Person reviewing health insurance options and medical bills at home

Is It Illegal to Not Have Health Insurance in the U.S

Content

Here's something that trips up millions of Americans: they remember hearing about mandatory health insurance years ago, but aren't sure if that's still a thing. Maybe you've skipped coverage for a few months (or years) and you're worried the government might come after you. Or perhaps you just lost your job and wonder if going uninsured means breaking the law.

he short answer? It's complicated—and it depends on your zip code.

Let me walk you through what's actually happening with health insurance requirements in 2026, because the rules have changed more times than most people realize.

Understanding the Health Insurance Mandate

Back in 2010, the Affordable Care Act flipped the script on American healthcare. For the first time in U.S. history, federal law required almost every citizen and legal resident to carry health insurance. This wasn't just a suggestion—the IRS would literally bill you during tax season if you went without coverage.

Why did lawmakers do this? Insurance only works when healthy people subsidize sick people. When only sick folks buy coverage, premiums skyrocket and the whole system collapses. So the mandate forced young, healthy people (who rarely need doctors) to buy policies, spreading costs across a larger pool.

From 2014 through 2018, uninsured Americans faced real financial consequences. The IRS calculated penalties using a two-part formula: either charge a per-person flat amount ($695 per adult by 2018) or take 2.5% of your household income above the tax filing threshold. Whichever number was bigger—that's what you owed. Some families paid over $2,000 annually just for being uninsured.

Then came 2017's Tax Cuts and Jobs Act. Republican lawmakers couldn't muster enough votes to kill the mandate outright, so they tried something clever: they kept the requirement on the books but reduced the penalty to exactly zero dollars. Once that took effect in January 2019, the federal mandate became toothless.

What counts as "real" insurance hasn't changed, though. Minimum essential coverage includes the usual suspects: your employer's group plan, a policy from Healthcare.gov or a state marketplace, Medicare Parts A and B, Medicaid and CHIP, TRICARE for military families, and VA health benefits. Recognizing these plan types matters mostly if you live in one of the handful of states that created their own mandates after the federal one died.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Federal Penalties for Not Having Health Insurance

