Cars driving on an American road illustrating car insurance requirements

Do You Have to Have Car Insurance in the United States?

Content

Here's something most drivers don't realize: car insurance laws in America vary wildly from one state to another. You might be perfectly legal cruising through Nashville with your current policy, but cross into another state and suddenly you're breaking the law.

Nearly every state in America requires some form of car insurance before you can legally drive. But—and this is important—two states take a different approach entirely. And even in states with strict insurance laws, certain situations let you operate vehicles without traditional coverage.

Drive without proper insurance and you're risking more than a ticket. We're talking suspended licenses, impounded vehicles, thousands in fines, and potentially devastating personal liability if you cause an accident. In 2026, with medical costs and vehicle values climbing higher than ever, understanding these requirements isn't optional.

Let's walk through exactly what you need to know: which states require what coverage, how to avoid penalties, and the nuts and bolts of deductibles and filing claims when something goes wrong.

Legal Requirements for Car Insurance by State

America doesn't have a single, unified car insurance law. Instead, each state writes its own rules, sets its own minimums, and enforces them differently. What this means for you: a bare-bones policy that's legal in one state might leave you ticketed in another.

The concept behind all this is "financial responsibility." States don't necessarily care whether you have insurance specifically—they care that you can pay for damage you cause. Insurance is just the most common way to prove financial responsibility. Some states also accept cash bonds, certificates of deposit, or self-insurance documentation if you meet specific criteria.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

