Driver reviewing car insurance policy near auto repair shop

What Is a Deductible in Car Insurance?

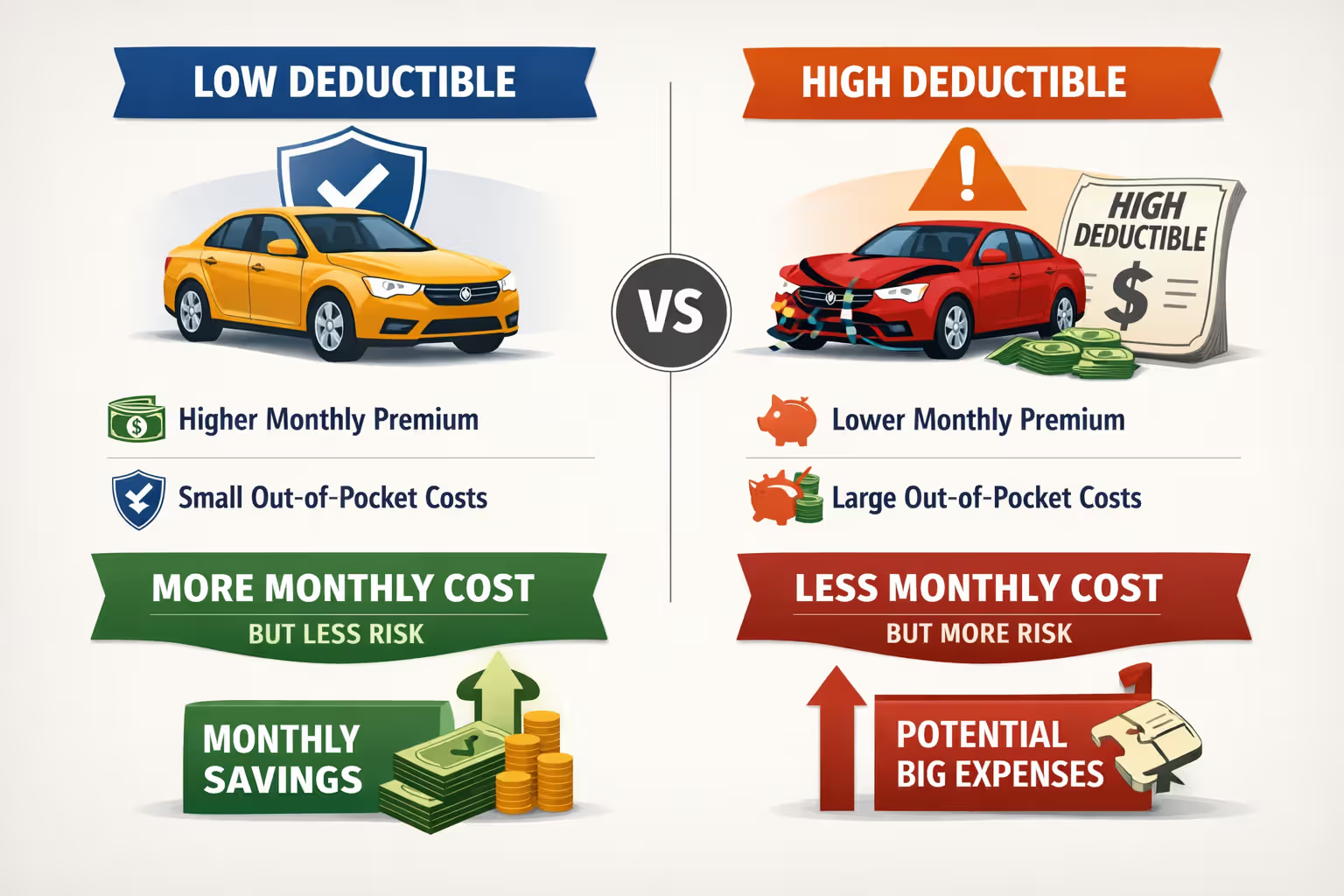

When you buy car insurance, you're agreeing to split the cost of future repairs with your insurance company. Your deductible is your share—the cash you'll hand over before your insurer pays a dime. Most policies let you pick anywhere from $250 to $2,000, and that choice matters more than most people realize.