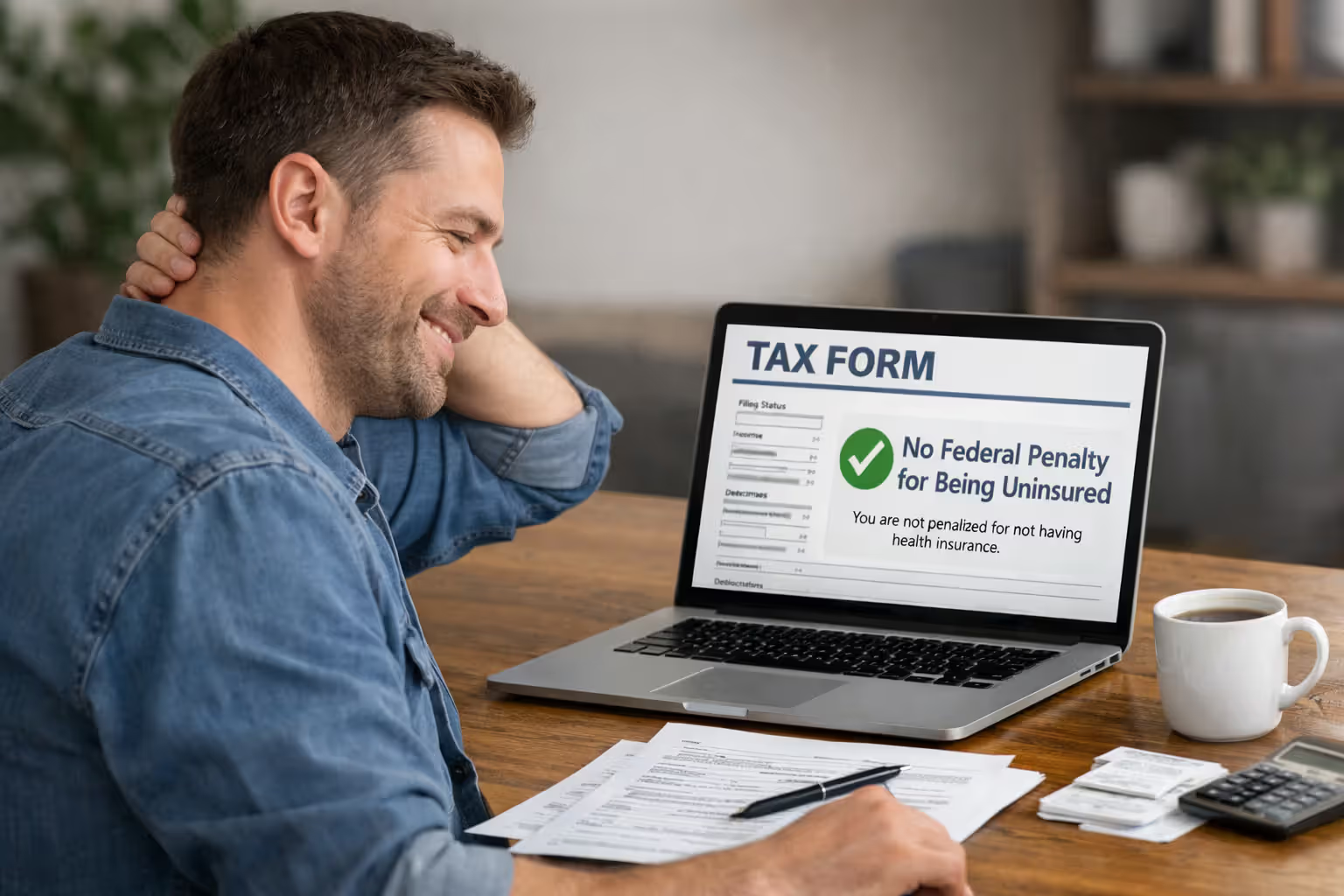

Let's clear this up once and for all: as of 2026, the federal government doesn't care whether you have health insurance. Zero enforcement. No penalties. Nada.

The IRS stopped asking about your coverage status on Form 1040 years ago. They won't send collection letters, withhold your refund, or report you to credit bureaus for being uninsured. That entire enforcement apparatus was dismantled.

This is a complete 180 from the 2014-2018 era when the IRS actively collected these penalties. During those years, they treated unpaid mandate penalties like any other tax debt—adding interest, sending increasingly stern notices, eventually intercepting tax refunds. That system no longer exists.

Here's where it gets weird: Congress never actually repealed the mandate language from the tax code. It's still there in the law books. They just changed the penalty from "a substantial amount" to "zero dollars." Legally, you're still "required" to have insurance—but there's no consequence for ignoring that requirement. It's like a speed limit with no fine and no cops. Technically still a rule, but functionally meaningless.

Some people still panic about federal penalties because their brother-in-law's cousin swears he got fined last year, or they read an old blog post from 2016. Don't let outdated information stress you out. The federal penalty is dead and gone.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

State-Level Health Insurance Requirements

While Washington stepped back, several states decided they'd rather not watch their insurance markets implode. Without a mandate forcing healthy people to buy coverage, insurers worried (reasonably) that only sick, expensive patients would keep their policies. That scenario leads to premium death spirals.