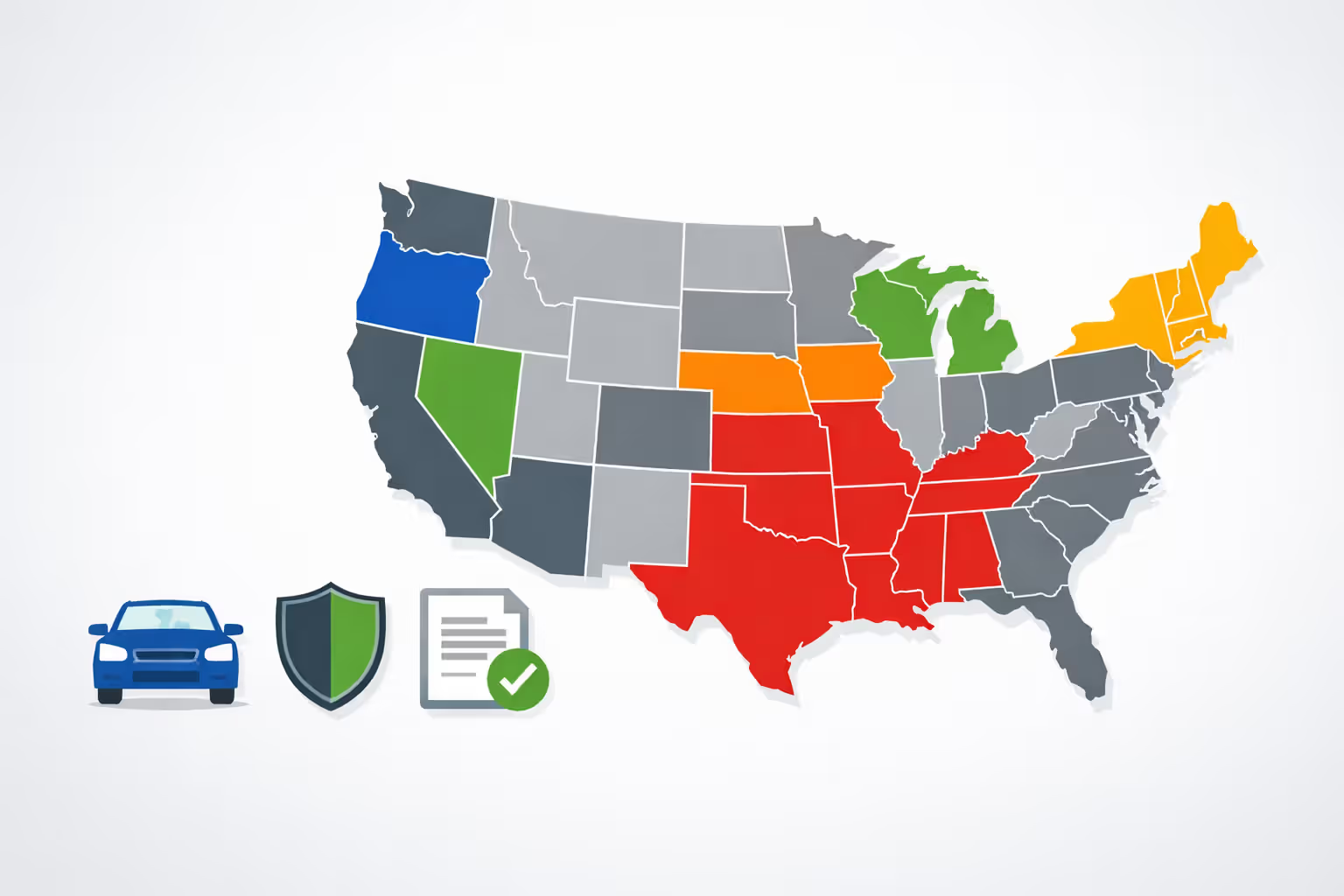

States That Require Car Insurance

Forty-eight states plus Washington D.C. won't let you register or drive a vehicle without maintaining at least minimum liability coverage. These "compulsory insurance" laws mean continuous coverage isn't a suggestion—it's mandatory.

But here's where it gets tricky: those minimums aren't consistent. California forces you to carry just 15/30/5 coverage (that's $15,000 per person injured, $30,000 total per accident, and $5,000 for property damage). Meanwhile, Maine requires 50/100/25—more than triple California's minimums for some categories. These represent absolute minimums. Ask any insurance agent and they'll tell you these bare-minimum policies rarely provide adequate protection.

How do states verify you're actually insured? Several ways. Police can check coverage status electronically during traffic stops. Your DMV typically demands proof of insurance when you renew registration. Some states run random audits throughout the year, sending letters demanding you prove coverage for every vehicle registered in your name.

States With Alternative Options

New Hampshire and Virginia break from the pack, though calling them "insurance optional" oversimplifies the reality.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

New Hampshire doesn't force you to buy insurance upfront. Sounds great, right? Here's the catch: cause an accident and you must personally cover every dollar of damage. Can't pay? The state suspends your license and registration immediately. You'll need to settle all outstanding debts AND maintain proof of financial responsibility (usually via SR-22 filing) for the next three years. Most New Hampshire residents carry insurance voluntarily because the alternative is financial Russian roulette.

Virginia offers a different workaround: pay the state $500 annually for an "Uninsured Motor Vehicle" fee when registering your car. That fee buys you exactly zero coverage. Cause a crash and you're on the hook for every medical bill, every vehicle repair, every legal fee. The UMV option makes sense only if you're registering a vehicle you rarely drive or keep in storage most of the year.

Important caveat for both states: financing a vehicle? Your lender will demand comprehensive and collision coverage regardless of what state law allows. Banks protect their collateral, period.

What Car Insurance Coverage Is Legally Required

When states mandate insurance, they're specifically talking about liability coverage. This pays for harm you inflict on other people—their hospital bills, car repairs, lost paychecks, and legal damages. Notice what's missing? Anything related to your own vehicle or injuries.

Liability coverage splits into two categories:

Bodily injury liability handles medical expenses, rehabilitation, lost wages, and pain-and-suffering damages when you hurt someone in a crash. Those three numbers in coverage descriptions work like this: 25/50/25 means $25,000 maximum per injured person, $50,000 maximum per accident total, and $25,000 for property damage. Injure three people? Each can claim up to the per-person cap, but combined they can't exceed the per-accident limit.

Property damage liability covers physical damage you cause to other vehicles, buildings, guardrails, utility poles, and anything else you crash into. That third number in coverage shorthand represents this limit. Here's a reality check for 2026: average new car prices exceed $48,000. Hit one luxury SUV and watch $25,000 in property coverage evaporate before you've even addressed the mangled guardrail or damaged storefront.

Some states pile on additional requirements beyond basic liability. Twelve states mandate personal injury protection (PIP) or medical payments coverage—these pay your own medical bills regardless of who caused the accident. These "no-fault" provisions reduce lawsuits by requiring each driver's insurance to handle their own injuries first.

About twenty states require uninsured/underinsured motorist coverage. This protects you when someone without insurance (or with inadequate coverage) crashes into you. Given that roughly 13% of American drivers operate uninsured vehicles, this coverage fills a dangerous gap.

What states DON'T require: comprehensive coverage (theft, vandalism, hail damage), collision coverage (repairs to your vehicle after crashes), or rental reimbursement. These protect your interests rather than others' legal rights, so states leave them optional. Lenders almost always mandate comprehensive and collision on financed vehicles, though.