Think of it this way: a $500 deductible means you're promising to cover the first $500 of damage every single time something goes wrong. In exchange, your insurer gives you a break on your monthly bill. That trade-off—pay less now, risk paying more later—is what trips up so many drivers.

Grasping how deductibles actually function saves you from nasty surprises when your car's been totaled or you're staring at a $3,000 repair estimate. The number you picked when you signed up? It becomes very real the moment you need it.

How Car Insurance Deductibles Work

Here's the basic setup. You cause $3,200 in damage backing into a concrete pillar. You've got a $500 deductible on your collision coverage. You pay $500, your insurer covers the remaining $2,700. Pretty straightforward.

But what if that same pillar only caused $400 in damage? You're covering all of it yourself. Your deductible works as a threshold—damage below that number comes entirely out of your pocket. Filing a claim for $400 when your deductible is $500 accomplishes nothing except creating a paper trail that might haunt your renewal rates.

The per-claim structure catches people off guard. Health insurance resets deductibles annually. Car insurance? Every separate incident triggers a fresh deductible payment. Back into a pillar in March, hit a deer in July, slide into a ditch in November—that's three deductible payments in one year, even though you're paying for the same policy.

Now for the part that confuses almost everyone: liability coverage operates completely differently. You rear-end someone and their repair bill hits $7,500? Your liability coverage pays every penny without asking you for a deductible. Zero. Nada. You're already at fault and paying higher premiums as a consequence—insurers don't pile on an additional out-of-pocket charge.

Some insurers sweeten the deal with vanishing deductibles. Stay claim-free for a year, and they knock $50 or $100 off your deductible. String together five clean years and your $500 deductible might disappear entirely. Others offer what's called a deductible waiver for glass—depending on your state, that windshield chip might get fixed without you paying anything at all.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Types of Car Insurance Coverage That Use Deductibles

Only certain parts of your policy require you to chip in before your insurer does. Knowing which ones involve deductibles helps you budget for the actual cost of a claim.

Collision Coverage kicks in when your car smacks into something or gets smacked. Another vehicle, a guardrail, a mailbox, the ground after flipping—all collision claims. Fault doesn't matter here. Even if the other driver ran a red light, using your own collision coverage means paying your deductible first. Most people select $500 or $1,000, applying the same amount regardless of how the collision happens.

Comprehensive Coverage handles everything else that can wreck your car without actually colliding. Someone keys your paint job? Comprehensive. Hailstorm dents your hood? Comprehensive. Catalytic converter gets stolen in a parking lot? Comprehensive. Many drivers go with a lower deductible here—maybe $250 instead of $500—since these incidents feel more random and beyond your control.

Uninsured/Underinsured Motorist Property Damage gets complicated because state laws vary wildly. This coverage fixes your car when someone without insurance (or without enough insurance) damages it. Some states mandate this coverage but ban deductibles on it. Others allow deductibles but cap them at $200 or $250. A few states don't require the coverage at all, making it optional with whatever deductible your insurer offers.

Personal Injury Protection goes either way depending where you live. Florida requires it with no deductible. Michigan lets you add one if you want. New Jersey gives you a choice between deductible and non-deductible versions. You'll need to dig into your actual policy documents—the declarations page spells out exactly what you're paying for.

What never involves a deductible? The liability coverages. Bodily injury liability, property damage liability, uninsured motorist bodily injury—none of those ask for money upfront because they're protecting other people or covering your injuries when someone else messed up.

Your coverage limits play a separate role from deductibles. Say you've got $50,000 in comprehensive coverage with a $500 deductible, and your $22,000 car gets stolen and never recovered. You're getting $21,500—the car's value minus your deductible. The $50,000 limit represents the ceiling your insurer will pay, while your deductible sets the floor you're always responsible for.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

How to Choose Your Deductible Amount

Picking a deductible means predicting your own future, which nobody's great at. You're guessing whether you'll have an accident, how much savings you'll have when it happens, and what your car will be worth at that mystery future date.