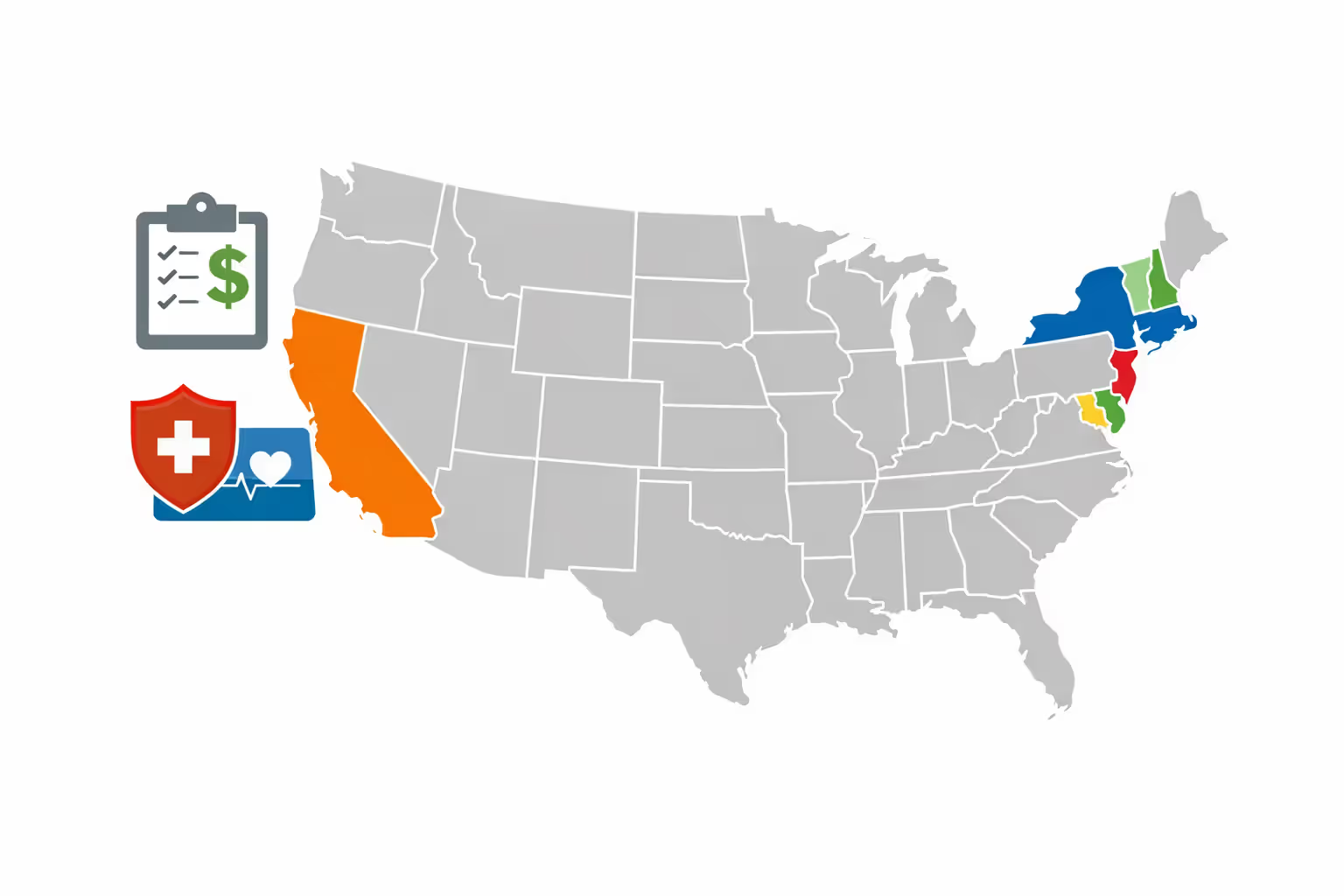

So six places decided to roll their own mandates: California, Massachusetts, New Jersey, Rhode Island, Vermont, and Washington D.C. Each one operates independently with unique penalty calculations, exemption rules, and enforcement tactics.

States with Active Penalties

California kicked off its state mandate in January 2020, right as the federal penalty disappeared. The California Franchise Tax Board doesn't mess around—they will absolutely collect penalties through your state return, and they have the authority to garnish wages or place liens if you ignore the bill.

Massachusetts is actually the OG of insurance mandates. They launched theirs way back in 2006, years before the ACA existed. The federal mandate was literally modeled on what Massachusetts did. This state has the longest track record of enforcement, and they've refined their system to catch nearly everyone who owes.

New Jersey jumped in fast, implementing their mandate in 2019 to coincide with the federal penalty's elimination. State lawmakers didn't want a coverage gap that might destabilize their marketplace. The penalty structure closely mirrors what the federal government used to charge.

Rhode Island followed in 2020. As one of the smallest states, Rhode Island's insurance market is particularly vulnerable when healthy people drop out. Even a few thousand uninsured residents can push premiums up noticeably, so state officials felt the mandate was necessary.

Vermont also started penalizing uninsured residents in 2020, though their approach differs significantly. Vermont's penalties run lower than most other states—critics argue they're too small to actually change behavior, while supporters counter that Vermont's progressive politics make aggressive enforcement unpopular.

District of Columbia rounds out the list with a 2019 start date. DC residents face penalties comparable to California and New Jersey, and the district's tax office has proven willing to collect aggressively from those who don't pay voluntarily.