Think carefully about coverage limits beyond bare minimums. A severe multi-vehicle accident with serious injuries can generate $500,000+ in medical bills and legal judgments. Carrying only 25/50/25 leaves you personally responsible for amounts exceeding those limits. Insurance professionals typically recommend 100/300/100 as a realistic baseline, with umbrella policies adding $1-2 million in extra protection for relatively small additional premiums.

State minimum coverage requirements were established decades ago and haven't kept pace with medical costs, vehicle values, or litigation trends. Drivers carrying only minimum limits are essentially underinsured and risk financial catastrophe after a serious accident

— Janet Ruiz

Exceptions and Special Circumstances

A few specific situations allow vehicle ownership or operation without standard insurance policies, though these exceptions come with major caveats.

Self-insurance certificates exist in most states for entities operating large vehicle fleets. You'll typically need 25+ vehicles and must deposit $50,000-$150,000 in cash or bonds with your state. This option makes sense exclusively for businesses or extremely wealthy individuals comfortable assuming direct financial risk.

Stored or non-operational vehicles escape insurance requirements in most states once you surrender plates and registration. Project cars, seasonal vehicles, or broken-down cars awaiting parts qualify. But the instant you re-register that vehicle or drive it anywhere public, insurance requirements snap back. Some states require filing an official "non-operational" declaration to prevent insurance verification penalties.

Military members stationed overseas can sometimes suspend insurance on vehicles stored stateside, though policies differ by insurer and state. Most insurance companies offer military suspension discounts rather than complete cancellation, which maintains your continuous coverage history.

Vehicles exclusively on private property generally don't require insurance assuming they never touch public roads. Farm equipment, off-road toys, and cars driven solely on private land fall here. But "public road" has a broader definition than most people think—even driving across a public street to reach another private property can trigger insurance requirements.

Classic and antique vehicles sometimes qualify for special registration categories with reduced insurance requirements, particularly if you accept mileage caps and usage restrictions. These policies usually cost less but explicitly prohibit daily driving or commuting.

None of these exceptions shield you from liability when accidents happen. A stored vehicle that rolls into the street causing damage, or an uninsured farm truck driven "just once" to the hardware store—both can generate massive personal liability.

Penalties for Driving Without Car Insurance

Getting caught without insurance sets off a domino effect of consequences extending far beyond the initial ticket.

First-offense penalties vary by state but typically range from $100-$500 fines, though some states slam violators with $1,000+ penalties. Courts sometimes reduce fines if you obtain insurance within 30 days and provide proof. Some jurisdictions tack on community service or mandatory insurance education classes.

License and registration suspension follows in most states, often automatically triggered. Your driving privileges vanish for anywhere from 30 days to a full year, depending on state law and your violation history. Reinstatement demands paying suspension fees ($50-$250), proving current insurance, and sometimes filing SR-22 certificates. During suspension, driving for any reason—including genuine emergencies—compounds your legal troubles.

SR-22 certificates are financial responsibility filings that your insurance company submits to your state, proving you maintain required coverage. States impose SR-22 requirements after serious violations: driving without insurance, DUI convictions, reckless driving, multiple at-fault crashes, or license suspensions. The SR-22 obligation typically lasts three to five years. Your insurer files the original certificate and must notify the state if your policy lapses or cancels. Any coverage interruption automatically suspends your license. Not every insurer offers SR-22 filings, and those that do charge substantially higher premiums—frequently 50-100% increases.

Vehicle impoundment happens in some states after repeat violations or crashes while uninsured. Impound fees accumulate daily ($50-$150 per day), and you can't retrieve your vehicle without proof of insurance. After 30 days, some states auction impounded vehicles to recover storage costs.

Accident liability becomes personally catastrophic without insurance. Cause a crash while uninsured and you're personally liable for all damages—medical bills, vehicle repairs, lost income, pain and suffering, and attorney fees. A moderate accident easily generates $50,000-$100,000 in claims. Victims can sue you, garnish your wages, place liens on your property, and pursue collection for years. Bankruptcy might discharge some accident-related debt, but not always.

Long-term insurance costs spike after uninsured periods. Insurance companies view coverage gaps as red flags indicating high-risk behavior. Expect 30-50% premium increases when resuming coverage, with surcharges lasting three to five years. Multiple lapses can make you virtually uninsurable except through high-risk state-assigned pools with premiums double or triple standard rates.

