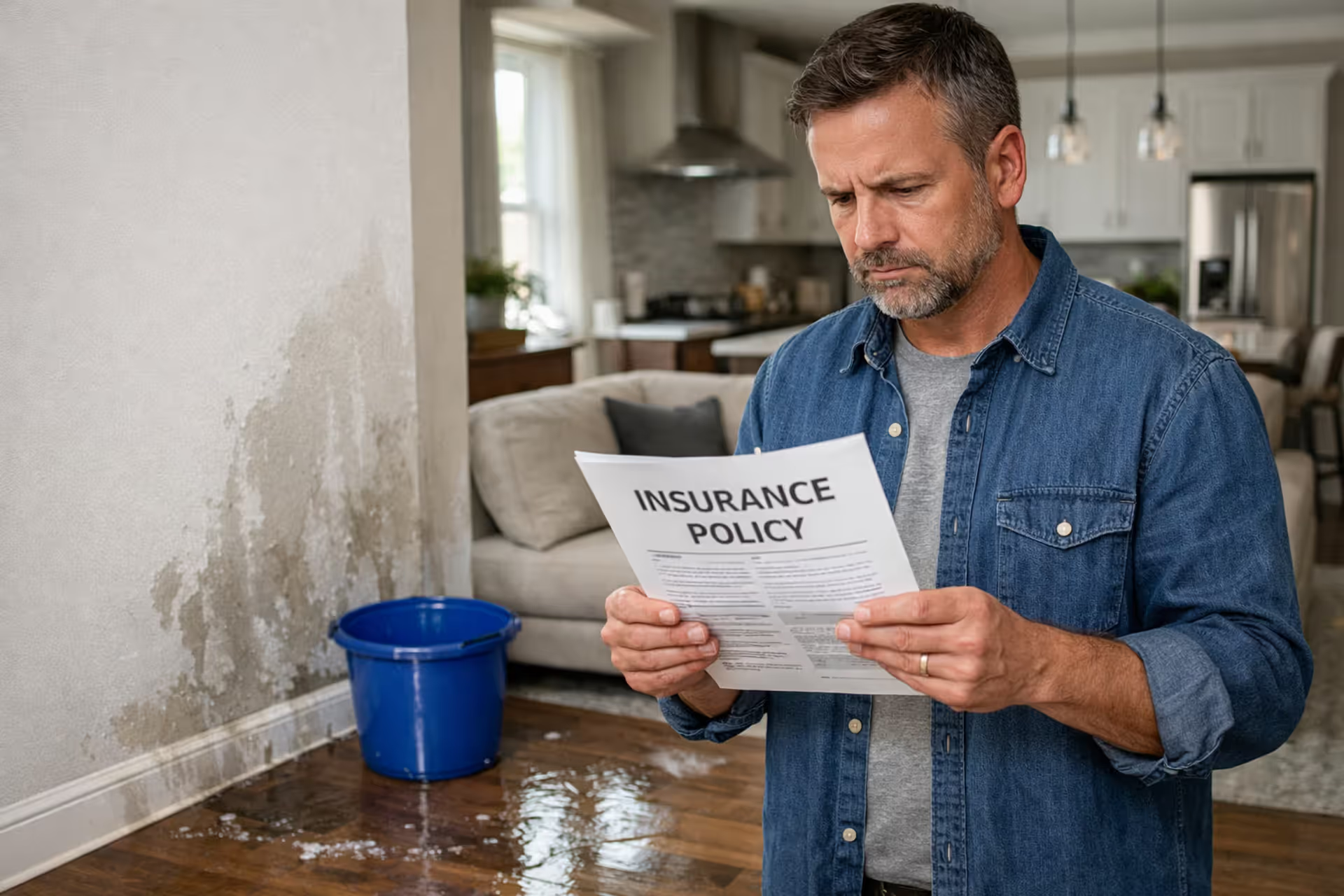

Homeowner reviewing an insurance policy in a damaged living room

How Does Home Insurance Work for Homeowners?

