Young adult comparing catastrophic health insurance options on a laptop at home

What Is Catastrophic Health Insurance?

Content

Catastrophic health insurance sits at the opposite end of the spectrum from comprehensive coverage. It's designed for people who rarely visit the doctor and want protection against worst-case medical scenarios—a serious accident, unexpected diagnosis, or emergency surgery that could otherwise lead to financial ruin. These plans carry rock-bottom monthly premiums but require you to pay thousands out of pocket before coverage kicks in for most services.

If you're young, healthy, and willing to shoulder significant upfront costs in exchange for minimal monthly payments, catastrophic coverage might fit your situation. But the eligibility rules are strict, and the trade-offs can backfire if you misjudge your healthcare needs or don't qualify for better options with subsidies.

Catastrophic Health Insurance Definition and Basics

Catastrophic health insurance is a tier of Affordable Care Act (ACA) marketplace coverage characterized by very high deductibles and low monthly premiums. These plans must cover the same ten essential health benefits as other marketplace plans—emergency services, hospitalization, maternity care, mental health services, prescription drugs, and more—but only after you've met an annual deductible that typically exceeds $9,000 for an individual in 2026.

The primary purpose is financial protection against major medical events. Think of it as a safety net that prevents a single hospital stay from wiping out your savings or forcing bankruptcy. Catastrophic plans are not designed for routine care management. If you need regular prescriptions, specialist visits, or ongoing treatment for a chronic condition, you'll pay full price until that steep deductible is satisfied.

All marketplace catastrophic plans must cover certain preventive services at no cost, even before you meet your deductible. Annual check-ups, immunizations, cancer screenings, and contraceptive counseling fall into this category. Beyond that, you're responsible for negotiated rates (not full retail prices) for doctor visits, urgent care, imaging, lab work, and prescriptions until your deductible is met.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Major insurers like Blue Cross Blue Shield, Cigna, and Oscar Health offer catastrophic plans in most marketplace regions. Availability varies by state and county, and not every carrier participates in every area. You can only enroll during the annual Open Enrollment Period or a Special Enrollment Period triggered by a qualifying life event—losing other coverage, moving, marriage, or birth of a child.

Who Qualifies for Catastrophic Health Insurance

Catastrophic plans come with strict eligibility gates. You must be under age 30 for the entire coverage year, or you must qualify for a hardship or affordability exemption regardless of age.

The under-30 rule is straightforward: if you turn 30 on December 31, 2026, you're eligible for a catastrophic plan for that year. Once you reach 30, you lose automatic access unless you secure an exemption.

Hardship exemptions cover a range of difficult circumstances: homelessness, eviction in the past six months, domestic violence, death of a close family member, natural disaster damage, bankruptcy in the past six months, medical debt resulting in substantial unpaid bills, or caring for a family member who is disabled or ill. You apply through the marketplace or directly with the Department of Health and Human Services, providing documentation of your situation.

Affordability exemptions apply when the lowest-cost Bronze plan available to you (after employer contributions, if applicable) would cost more than 8.39% of your household income in 2026. If you qualify for this exemption, you can choose a catastrophic plan instead. However, this is a narrow window: if you're eligible for premium tax credits based on income, those credits cannot be applied to catastrophic plans. You'd likely pay less overall by selecting a Bronze or Silver plan with subsidies.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

You must enroll through the federal or state marketplace. Catastrophic plans are not available off-exchange or directly from insurers outside the ACA system.

What Does Catastrophic Health Insurance Cover

Catastrophic plans cover all ten essential health benefits mandated by the ACA: ambulatory patient services, emergency services, hospitalization, maternity and newborn care, mental health and substance use disorder services, prescription drugs, rehabilitative services and devices, laboratory services, preventive and wellness services, and pediatric services including dental and vision.

The catch is timing. Before you meet your deductible, you pay the full negotiated rate for most of these services. If an urgent care visit costs $150 under your plan's contracted rate, you pay $150. An MRI might run $800; you pay $800. A generic prescription could be $25; you pay $25. Every dollar you spend counts toward your deductible.

Preventive care is the major exception. Annual physicals, blood pressure screenings, cholesterol tests, diabetes screenings, colorectal cancer screenings, mammograms, Pap tests, flu shots, HPV vaccines, and well-child visits are covered at 100% with no cost-sharing. These services are free even if you haven't touched your deductible. Contraceptive methods and counseling are also fully covered for women.

