnish your wages, empty your savings, and even force you to sell your home.

Financial advisors consistently recommend carrying liability limits at least equal to your net worth. Own $400,000 in assets? Carry at least $400,000 in liability coverage (or split limits like 250/500/100). People with substantial assets often buy umbrella policies—additional liability coverage that kicks in after auto policy limits exhaust, providing $1 million or more in protection for just a few hundred dollars yearly.

Collision and comprehensive limits equal your vehicle's actual cash value. If your car is worth $18,000, that's the maximum your insurer will pay if it's totaled, regardless of policy limits. You can't insure an $18,000 car for $30,000—remember, insurance restores you to your financial position before the loss, not better. Insurers prevent people from profiting from insurance claims.

I see the same mistake constantly: drivers obsessing over saving $15 monthly on premiums by choosing state minimum liability limits, not realizing they're exposing themselves to catastrophic financial risk. The difference in cost between 25/50/25 minimum coverage and 250/500/100 adequate coverage is typically just $30 to $50 per month. That extra $40 monthly could be the difference between a manageable insurance claim and losing your house in a lawsuit. Never, ever prioritize a cheap premium over adequate protection

— Jennifer Martinez

The Car Insurance Claim Process

Understanding how claims actually work in real life helps you navigate the stressful chaos after an accident. The process varies slightly by insurer and claim type, but follows this general pattern.

Step 1: Secure Safety and Gather Evidence. Right after an accident, check whether anyone needs immediate medical attention and call 911 if so. If vehicles are drivable and blocking traffic, move them to safety. Exchange information with other drivers: full names, phone numbers, insurance company names, policy numbers, and license plates. Take extensive photos—vehicle damage from multiple angles, the overall accident scene, street signs, traffic signals, skid marks, and anything else relevant. Avoid admitting fault or apologizing. Stick to factual statements when talking to police and other drivers.

Step 2: Contact Your Insurer Quickly. Call your insurance company within 24 hours—most offer round-the-clock claims reporting via phone or mobile app. You'll describe when, where, and how the accident occurred, plus provide the other driver's information. Even if you believe you weren't at fault, report it anyway. The other driver might blame you and file a claim against your policy. Your insurer needs to know immediately to protect your interests.

Step 3: Submit Your Formal Claim. If you're claiming collision or comprehensive coverage for your own vehicle damage, you'll file what's called a "first-party claim" with your insurer. If you're seeking compensation from another driver's insurance for damage they caused, you'll file a "third-party claim" with their company. Your insurer assigns you a unique claim number and a specific adjuster who will handle your case.

Step 4: The Adjuster Inspects Damage. An insurance adjuster—either meeting you in person or reviewing photos you upload—inspects your vehicle to assess damage and estimate repair costs. For straightforward claims, you might just upload pictures through a mobile app. The adjuster determines whether your car is economically repairable or qualifies as a total loss. If repairable, they'll approve repairs at your chosen shop (or require a network shop if your policy says so). If totaled, they'll calculate your car's pre-accident value and offer a settlement.

Step 5: Repairs Happen or Settlement Gets Paid. Once the adjuster greenlights repairs, your chosen shop completes the work and bills your insurer directly. You pay just your deductible amount. For total losses, your insurer issues a check for the vehicle's value minus your deductible. You can negotiate if you believe the valuation undervalues your car—gather comparable vehicle listings from your area to support a higher value.

Step 6: Closing Your Claim. Straightforward property-damage-only claims often close within one to two weeks. Injury claims drag on much longer—sometimes months—since medical treatment must finish before total costs become clear. Disputed claims or those involving lawsuits can stretch on for a year or longer.

One mistake people make constantly: delaying medical evaluation after accidents. Even if you feel fine, see a doctor within 24 hours. Some injuries like whiplash or concussions don't manifest immediately. Gaps in treatment give insurers ammunition to argue your injuries weren't serious or weren't caused by the accident.

Frequently Asked Questions About Car Insurance

Car insurance protects far more than sheet metal and glass—it safeguards your financial future, your legal standing, and your ability to sleep soundly at night knowing one mistake won't destroy everything you've built. The drivers who get the most value from their coverage are those who understand what they're actually buying, not those who simply hunt for the absolute cheapest premium they can find.

Start by honestly evaluating your financial situation and risk tolerance. Could you replace your car tomorrow if it was totaled tonight? Can you write a $1,000 check without financial stress? Do you own assets worth protecting from lawsuits? Your honest answers to these questions should drive your coverage decisions.

Resist the temptation to chase state minimums just to save money. Those minimums represent legal floors, not sensible recommendations. The $25 you save monthly on bare-bones coverage evaporates instantly if you cause a serious accident and face a lawsuit. Conversely, avoid overpaying for coverage that doesn't match your situation—if your 15-year-old vehicle is worth $1,800 and collision plus comprehensive costs $550 yearly, you're essentially betting against yourself at terrible odds.

Ask about every available discount: bundling multiple policies with one insurer, installing anti-theft devices, maintaining good grades if you're a student, completing defensive driving courses, paying your full premium upfront instead of monthly, or choosing paperless delivery. These discounts can slash your total costs by 20% or more without reducing your protection one bit.

Finally, actually read your policy documents. Yes, they're dense and filled with legal language, but knowing exactly what triggers coverage and what doesn't prevents devastating surprises when you need your insurance most. The worst possible time to discover you don't have rental reimbursement coverage is when you're standing at a collision repair shop being told your car needs three weeks of work.

Car insurance is one of those purchases you genuinely hope never to use beyond minor claims. But when you really need it—when stakes are high and costs are staggering—you'll be profoundly grateful you invested the time to get it right.