Content

Here's the reality: your policy is essentially a promise. The insurance company says they'll pay for certain disasters if you keep sending premium checks. But that promise comes with fine print, limits, and a whole claims process that catches people off guard when they're standing in two inches of water at 3 AM.

The way it actually functions involves you paying monthly or annual premiums. When something bad happens—and it's on the approved list of bad things—you file a claim. The insurer investigates, you pay your deductible, and they cut a check for the rest. Simple in theory. Complicated when you're living it.

What Home Insurance Covers and What It Doesn't

Your policy breaks down into four main buckets of protection. Each one handles different types of losses.

Dwelling coverage handles the physical structure—your house itself. This means the walls, roof, foundation, built-in appliances, and anything permanently attached. Let's say lightning strikes and starts a fire that guts your kitchen. This coverage pays contractors to rebuild it. Same goes for wind that rips off shingles or a vehicle that plows into your living room wall.

Personal property protection reimburses you for stuff inside the house. Your couch, TV, clothes in the closet, kitchen gadgets—basically anything you'd take with you if you moved. Here's where it gets interesting: insurers offer two payment methods. Actual cash value gives you what your five-year-old laptop is worth today (not much). Replacement cost pays for a new equivalent (way better, slightly pricier premiums).

Liability protection covers you when someone gets hurt on your property or you accidentally wreck someone else's stuff. Imagine a delivery driver slips on your icy steps, breaks an arm, and lawyers up. This section pays legal fees and any settlement. It also kicks in if your kid throws a baseball through a neighbor's window or your dog bites someone at the park.

Additional living expenses (sometimes called "loss of use") reimburses hotel costs, restaurant meals, and other extra expenses when you can't live at home during repairs. A major fire might displace you for six months. Your mortgage doesn't pause, but now you're also paying for temporary housing. This coverage handles that second set of living costs.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Standard policies typically respond to these problems: fire, lightning, windstorms, hail, explosions, theft, vandalism, objects falling on your house, ice and snow weight damage, and water escaping from burst pipes or appliances. Notice the specificity—it matters tremendously.

What's definitely not covered surprises homeowners constantly. Flood damage isn't included, period. You need separate flood coverage through NFIP or private carriers. Earthquakes require their own policy or endorsement. Your standard policy treats these like they don't exist.

Water damage gets tricky. A pipe bursts suddenly and floods your basement? Covered. Groundwater seeps through your foundation during heavy rain? Not covered. Your sewer backs up into the house? Not covered unless you added that specific endorsement. A pipe's been dripping behind the wall for months and now there's mold? Definitely not covered—that's maintenance you should've handled.

Also excluded: termites and pest damage, wear and tear, anything breaking because it's old, sinkholes (in most policies), and damage you cause intentionally. These gaps explain why people sometimes face $30,000 repair bills despite "having insurance."

Understanding Your Home Insurance Deductible

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Your deductible is the amount you pay before insurance contributes a single dollar. Think of it as your skin in the game.

Here's a real scenario: hail pummels your roof, causing $12,000 in damage. You've got a $2,000 deductible. The insurance company pays $10,000. You pay $2,000. That deductible amount never comes back to you—it's not like they write two checks and one goes to you. They simply subtract it from the total damage before calculating their payment.

Most folks land somewhere between $500 and $2,500 when picking their deductible. Here's the trade-off: agree to pay more out-of-pocket per claim, and your insurer drops your monthly premium. A $2,500 deductible might save you $300-$500 yearly compared to a $500 deductible. Over ten years with no claims, that's $3,000-$5,000 in your pocket. But when disaster strikes, you're paying $2,000 more upfront.

Now, the deductible math changes the entire claim equation. Say you've got a $1,000 deductible and discover $1,400 in hail damage. The insurance company would pay you $400—but filing that claim might raise your rates by $200 annually for the next three to five years. You'd actually lose money by filing. Smart homeowners often eat costs just above their deductible rather than trigger rate increases.

Coastal areas complicate things with percentage-based hurricane or wind deductibles. Instead of a flat dollar amount, you might face a 2% or 5% deductible calculated from your dwelling coverage. On a house insured for $400,000, that 2% deductible means you're paying the first $8,000 after a hurricane. That's dramatically different from your normal $1,000 deductible for other perils.