How State Penalties Are Calculated

Most states borrowed the federal formula but adjusted it for local conditions. They typically look at your income and household size, then charge the greater of two amounts: a flat per-person fee or a percentage of income above the filing threshold.

| State | How They Calculate Your Penalty | Minimum You'll Pay (2026) | Maximum Cap (2026) |

| California | $850 for each adult and $425 per kid, OR 2.5% of income above filing requirements—whichever hurts more | $850 | No maximum—sky's the limit at 2.5% |

| Massachusetts | Up to half the annual premium of the cheapest ConnectorCare plan you qualify for based on income | Changes based on your income bracket | Around $3,000 per adult |

| New Jersey | $695 per grownup and $347.50 per child, OR 2.5% of income over the threshold | $695 | Uncapped at 2.5% of income |

| Rhode Island | $695 for adults and $347.50 for kids, OR 2.5% of household income beyond filing minimum | $695 | No ceiling—depends on income |

| Vermont | Equals the average premium tax credit amount for similar households in the state | Varies significantly | Approximately $3,500 per household |

| District of Columbia | $695 per adult/$347.50 per child, OR 2.5% of income above threshold | $695 | Unlimited at 2.5% |

These penalties hit when you file your state taxes. The state's revenue department calculates what you owe based on how many months you went bare. And unlike federal tax debt that people sometimes ignore for years, state tax obligations are harder to dodge—states have powerful collection tools and aren't shy about using them.

Here's a trap people fall into: they assume having insurance for part of the year gets them off the hook. Wrong. States prorate penalties by the month. Most give you a free pass for short gaps under three consecutive months, but if you're uninsured for four months or more, you'll pay for every month beyond that three-month grace period.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