Start with the premium math. Bumping your deductible from $500 to $1,000 typically shaves 15-30% off your annual cost. Let's say you're paying $1,600 yearly for full coverage. Choosing $1,000 over $500 might save you $280 each year. Sounds great, right? But file one claim and you're paying an extra $500 out of pocket, instantly erasing nearly two years of savings.

Track your actual driving history. Gone five years without filing a claim? Maybe you can handle a higher deductible—you're clearly not using the coverage often. Meanwhile, if you filed two claims in the past three years, a $2,000 deductible is basically guaranteeing you'll be scrambling for cash next time something goes wrong.

Your emergency savings account matters more than anything else. Can you pull $1,000 from savings today without missing rent or putting groceries on a credit card? Then $1,000 is your upper limit. Would a sudden $1,000 expense force you to carry credit card debt at 22% interest? Drop down to $500, even if it costs you $20 more per month. That extra premium buys you financial stability when you're already stressed about a crashed car.

Set your deductible at whatever amount you could pull from savings in 24 hours without breaking a sweat.You're choosing this number on a calm Tuesday afternoon. You'll need that actual cash on a chaotic Thursday morning when your car's undriveable and you've got to get to work

— Sarah Chen

Vehicle age changes everything. Your car's worth $5,000 now, down from $28,000 when you bought it four years ago. Keeping a $250 deductible on a $5,000 car means you're self-insuring only 5% of its value—you might as well self-insure more and pocket the premium savings. Once cars dip below $4,000 in value, plenty of drivers drop collision and comprehensive entirely, accepting they'll just replace the car out-of-pocket if something catastrophic happens.

Consider your daily reality. Parking on crowded city streets every day? That's high ding-and-dent territory. Commuting 80 miles daily on icy highways? More accident exposure than someone working from home and driving 6,000 miles yearly. Match your deductible to your actual risk—more exposure argues for lower deductibles that won't devastate you when the inevitable happens.

| Your Deductible | What You'll Pay Annually | Cash Needed Per Claim | Makes Sense For |

| $250 | $1,800 | $250 | Brand-new drivers, people with tight budgets, expensive new vehicles, high-theft neighborhoods |

| $500 | $1,500 | $500 | Average drivers with decent savings, cars worth over $15,000, moderate commuting |

| $1,000 | $1,200 | $1,000 | Clean driving records spanning 5+ years, solid emergency funds, established safe drivers |

| $2,000 | $1,050 | $2,000 | Ten-year spotless records, substantial savings, older vehicles, minimal driving |

These numbers reflect typical costs for full coverage on a mid-sized sedan in a medium-risk ZIP code. Your actual premiums will shift based on your specific location, vehicle, and history.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

The Car Insurance Claim Process With Deductibles

The moment you realize you need to file a claim, the deductible shifts from abstract number to concrete problem. Here's how the money actually moves.

Step 1: You Report What Happened: Call your insurer right after the incident—same day if possible. You'll describe the damage, location, and circumstances. They'll assign a claim number and connect you with an adjuster. During this conversation, confirm which coverage applies and what deductible goes with it. Don't assume you remember correctly—verify it against your policy documents.

Step 2: Someone Inspects the Damage: An adjuster either visits the repair shop to examine your car in person or asks you to upload photos through your insurer's app. They're calculating repair costs or, if your car's totaled, its current market value. This estimate becomes the foundation for everything else—it determines how much your insurance pays and whether filing even makes sense.

Step 3: You Get Repairs Authorized: Once the adjuster signs off, you can proceed with repairs. Your insurer might push you toward their "preferred" shop network, but you can usually pick your own mechanic. The shop and the insurer work out the approved repairs and payment logistics behind the scenes.

Step 4: You Pay Your Share: This timing varies dramatically. Some insurers have you pay the deductible directly to the repair shop when you pick up your car—the shop gets the insurance payment separately, and you're settling your portion in person. Other insurers subtract your deductible from the total and cut you one check for the difference. You then pay the shop that amount plus your deductible portion, effectively paying your deductible indirectly.