How Different Deductibles Affect Your Wallet

| Deductible Amount | Monthly Premium Impact | You Pay Per Claim | Makes Sense For |

| $500 | You'll pay the most monthly | Only $500 out-of-pocket | People with minimal emergency savings or who worry about affording repairs |

| $1,000 | Middle-ground monthly cost | $1,000 out-of-pocket | Most homeowners wanting balance between premium savings and manageable repair costs |

| $2,500 | You'll save considerably each month | $2,500 out-of-pocket | Those with solid emergency funds who want to minimize lifetime insurance costs |

| 2% of home value | Depends on your coverage amount | Could be $4,000-$10,000+ | Often mandatory for wind/hurricane damage in coastal zones |

Financial planners usually suggest this: pick the highest deductible you could handle tomorrow if you had to. That strategy cuts your lifetime premium costs substantially while keeping you protected against truly catastrophic losses.

Coverage Limits and How They Affect Your Policy

Every section of your policy has a maximum payout—the ceiling on what the insurer will spend. These caps determine whether you'll actually be made whole after major damage.

Dwelling limits should match what rebuilding your house would cost, not what you paid for it or what Zillow claims it's worth. Common mistake: people confuse market value with reconstruction cost. Your house might sell for $500,000 in a hot neighborhood, but perhaps it would only cost $320,000 to rebuild because land value doesn't need insurance. Flip side: in areas with expensive labor and materials, a $280,000 house might require $375,000 to rebuild.

Insurance companies offer a few approaches here. Basic replacement cost pays up to your dwelling limit to rebuild. Extended replacement cost gives you an extra 25%-50% cushion if construction costs have jumped. Guaranteed replacement cost (rare these days) promises to rebuild regardless of cost—but premiums run significantly higher.

Personal property limits usually equal 50%-70% of your dwelling coverage. So a policy with $300,000 in dwelling coverage might include $150,000-$210,000 for your belongings. This works fine for most people but creates problems if you've got expensive stuff in a modest home.

The real gotcha: sub-limits for specific categories. Your policy might say $150,000 in personal property coverage, but jewelry is capped at $1,500 total. Same for firearms ($2,500 typical limit), cash ($200), and securities. That $8,000 engagement ring stolen in a burglary? You're getting $1,500 unless you purchased a separate "floater" or scheduled personal property endorsement that lists the ring specifically with its appraised value.

This explains why your coverage needs regular updates. You renovate the kitchen for $40,000, add a primary suite for $60,000, finish the basement for $35,000—suddenly your rebuilding cost jumped $135,000. If you never told your insurer, your dwelling coverage might be $100,000+ too low.

Construction costs have spiked 30%-40% in many markets since 2020. A coverage limit that was perfect in 2023 could leave you badly short in 2025. Most insurers offer automatic annual inflation adjustments (usually 3%-5%), but that might not keep pace in high-growth areas.

Liability limits typically start at $100,000, which sounds like a lot until you imagine actual lawsuit scenarios. Someone suffers a serious injury on your property—broken back, permanent disability, lost income. Medical bills, pain and suffering, lost wages could easily hit $500,000 or more. Many insurance professionals push for $300,000-$500,000 in basic liability, plus an umbrella policy adding another $1-5 million for people with substantial assets.

How to File a Home Insurance Claim

This is where your policy transforms from paperwork into actual money. Each step matters if you want to avoid delays or disputes.

First move: grab your phone and document everything. Take dozens of photos and videos showing all damage from multiple angles before you touch anything. Create a detailed list of damaged items—write down what each thing was, roughly when you bought it, and approximately what it cost. This evidence proves your loss exists and prevents the "he said, she said" arguments that delay claims.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Second: prevent additional damage immediately. Your policy actually requires this—it's called "duty to mitigate." A window breaks during a storm? Cover it with plywood so rain doesn't pour in and destroy your floors. Pipe bursts? Shut off the water main. Roof gets punctured? Tarp it. Keep every receipt for these emergency repairs—insurers typically reimburse these costs. But don't hire contractors to fix everything permanently before the adjuster sees it.