Once you hit your deductible—often $9,200 or more for individual coverage in 2026—the plan begins paying for covered services. At that point, you typically pay coinsurance (a percentage of costs) or copays until you reach your out-of-pocket maximum, which is capped at the federal limit of $9,200 for individuals in 2026. For catastrophic plans, the deductible and out-of-pocket max are often identical or very close, meaning once you meet the deductible, you pay little to nothing for additional care that year.

Catastrophic plans do not cover services deemed non-essential: cosmetic procedures, elective surgeries, alternative medicine, acupuncture (unless required by state mandate), long-term care, or private-duty nursing. Dental and vision coverage for adults is also excluded, though pediatric dental and vision are included as essential benefits.

Understanding Catastrophic Health Insurance Deductibles and Costs

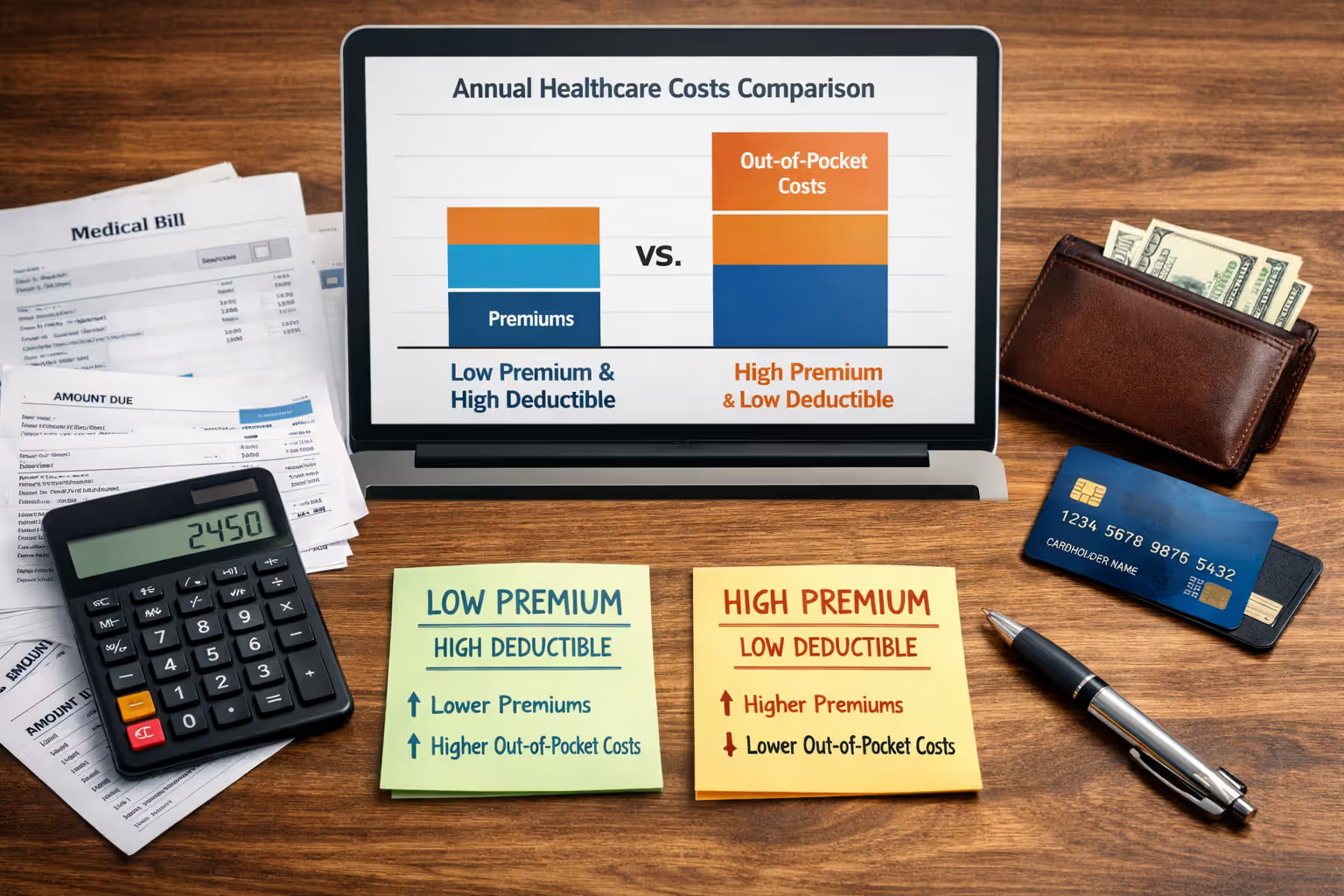

Deductibles for catastrophic plans in 2026 typically range from $9,200 to $9,450 for individual coverage, mirroring the federal out-of-pocket maximum. Family deductibles can reach $18,400 or higher. These figures are significantly higher than other metal tiers: Bronze plans average $6,000 to $7,500 deductibles, Silver plans $3,000 to $5,000, and Gold plans $1,000 to $2,500.