What Happens If You Go Without Coverage

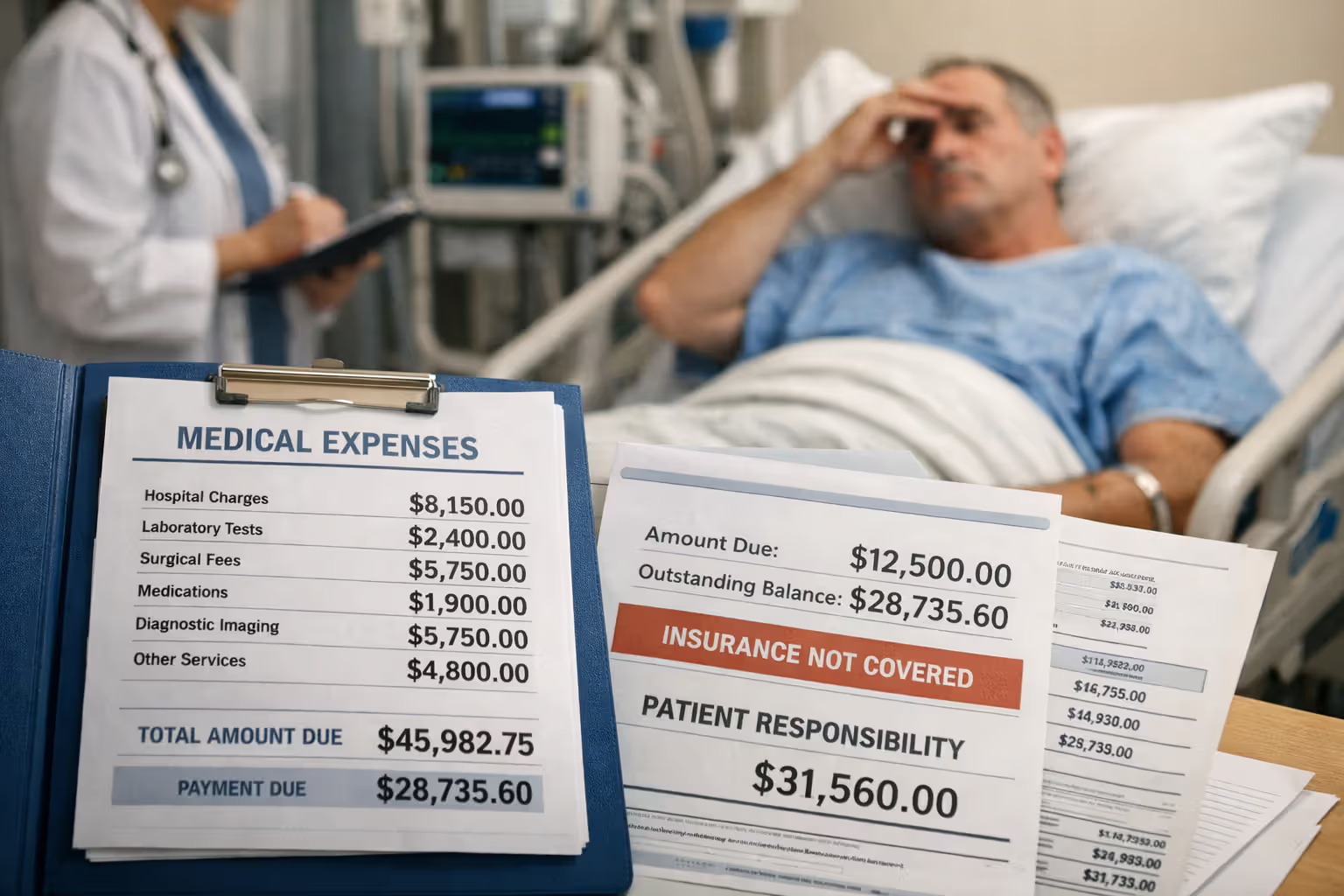

Forget penalties for a minute. The real danger of going uninsured isn't a government fine—it's the financial and medical trainwreck that happens when you actually need care.

Medical debt destroys American families more than any other type of financial problem. Break your leg skiing? That ER visit, X-rays, orthopedist consult, and cast will run $7,000-$12,000. Get pneumonia bad enough to need hospitalization? Figure $40,000-$60,000 for a three-day stay. Diagnosed with cancer? A year of treatment can easily exceed $200,000. Without coverage, every penny comes from your bank account.

Here's what really stings: hospitals charge uninsured patients substantially more than they bill insurance companies. When Blue Cross sends a patient, the hospital might accept $3,000 for a procedure they list at $8,000. That negotiated discount is baked into every insurance contract. But when you show up uninsured? You're billed the full $8,000 "rack rate." You lose 40-60% in negotiating power just by being uninsured.

Access to care dries up too. Try calling a specialist—dermatologist, cardiologist, neurologist—and tell the receptionist you're paying cash without insurance. Half will refuse to book you as a new patient. Primary care doctors increasingly require upfront payment from uninsured patients before they'll see you. Preventive care like mammograms, colonoscopies, and routine bloodwork become expensive enough that people skip them, leading to late-stage diagnoses.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

The concept of coverage limits flips upside down when you're uninsured. With a policy, you face annual out-of-pocket maximums—maybe $9,000 for individuals or $18,000 for families. Hit that cap and insurance pays 100% of everything else. Without coverage, there's no maximum. You're exposed to unlimited financial liability. A serious car accident with multiple surgeries, weeks in ICU, and months of rehab? You could face $500,000 in bills with no cap protecting you.

The claim process becomes irrelevant because there's nobody to file a claim with. Instead you negotiate directly with hospitals, often while you're sick or recovering from surgery. Some facilities offer charity care programs or payment plans, but qualifying is difficult—they want extensive financial documentation, and approval can take months while your bill heads to collections.

Most people dramatically underestimate how fast medical costs can destroy their finances. We regularly counsel families who lost homes, emptied 401(k)s, or filed bankruptcy over medical bills that insurance would have covered for a $5,000 deductible. The monthly premium looks expensive until you're staring at six figures of hospital bills

— Jennifer Martinez

Exemptions and Special Circumstances

Even in states running their own mandates, plenty of people don't have to carry coverage. Exemptions exist for financial hardship and special situations.

Income-based exemptions are the most common escape hatch. If buying the cheapest bronze plan available through your state's marketplace would eat up more than 8-10% of household income (the exact percentage varies by state), you qualify for an affordability exemption. States calculate this using the lowest-cost plan you're eligible for, not the average plan price.

Short gaps get automatic forgiveness. Miss coverage for under three consecutive months and most states let it slide without penalty. This helps people transitioning between jobs who need a few weeks to get new coverage started. But stretch that gap to four months and penalties kick in.