Criminal charges apply in some states for repeat offenses or accidents causing serious injury while uninsured. Misdemeanor charges can result in jail time, probation, and permanent criminal records affecting future employment and housing opportunities.

The financial math is brutal: a year of minimum liability insurance costs $400-$800 in most states. A single day driving uninsured can trigger $2,000+ in fines, fees, and increased premiums—plus unlimited personal liability if you cause a crash.

How Car Insurance Deductibles and Coverage Limits Work

Understanding deductibles and coverage limits helps you balance what you pay monthly against protection when accidents happen. These two elements function differently but both dramatically affect what you'll actually receive when filing claims.

Coverage limits represent the absolute maximum your insurer pays per claim. Liability limits follow that three-number format discussed earlier (like 100/300/50). Comprehensive and collision coverage typically use single-limit deductibles instead of per-person/per-accident structures.

Selecting appropriate limits involves honestly assessing your assets and risk exposure. Own a home? Have retirement savings? Earn substantial income? You're an attractive target for lawsuits after serious accidents. Plaintiffs' attorneys specifically pursue defendants with "deep pockets." Carrying 100/300/100 liability coverage plus a $1-2 million umbrella policy costs perhaps $800-$1,200 annually but protects assets worth exponentially more.

Property damage limits deserve special attention in 2026. Average new car prices exceed $48,000, with luxury vehicles routinely surpassing $80,000. The old-standard $25,000 property damage limit won't cover a totaled luxury SUV, much less multiple vehicles in chain-reaction crashes. Increasing property damage coverage to $100,000 typically adds just $50-$100 to annual premiums.

Deductibles represent amounts you personally pay out-of-pocket before insurance coverage kicks in. They apply to comprehensive and collision claims—coverage protecting your own vehicle. Common deductibles range from $250 to $2,000. Higher deductibles reduce premiums; lower deductibles mean less immediate cash needed after accidents.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

The deductible decision involves both math and psychology. Increasing your deductible from $500 to $1,000 might save $200 annually. Skip filing claims for three years and you've saved $600—enough to cover the higher deductible plus $100 extra. But you need $1,000 available immediately after an accident, which strains some household budgets.

A practical approach: select deductibles you can comfortably afford from emergency savings. If $500 would strain your budget, don't choose a $1,000 deductible just to save $150 yearly. The stress and financial scrambling after crashes isn't worth modest premium savings.

Deductible application varies by coverage type. You pay your deductible once per claim, not per vehicle or per person. If hailstorm damages your car (comprehensive claim) and you later hit a deer (another comprehensive claim), you'll pay the deductible twice—these constitute separate incidents. But cause an accident damaging three other vehicles? You don't pay three deductibles; liability coverage operates without deductibles.

Some insurers offer "disappearing" or "vanishing" deductibles that decrease $50-$100 annually for claim-free driving. After five years without claims, your $500 deductible might drop to $250 or even $0. This rewards safe driving while providing better protection over time.

Coverage limit tiers affect premiums less than many assume. Increasing liability coverage from 50/100/50 to 100/300/100 frequently adds only 10-15% to premiums. The jump from state minimums to adequate coverage costs more proportionally, but still represents excellent value. Doubling your protection doesn't remotely double your premium.

Review coverage limits annually. As your assets grow—home equity, retirement accounts, savings—increase liability limits correspondingly. Your insurance protection should scale with your financial life.

Filing a Car Insurance Claim When Coverage Is Required

The claim process determines whether your insurance provides smooth support or bureaucratic nightmare. Understanding steps and common pitfalls helps you navigate claims efficiently.

Immediate post-accident steps establish the foundation for successful claims. First, ensure everyone's safety and dial 911 if anyone is injured or vehicles block traffic. Collect information from other drivers: full names, contact numbers, insurance companies, policy numbers, and vehicle registrations. Photograph vehicle damage, street positioning, traffic signals, skid marks, and the overall scene from multiple angles. These photos prove invaluable weeks later when memories fade and stories shift.

Avoid admitting fault at the scene. Stick to factual observations: "I didn't see the other car approaching" rather than "This is completely my fault." Fault determination involves complex factors—traffic laws, right-of-way rules, witness accounts—that accident participants can't accurately assess in the moment. Fault admissions can undermine your position even if subsequent investigation reveals shared responsibility or exonerating circumstances.