Monthly premiums are the upside. Catastrophic plan premiums often run $150 to $250 per month for a 25-year-old in a mid-cost area, compared to $300 to $400 for Bronze and $400 to $550 for Silver. Over a year, that's $1,800 to $3,000 in premium savings. But if you need $5,000 worth of care, you'll pay every dollar of it under a catastrophic plan, whereas a Silver plan with a $4,000 deductible and subsidies might cost you less overall.

Out-of-pocket maximums cap your annual spending on covered services. For catastrophic plans, this limit is set at the federal maximum: $9,200 for individuals and $18,400 for families in 2026. Once you hit this ceiling, the plan pays 100% of covered expenses for the rest of the year. Premiums don't count toward this limit, nor do out-of-network services or non-covered care.

How Deductibles Work in Catastrophic Plans

Every dollar you spend on covered services (except preventive care) counts toward your deductible. If you visit an in-network primary care doctor and the negotiated rate is $120, you pay $120, and that amount applies to your deductible. If you fill a prescription with a negotiated cost of $40, you pay $40, and it counts. Emergency room visits, specialist consultations, physical therapy, imaging—all of it accumulates until you reach the deductible threshold.

Once the deductible is met, most catastrophic plans switch to minimal cost-sharing. Some plans cover subsequent services at 100%, while others require small copays or coinsurance until you hit the out-of-pocket max. Because the deductible and out-of-pocket max are often the same figure, many enrollees pay full negotiated rates up to $9,200, then everything is free.

One common mistake: assuming the deductible resets mid-year. It doesn't. Deductibles reset on January 1, so if you meet your deductible in November, you get only two months of full coverage before starting over.

Premium vs. Deductible Trade-offs

The fundamental trade-off is clear: pay less each month, pay more when you need care. For someone who uses healthcare infrequently—maybe one or two doctor visits a year, no prescriptions, no chronic conditions—a catastrophic plan can save money. Annual costs might total $2,400 in premiums plus $300 in out-of-pocket expenses for preventive and minor care, totaling $2,700.

Compare that to a Silver plan with $450 monthly premiums ($5,400 annually) and a $4,000 deductible. If you use $300 in care, your total is $5,700—more than double the catastrophic plan cost. But if you need $8,000 in care, the catastrophic plan costs $9,200 in deductible plus $2,400 in premiums ($11,600 total), while the Silver plan costs $5,400 in premiums plus $4,000 deductible ($9,400 total).

The break-even point varies by individual premiums, deductibles, and expected utilization. A rule of thumb: if you're confident you'll spend less than $3,000 on healthcare in a year, catastrophic plans often win. If you anticipate $5,000 or more, higher-tier plans with subsidies usually cost less overall.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Subsidies tilt the math heavily. Premium tax credits can reduce Silver plan premiums to $50 or even $0 per month for lower-income enrollees. Cost-sharing reductions lower deductibles and copays on Silver plans for those earning up to 250% of the federal poverty level. Catastrophic plans are ineligible for both, so even if you qualify for an affordability exemption, you forfeit thousands in potential assistance.

How the Catastrophic Health Insurance Claim Process Works

Filing a claim under a catastrophic plan follows the same process as other marketplace plans. Most of the time, you won't file claims yourself—providers submit them directly to your insurer. Here's the typical sequence:

- Receive care from an in-network provider. Present your insurance card. The provider verifies coverage and eligibility electronically.

- Provider submits a claim to your insurer. This includes procedure codes, diagnosis codes, and negotiated rates. Submission usually happens within a few days of your visit.

- Insurer processes the claim. They confirm the service is covered, apply the negotiated rate, and determine your responsibility. Since you likely haven't met your deductible, you're responsible for the full negotiated amount.

- You receive an Explanation of Benefits (EOB). This document (mailed or available online) details what was billed, what the insurer negotiated, what you owe, and how much counts toward your deductible. It's not a bill—it's a summary.

- Provider bills you. You receive a separate bill for the amount shown on the EOB. Payment is due to the provider, not the insurer.