Third: call your insurance company ASAP. Most policies demand "prompt" notification, which courts generally interpret as within a few days. Ring up your agent or the insurer's claims line to get the ball rolling. They'll assign you a claim number and explain what happens next.

Fourth: meet the insurance adjuster. The company dispatches someone to inspect damage firsthand, confirm coverage applies, and calculate repair costs. Be there during this inspection. Point out every bit of damage—it's harder to add things later. Hand over your documentation and receipts. The adjuster writes a report that essentially becomes your settlement offer.

Fifth: review their offer carefully. The adjuster's estimate determines your payout. If it seems low, you're not stuck. Request another inspection. Hire a contractor to provide a competing estimate. Or bring in a public adjuster (someone who works for you, not the insurance company) to negotiate on your behalf. Public adjusters typically take 10%-15% of your settlement but often boost payouts by 20%-60%, making them worth it for large claims.

Sixth: finish repairs and collect your money. For major claims, insurers usually send an initial check minus your deductible and any depreciation. Once you provide receipts proving repairs are complete, they release the depreciation holdback (on replacement cost policies). Big losses might involve multiple payments as work progresses.

Timeline? Small, straightforward claims might close in two to four weeks. Major structural damage involving multiple contractors can stretch three to twelve months. Catastrophic events affecting entire regions—hurricanes, wildfires—create adjuster shortages that push timelines to a year or more.

One more thing: stay on top of communication. Return adjuster calls same-day. Submit requested documents within 48 hours. Follow up weekly if things seem stalled. And write down every conversation—date, time, person's name, what they said. This paper trail becomes critical if disputes arise.

How Home Insurance Premiums Are Calculated

Insurance companies feed dozens of variables into pricing algorithms. Several factors dominate the equation.

Location drives massive price differences. A house in coastal Florida or Louisiana faces hurricane risk that pushes premiums to $3,000-$6,000 annually. That same house transplanted to Ohio might cost $800-$1,200 yearly. High-crime neighborhoods increase theft risk, raising premiums. Distance to fire stations matters—homes farther from hydrants and fire departments pay more because fires cause worse damage. Wildfire zones in California, Colorado, and other Western states now face brutal premiums or outright coverage denials.

Author: Trevor Whitfield;

Source: talero.spotpariz.net

Your home's characteristics play a huge role. Age is big—older houses have aging electrical systems, old plumbing, outdated HVAC that increase fire and water damage risk. Construction type matters: wood frame costs more to insure than brick or concrete block. Your roof's age and condition directly affect rates. A roof that's 25 years old and nearing replacement might add 20%-30% to premiums versus a new roof with 30 years of life ahead. Square footage obviously impacts costs—bigger houses cost more to rebuild.

Coverage choices and deductibles affect premiums in predictable ways. More dwelling coverage equals higher premiums. Lower deductibles mean higher premiums. Every endorsement you add increases the bill. But the relationship isn't linear—doubling coverage might only boost premiums by 40%-60%.

Your claims history follows you everywhere. Insurers check the CLUE (Comprehensive Loss Underwriting Exchange) database, which tracks claims for five to seven years. File two claims in three years and expect rate hikes of 20%-40%. Three or more claims often trigger non-renewal—the insurer drops you, forcing you to find coverage elsewhere at even higher rates. Even claims from the previous homeowner can haunt you for the first few years you own the place.

Credit-based insurance scores heavily influence pricing in most states. Insurers discovered statistical correlations between credit behavior and claim frequency. Homeowners with excellent credit might pay 30%-50% less than someone with poor credit for identical coverage on the same house. Several states have restricted this practice, but it's still widespread.

Protective features can slash premiums. Monitored security systems, smoke detectors wired to monitoring services, fire extinguishers, storm shutters, and impact-resistant roofing qualify for discounts ranging from 5%-20%. Newer homes often get breaks. Some insurers discount for extended claims-free periods. Bundling home and auto policies with the same company typically saves 15%-25%. Even professional affiliations sometimes qualify for group discounts.