Religious exemptions apply if you belong to a recognized religious sect with established opposition to insurance. These aren't casual "I personally object" claims—the religious group must have formal doctrines rejecting insurance benefits, and you must be an actual member in good standing. It's a narrow exemption with strict requirements.

Hardship exemptions cast a wider net: homelessness, facing eviction or foreclosure, surviving domestic violence, death of a close family member, natural disaster damage to your property, filing bankruptcy, carrying substantial medical debt from before the coverage year, and various other circumstances that reasonably prevented you from getting insured. Each state runs its own hardship exemption application, and you'll need documentation backing up your claim.

Incarcerated individuals are automatically exempt for months spent in jail or prison. Members of federally recognized Indian tribes and those eligible for Indian Health Service programs also get exemptions.

One critical point: qualifying for a penalty exemption doesn't give you health coverage. You still lack insurance and face all the medical and financial risks of being uninsured. You just won't pay a tax penalty on top of those problems.

How to Get Covered If You're Uninsured

Currently uninsured and ready to fix that? Several pathways exist depending on your situation and the calendar.

Open Enrollment happens once yearly, running from early November through mid-January for coverage starting the following January 1st. During this roughly ten-week window, anyone can buy individual marketplace insurance through Healthcare.gov or their state's exchange without proving they have a qualifying reason. Miss this window and you're stuck waiting until next year unless you experience a qualifying life event.

Special Enrollment Periods open when life changes occur: losing existing coverage (including aging off a parent's plan at 26), getting married or divorced, having a baby or adopting a child, moving to a new ZIP code that offers different plan options, or becoming a U.S. citizen. Most qualifying events give you 60 days to enroll, but you'll need documents proving the event occurred—marriage certificate, birth certificate, lease agreement, etc.

Medicaid operates year-round with no enrollment deadlines. If your income falls below your state's cutoff (usually 138% of federal poverty level in the 39 states plus DC that expanded Medicaid), you can apply any month and get coverage starting immediately—often the first day of the month you applied. Medicaid doesn't care about Open Enrollment windows.

Employer coverage is how most working-age Americans get insured. If your company offers health benefits, you can usually enroll when first hired or during the company's yearly enrollment period. Some employers cover 100% of employee premiums, though most require workers to chip in something.

CHIP serves kids in families earning too much for Medicaid but not enough to comfortably afford private coverage. States set their own income limits, but most extend CHIP to families making 200-300% of poverty level. Your kids might qualify even if you don't.

Short-term plans are available outside enrollment periods, but buyer beware: these don't count as real coverage under state mandates. They also exclude pre-existing conditions, cap benefits, and routinely deny claims that regular plans would cover. They're essentially catastrophic accident insurance, not real health coverage.

Deductibles range wildly—from $0 on many Medicaid plans to over $9,000 on high-deductible bronze marketplace plans. This is the amount you'll pay out-of-pocket each year before your insurance starts covering most services at the higher benefit levels. Lower monthly premiums usually mean higher deductibles, forcing you to choose between affordable monthly costs and protection against big expenses.

Premium tax credits slash monthly marketplace premiums for individuals and families earning 100-400% of poverty level. Many people qualify for subsidies that drop their monthly payment to $50 or less. Additional cost-sharing reductions (available to those earning up to 250% of poverty) reduce your deductible and copays, making care more affordable when you actually need it.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Frequently Asked Questions About Health Insurance Requirements

Whether you legally need health insurance comes down to geography. The federal government stopped enforcing its mandate years ago, but six states (California, Massachusetts, New Jersey, Rhode Island, Vermont, and D.C.) run their own with real penalties for noncompliance.

But here's what matters more than legal requirements: going uninsured is financially dangerous regardless of where you live. Medical costs keep climbing, and a single hospitalization can generate debt that follows you for decades. Legal penalties—whether state fines or medical bills—hurt far less than the security that comes from having coverage.

Currently uninsured? Check if you qualify for Medicaid immediately—many people qualify without realizing it. Otherwise, mark your calendar for the next Open Enrollment Period starting in November. Most people are surprised to find that subsidized marketplace coverage costs less than they expected.

Understanding your state's specific rules and knowing what coverage options exist puts you in control of both your health and financial security. Don't wait for a medical emergency to force your hand—millions of Americans learn that lesson the expensive way. Take action now to get appropriate coverage in place for yourself and your family.