- After meeting your deductible, the insurer pays claims. Once your accumulated expenses hit the deductible, the insurer begins covering services. You may still owe coinsurance or copays until you reach the out-of-pocket max.

Reimbursement timelines vary. If you pay upfront (common for prescriptions or urgent care), you may need to submit a claim manually. Download a claim form from your insurer's website, attach itemized receipts, and mail or upload it. Reimbursement typically takes 30 to 45 days.

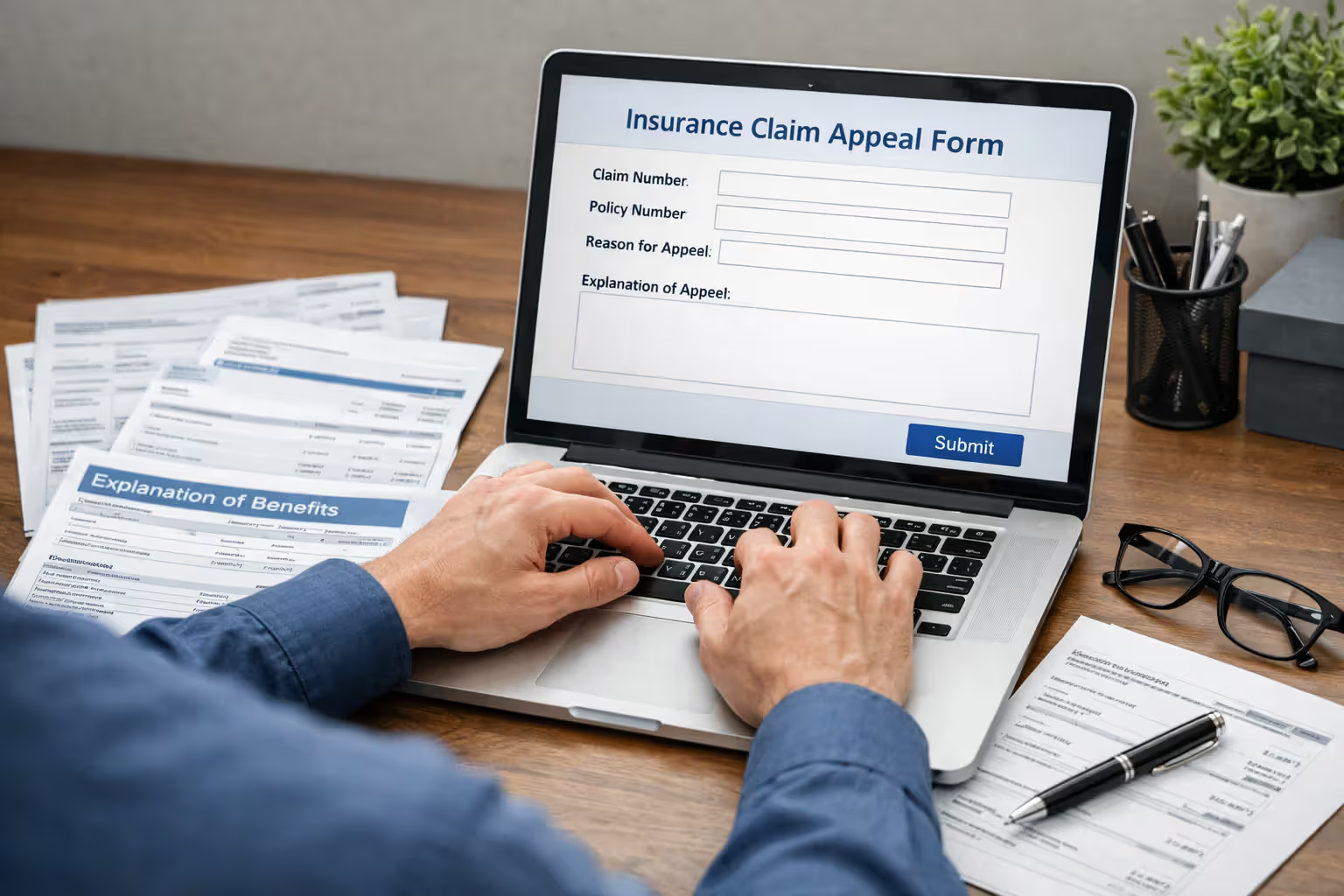

If a claim is denied—perhaps the insurer argues a service isn't covered or wasn't medically necessary—you have the right to appeal. Start with an internal appeal through your insurer, providing documentation from your provider. If that fails, you can request an external review by an independent third party. The ACA guarantees this right, and external reviewers often overturn insurer denials.