Author: Nathaniel Porter;

Source: talero.spotpariz.net

Reporting the claim should happen within 24 hours, even if you're uncertain about pursuing coverage. Policies typically require "prompt" or "immediate" notification; significant delays can jeopardize claims entirely. Call your insurer's claims hotline (available 24/7 with most companies) and relay basic accident details. You'll get assigned a claim number and adjuster contact.

Many insurers now provide mobile app claim filing with photo uploads, AI-powered damage estimates, and real-time status tracking. These digital tools accelerate processing but don't replace human adjusters for complex claims.

Adjuster evaluation begins within one to three business days. The adjuster contacts you to discuss the accident, review your account, and inspect vehicle damage. For minor claims, adjusters frequently assess damage exclusively through submitted photos. Larger claims require in-person inspections at your home, a body shop, or the insurer's claims facility.

The adjuster determines fault based on police reports, witness statements, photographs, and state traffic laws. Clear-cut cases (rear-end collisions, red-light violations) involve straightforward fault assignment. Complicated scenarios—intersection crashes, merging accidents, parking lot incidents—demand more thorough investigation.

Repair authorization follows damage assessment. The adjuster provides a repair estimate and authorizes work at your selected body shop (or the insurer's preferred shop, which may offer guarantees and expedited processing). You'll pay your deductible directly to the repair shop; insurance covers remaining costs up to your vehicle's actual cash value.

When repairs exceed vehicle value, insurers "total" the car and pay you its pre-accident market value minus your deductible. You can negotiate total-loss settlements using comparable vehicle listings, recent sales data, and condition documentation. Many insurers use valuation services like CCC ONE or Mitchell, which aggregate market data determining fair value.

Rental reimbursement requires separate optional coverage (typically $20-40 annually). Without this add-on, you're personally responsible for rental costs while your car undergoes repairs. Rental coverage pays $30-$75 daily up to policy limits, usually capped at 30 days maximum. Book rentals promptly after accidents; coverage begins when repairs start, not when the accident occurred.

Claim timelines vary by complexity. Straightforward property damage claims with clear fault frequently settle within 7-14 days. Injury claims drag on for months or years, especially when medical treatment continues or liability remains disputed. Most states require insurers acknowledging claims within 15 days and making coverage decisions within 30-45 days, though these timelines extend when investigation continues.

Common mistakes that undermine otherwise valid claims:

- Delaying medical treatment after injuries. Gaps between accidents and treatment suggest injuries aren't accident-related.

- Signing quick settlement releases before understanding full damages. Once you sign, you can't reopen claims for additional costs discovered later.

- Providing recorded statements without fully understanding questions. Insurers use recorded statements locking in your version of events; later inconsistencies damage your credibility.

- Failing to document ongoing expenses. Retain receipts for rental cars, medical copays, lost wages, and other accident-related costs.

- Discussing accidents on social media platforms. Insurance companies and opposing attorneys routinely review social media seeking contradictory statements or evidence suggesting fraud.

Denied claims occur when coverage doesn't apply (wrong coverage type, lapsed policy, excluded driver), fraud is suspected, or you failed meeting policy conditions. You can appeal denials by submitting additional documentation, correcting misunderstandings, or escalating to supervisors. State insurance departments handle complaints when insurers demonstrate bad faith or violate regulations.

Most claims conclude satisfactorily when you document thoroughly, communicate clearly, and understand your coverage. The claim process ultimately tests whether your insurance provides genuine protection or merely paperwork.

Frequently Asked Questions About Car Insurance Requirements

Car insurance requirements exist protecting everyone sharing the road, not merely generating revenue for insurers or states. The question "do you have to have car insurance" has a straightforward answer for most Americans: yes, with rare exceptions carrying significant financial risk.

Understanding your state's specific requirements, selecting coverage limits protecting your assets, and maintaining continuous coverage prevents both legal troubles and financial catastrophe. State minimum coverage satisfies legal obligations but frequently provides woefully inadequate protection after serious accidents. The modest cost difference between minimum coverage and robust protection—often just $200-$400 annually—represents one of the best values in personal finance.

Penalties for driving uninsured extend far beyond initial fines. License suspensions, SR-22 requirements, skyrocketing premiums, and unlimited personal liability make uninsured driving among the riskiest financial decisions Americans make. A single accident without coverage can derail your financial life for years or decades.

Take time reviewing your current coverage, compare it against both your state's requirements and your personal assets, then adjust limits accordingly. The few minutes spent understanding deductibles, coverage limits, and the claim process pay substantial dividends when accidents occur. Car insurance isn't merely a legal checkbox—it's financial protection preserving your assets, income, and peace of mind.