Total loss claims work differently. Your car's deemed unfixable or not worth repairing. The insurer values it at $14,000. With a $500 deductible, they mail you a check for $13,500. You're getting the car's value minus what you agreed to cover.

Step 5: Repairs Finish and Everyone Settles Up: The shop completes the work and may require an inspector's sign-off. If they discover hidden damage mid-repair (extremely common with collision damage), the adjuster approves supplemental payments to cover the additional work. You don't pay your deductible again—it's one payment per claim no matter how many revisions the estimate requires.

Sometimes you sidestep your deductible completely. Another driver clearly causes the accident and their insurer admits fault. Their liability coverage pays your entire repair bill—no deductible. If fault's disputed, you might file through your collision coverage initially (paying your deductible), then your insurer pursues the other driver's insurance to recover everything, including your deductible. Once they succeed—usually 30 to 90 days later—they refund your deductible.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Common Deductible Mistakes to Avoid

Most deductible regrets fall into predictable patterns. Dodge these traps and you'll handle claims far more smoothly.

Selecting Deductibles Based on Fantasy Finances: That $2,000 deductible looks brilliant when you're imagining your future disciplined-saver self. It looks terrible when present-day you has $800 in savings and needs $2,000 cash by Friday. Choose deductibles based on the money you actually have right now, not the savings account you wish you had.

Getting Confused About When You Pay: Drivers expect to pay a deductible when they damage someone else's property. Wrong—that's liability, no deductible required. Others assume their insurer will cover their own vehicle damage without any contribution when they're clearly at fault. Also wrong—that's collision coverage, deductible definitely applies. These misunderstandings create frustration that a quick policy review would prevent.

Customizing Deductibles Then Forgetting: You absolutely can set collision at $1,000 and comprehensive at $250. Plenty of people do exactly this. Then a year later they file a comprehensive claim and get surprised by their $250 deductible, having convinced themselves everything was $1,000. Skim your declarations page every time you get your renewal—it takes 90 seconds.

Filing Claims That Barely Exceed Your Deductible: You've got a $500 deductible and $650 in damage. Filing that claim nets you $150 but often triggers rate increases costing hundreds annually for the next three to five years. Unless damage significantly exceeds your deductible—say, at least double—paying out-of-pocket frequently makes more financial sense. At-fault claims especially tend to spike your premiums regardless of the payout amount.

Setting It Once and Never Adjusting: Your ideal deductible three years ago isn't necessarily ideal now. Your emergency fund has grown. Your car has depreciated $6,000. You've moved to a lower-risk neighborhood. All of these suggest revisiting your deductible choice, yet most drivers maintain the same amount for years simply because changing requires initiative.

Thinking Deductibles Reset Annually: Health insurance trains us to think about annual deductibles. Max it out in February? The rest of the year is smooth sailing. Car insurance doesn't work that way—every separate claim resets the clock. Three incidents mean three deductible payments, even if they happen within weeks of each other.

Ignoring State-Specific Options: Your state might offer deductible buyback endorsements, disappearing deductibles, or zero-cost glass coverage. Drivers who don't investigate their state's specific rules leave money on the table, paying more than necessary or maintaining higher deductibles than required.

Frequently Asked Questions About Car Insurance Deductibles

Your deductible represents one of those financial decisions that feels abstract until it suddenly becomes urgent. The number you picked months or years ago determines whether a car accident creates a minor inconvenience or a major financial crisis.

Begin by honestly assessing your savings. How much cash could you access tomorrow if your car was undriveable and needed immediate repairs? That's your realistic maximum deductible. Calculate premium differences between deductible options—sometimes the savings don't justify the additional risk. Factor in your vehicle's current value, which might be far lower than when you bought coverage. Consider your driving patterns, claim history, and daily environment.

Review these choices annually, particularly after significant life changes—income increases, improved savings, vehicle depreciation, or moves to different risk areas. The deductible that suited your circumstances three years ago might not fit today. And make sure you understand which coverages involve deductibles and which don't. Knowing that liability never requires upfront payment while collision always does prevents confusion when you're already stressed about vehicle damage.

The right deductible balances monthly affordability against realistic emergency preparedness, matching your actual financial situation to your real driving risks.