Author: Alyssa Coleman;

Source: talero.spotpariz.net

Catastrophic Health Insurance vs. Other Plan Types

Understanding how catastrophic plans stack up against Bronze and Silver options clarifies when they make sense.

| Plan Type | Monthly Premium | Deductible | Out-of-Pocket Max | Best For |

| Catastrophic | $150–$250 | $9,200 | $9,200 | Healthy individuals under 30, minimal care needs, no subsidy eligibility |

| Bronze | $300–$400 | $6,500 | $9,200 | Low to moderate care needs, some subsidy eligibility, prefer lower premiums |

| Silver | $400–$550 | $4,000 | $8,500 | Moderate care needs, subsidy-eligible, want cost-sharing reductions |

Catastrophic plans offer the lowest premiums but the highest deductibles. Bronze plans provide a middle ground: slightly higher premiums, moderately high deductibles, and eligibility for premium tax credits. Silver plans cost more monthly but offer lower deductibles and qualify for both premium credits and cost-sharing reductions if your income is below 250% of the federal poverty level.

When catastrophic makes sense: You're under 30, earn too much for subsidies (above 400% FPL, roughly $60,000 for an individual in 2026), rarely see doctors, have no prescriptions, and have savings to cover a $9,200 emergency. You value low monthly costs and accept the risk of high out-of-pocket expenses.

When it doesn't: You qualify for subsidies, have ongoing medical needs, take regular medications, or lack emergency savings. A subsidized Silver plan with a $1,000 deductible and $50 monthly premium beats a catastrophic plan with $200 premiums and a $9,200 deductible in nearly every utilization scenario.

Catastrophic plans are often misunderstood as 'cheap insurance,' but they're really financial catastrophe insurance. They're appropriate for a narrow slice of the population—young, healthy individuals with substantial savings who can afford to self-insure for routine care. For everyone else, especially those eligible for subsidies, a Bronze or Silver plan almost always provides better financial protection and lower total costs

— Jennifer Tolbert

Common Mistakes to Avoid with Catastrophic Coverage

Underestimating healthcare needs. Many young adults assume they won't need care, then face unexpected illness or injury. A broken bone, appendicitis, or severe flu can generate $8,000 in bills quickly. If you lack savings to cover your deductible, you'll struggle to pay providers or delay necessary treatment.

Ignoring preventive benefits. Catastrophic plans cover preventive care at no cost, yet many enrollees skip annual check-ups because they associate the plan with "only for emergencies." Take advantage of free screenings, vaccinations, and wellness visits. Early detection of issues like high blood pressure or prediabetes can prevent expensive complications.

Not budgeting for the deductible. Choosing a catastrophic plan without setting aside funds to cover the $9,200 deductible is a recipe for financial distress. Open a dedicated savings account and contribute monthly. If you're saving $200 per month in premiums compared to a Bronze plan, bank that difference.

Overlooking subsidy eligibility. Many people eligible for premium tax credits choose catastrophic plans because the sticker price looks appealing, not realizing subsidies could reduce a Silver plan premium to $50 or less. Run the numbers on Healthcare.gov or your state marketplace before deciding. Input your income and household size to see actual costs.

Assuming catastrophic means "no coverage." These plans do cover you once the deductible is met, and they protect you from unlimited bills. Some enrollees avoid seeking care entirely, fearing they have no coverage. If you need emergency surgery, the plan will pay after you hit the deductible, and your total costs are capped.

Forgetting about network restrictions. Catastrophic plans use the same provider networks as other marketplace plans. Going out of network can mean higher costs or no coverage at all. Verify your doctors and hospitals are in-network before enrolling.

Frequently Asked Questions

Catastrophic health insurance serves a specific purpose: protecting young, healthy individuals from financial disaster due to major medical events while keeping monthly costs minimal. It's not a substitute for comprehensive coverage, nor is it the right choice for most people. The high deductibles and lack of subsidy eligibility make it a poor fit for anyone with regular healthcare needs or those who qualify for financial assistance.

Before choosing a catastrophic plan, calculate your total potential costs—premiums plus expected out-of-pocket expenses—and compare them to subsidized Bronze or Silver options. Factor in your savings cushion, risk tolerance, and healthcare utilization patterns. For the narrow group who meet the eligibility requirements and can afford to self-insure for routine care, catastrophic plans offer valuable peace of mind at a low monthly price. For everyone else, higher-tier plans with subsidies deliver better financial protection and lower overall costs