Common Mistakes Homeowners Make With Insurance

Even careful people make errors that cost them money or leave them exposed.

Underinsuring the dwelling causes more financial disasters than almost anything else. People insure for the purchase price paid five years ago, or for the remaining mortgage balance, or for the property's market value—all wrong numbers. Then major damage strikes and they discover their actual rebuilding cost exceeds coverage by $75,000 or $120,000. Guess who pays that gap? Not the insurance company.

Forgetting to update policies after life changes creates coverage holes everywhere. You spend $50,000 finishing the basement into a media room—did you tell your insurer so they'd increase dwelling coverage? You bought a $4,000 laptop and $2,500 camera for your side business—does your policy cover business equipment at home (usually no)? You installed a pool—did you boost liability coverage to address that drowning risk? Most people answer no to all of these.

Not documenting possessions makes claims nightmarish. When fire destroys everything you own, can you list it all from memory? Walk through your house with your phone right now, narrating and filming everything in every room, every closet, every drawer. Open boxes, show labels, describe items. Do this annually. Store the video in cloud storage or email it to yourself. When disaster strikes, this becomes your proof of what you owned.

Ignoring available discounts means overpaying for years. Many homeowners don't realize they qualify for bundling discounts, claims-free discounts, retiree discounts, professional association discounts, or security system discounts. Simply asking your agent "what discounts am I missing?" can cut premiums by 15%-30%.

Never shopping around leaves money on the table. Insurance rates vary wildly between companies for identical coverage on the same house. One insurer quotes $2,100 annually while another charges $1,450 for the exact same protection. Compare quotes from at least three companies every two to three years, especially after major life events like marriage, retirement, or paying off your mortgage.

Picking the wrong deductible causes problems both directions. Some people stick with $500 deductibles they don't need, paying $300-$400 extra yearly in premiums for decades. Others choose $5,000 deductibles they can't actually afford, then panic when they need to file a claim and don't have the cash.

Filing small claims destroys rate longevity. That $2,500 water damage claim might get paid, but then your rates jump $300 annually for five years. You'll pay $1,500 extra in future premiums for a $2,500 claim payout. Most experts suggest eating any loss within $5,000-$10,000 of your deductible rather than filing claims that trigger rate increases.

Expert Perspective

I've handled claims for 18 years, and the pattern never changes.Homeowners treat their policy like a subscription service—sign up and forget it exists until disaster strikes. Then they're shocked their coverage hasn't kept pace with construction costs that jumped 35% since they bought the policy. Or they added $80,000 in renovations without updating coverage. I saw a family last month whose house was insured for $280,000 but rebuilding it after a fire will cost $395,000. That $115,000 gap comes from their savings. Schedule an annual review with your agent. Update coverage immediately after any home improvements. Actually read your exclusions section before you need to file a claim. These three habits prevent 80% of the problems I see

— Jennifer Martinez

Frequently Asked Questions About Home Insurance

Home insurance operates through a financial contract where you pay regular premiums and the insurance company promises to cover specified disasters up to predetermined limits. The system delivers protection through dwelling coverage that rebuilds your house, personal property reimbursement for belongings, liability defense when lawsuits arise, and temporary living expense coverage during displacement.

Deductibles determine your share of each loss before insurance contributes. Coverage limits cap maximum payouts and require careful calibration matching your actual rebuilding costs and possession values. The claim process converts policy language into actual payments through documentation, adjuster inspections, repair completion, and final settlement.

Your premiums reflect dozens of variables—location risk, home age and construction, coverage amounts selected, claim history, credit scores, and protective features. Common errors plague homeowners constantly: underinsuring dwelling coverage, forgetting to update policies after renovations, skipping possession documentation, missing obvious discounts, and filing small claims that trigger long-term rate increases.

Making this system work for you requires active management, not passive premium payments. Review coverage annually with your agent. Document your possessions thoroughly. Maintain your home to prevent excluded damage. Choose deductibles matching your emergency savings. File claims strategically, recognizing small losses might cost more in future premiums than paying out-of-pocket. Your home insurance functions effectively only when you understand its mechanics and manage it as a critical piece of your financial protection strategy.